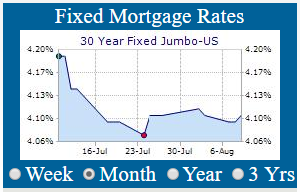

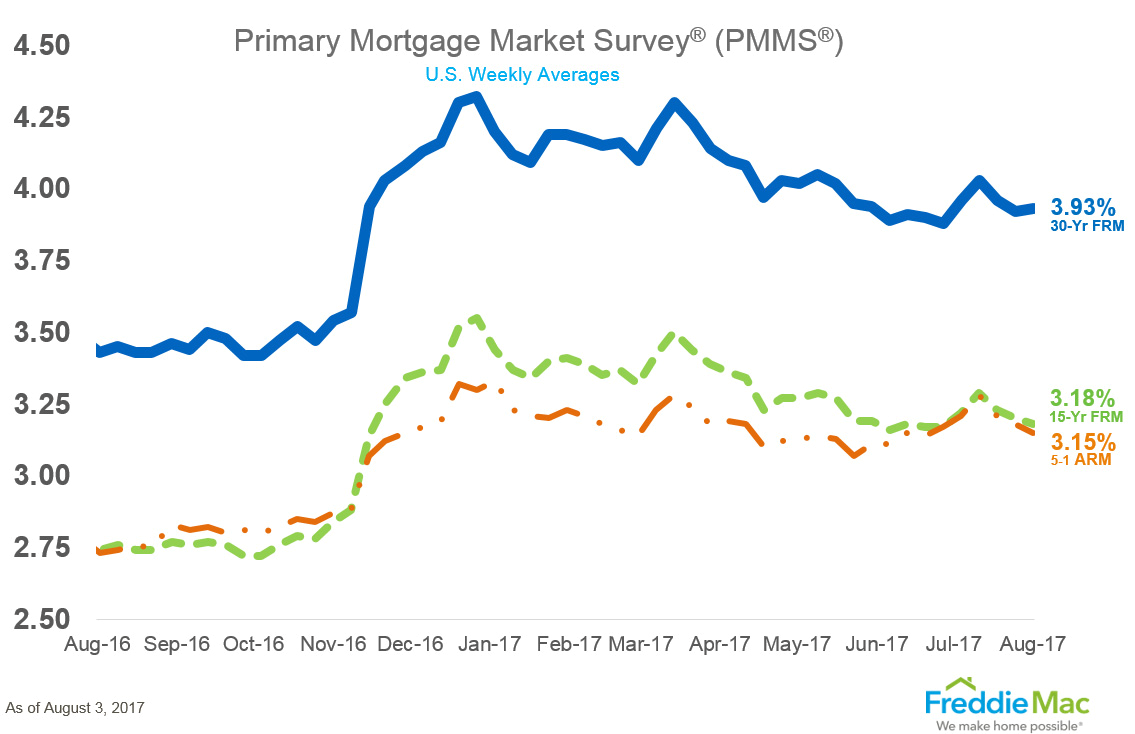

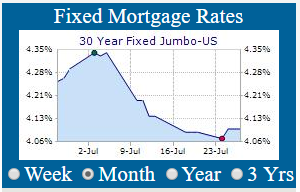

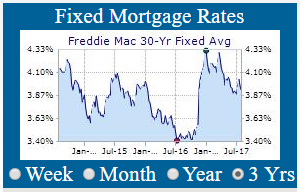

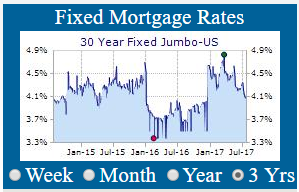

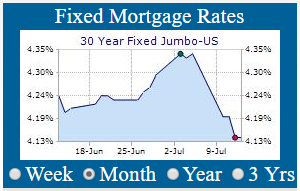

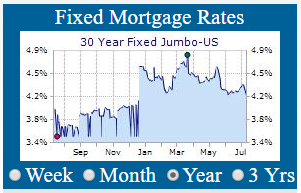

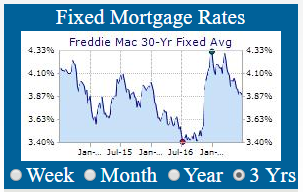

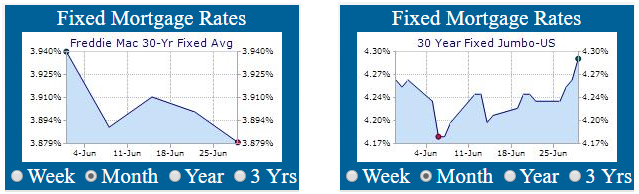

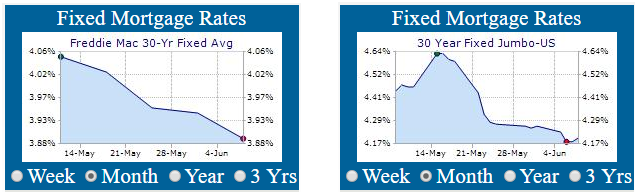

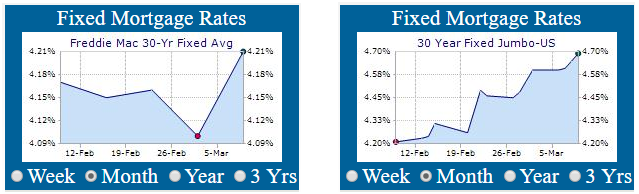

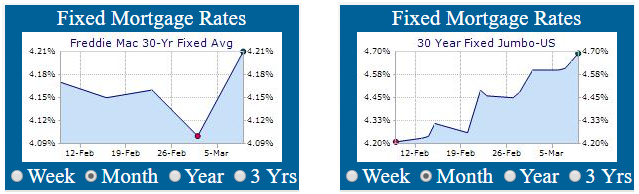

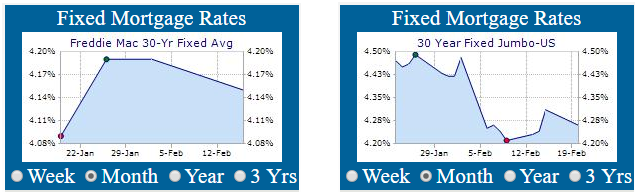

Current 30-Year Fixed Mortgage Rates Overview

"This page dedicated to current 30-year fixed mortgage rates offers a comprehensive and up-to-date overview of mortgage rate trends and financial market insights. This resource is designed to assist homeowners and potential buyers in understanding the landscape of mortgage rates, providing valuable context for financial decisions. With detailed analysis and easy-to-understand graphs, the page presents a snapshot of current rates, alongside key economic indicators that influence these rates. Whether you're considering refinancing, purchasing a new home, or simply staying informed about market conditions, this page serves as an essential tool for navigating the complex world of mortgage financing."

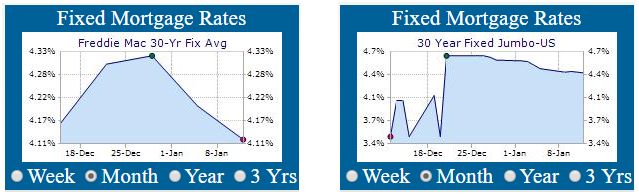

ERATE's Daily Rate Summary

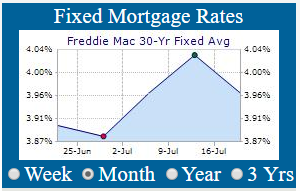

August 14, 2017

Mortgage Rates and Treasury Yields Fall.

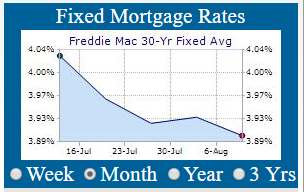

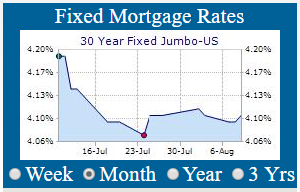

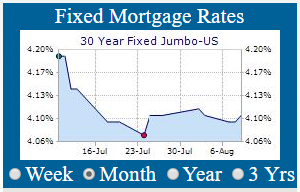

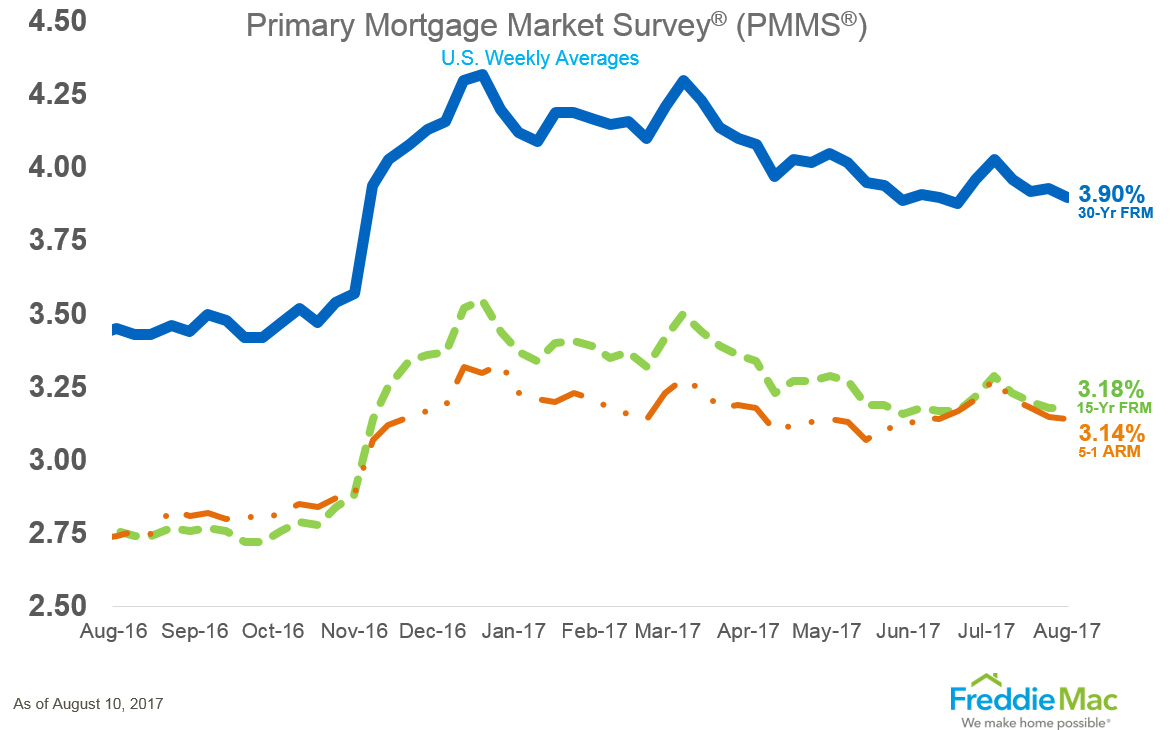

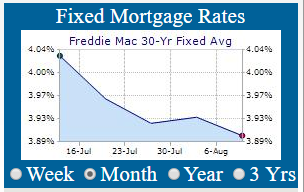

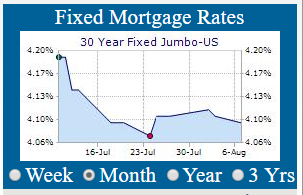

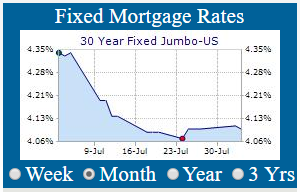

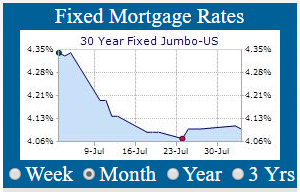

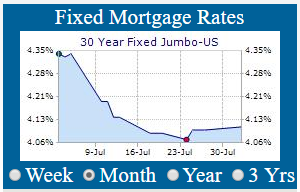

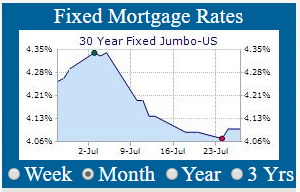

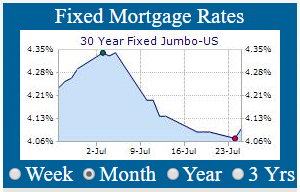

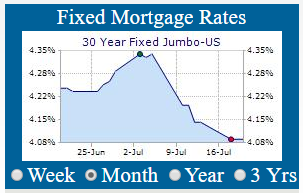

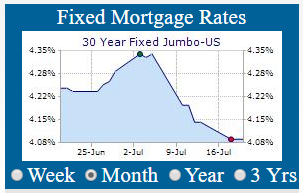

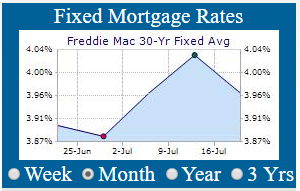

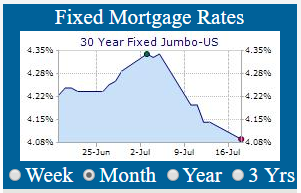

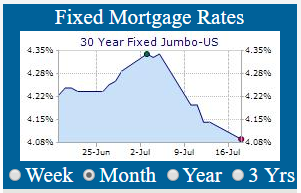

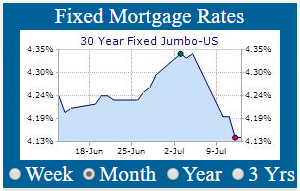

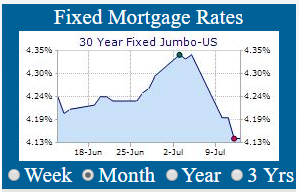

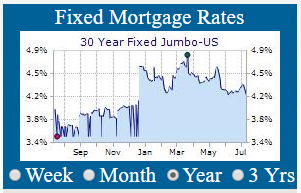

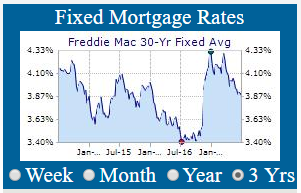

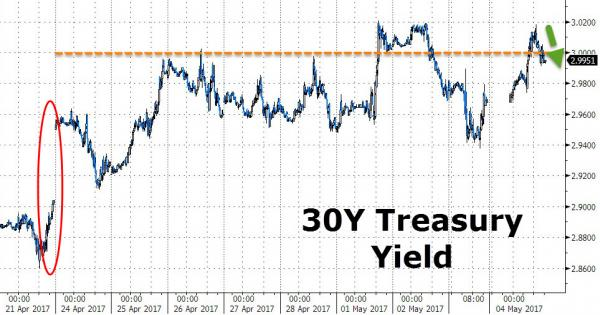

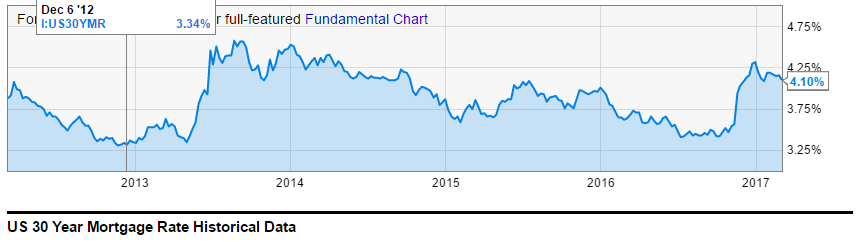

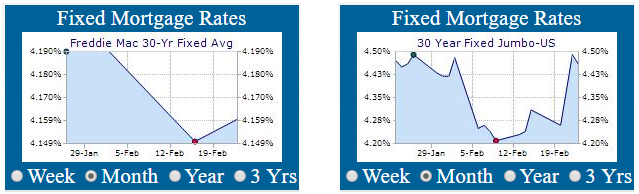

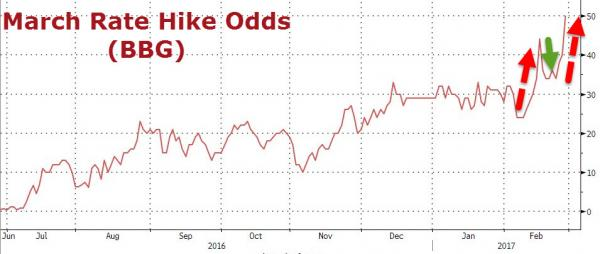

On Friday, Treasury bond yields and Mortgage interest rates fell as Credit Market participants bet on volatility and interest rate moderation in ‘quiet’ period in August. The September 10 Yr. U.S. Treasury Note stood at a yield of 2.1888% and the 30 Yr. U.S. Treasury Bond is yielding 2.7855%. 30 Year Mortgages according to Freddie Mac were around 3.90% for conforming and 4.10% for Jumbo products.

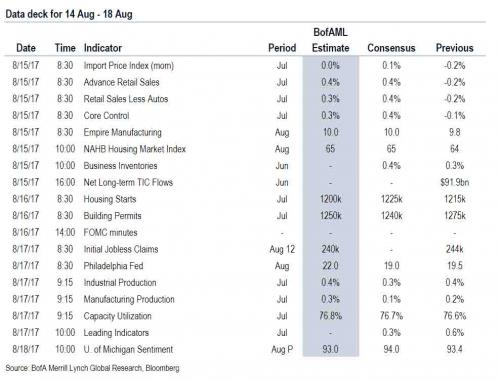

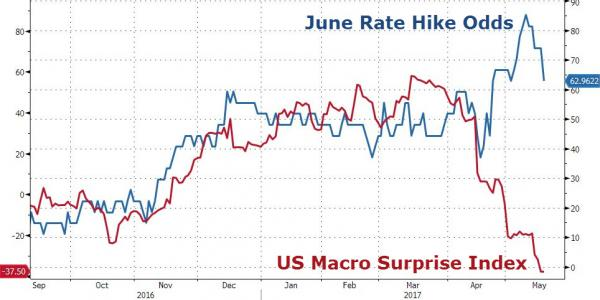

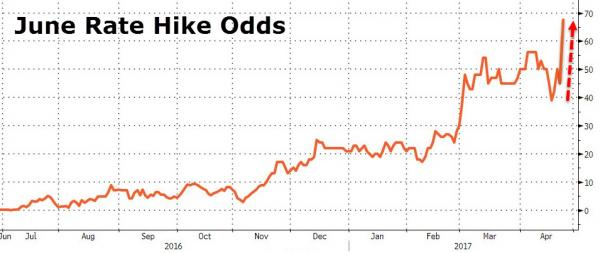

There are a number of key data releases for the Week of Aug 14th through Aug 18th. According to Goldman Sachs, the key economic data releases this week are retail sales on Tuesday and industrial production on Thursday. There are a few scheduled speaking engagements by Fed officials this week. In addition, the minutes from the July FOMC meeting will be released on Wednesday.

Goldman Sachs: Key Data Releases for Week of Aug 14th to Aug 18th

(Chart courtesy of Zerohedge.com).

This week should provide confirmation of the direction of economic activity and the pace of the recovery and further confirm the path for the economy and interest rate policy. The Jackson Hole Symposium will kick off next week. A lot will depend on inflationary expectations as CB’s assess ‘animal spirits’ and incoming economic data toward further tightening of interest rates & balance sheet normalization policy.

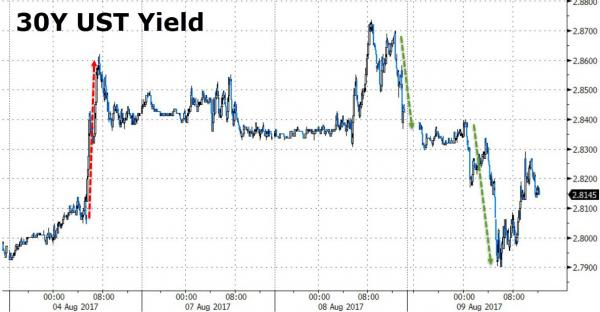

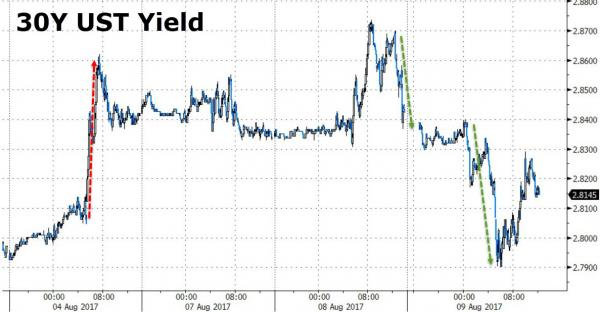

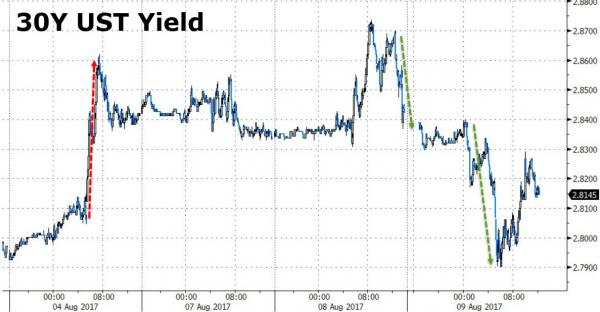

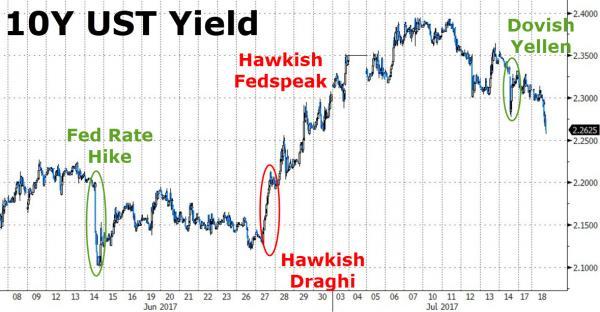

30 Year U.S. Treasury Bond Yield fall to 2.7972% then steadies at 2.7855%

(Chart courtesy of Zerohedge.com).

The 30 Year U.S. Treasury Bond has now extended its trading range to below 2.80% and may be presaging lower yields and a new lower trading range.

30 Year U.S. Treasury Bond Yield Testing lower range between 2.80% and 2.94%.

(Chart courtesy of Zerohedge.com).

At the extremes of this range buyers of long bonds can be counted on to appears in force when the 30 Year U.S. Treasury Yield moves to the top of this range around 2.94%; conversely, sellers come out when the yield falls to 2.80%.

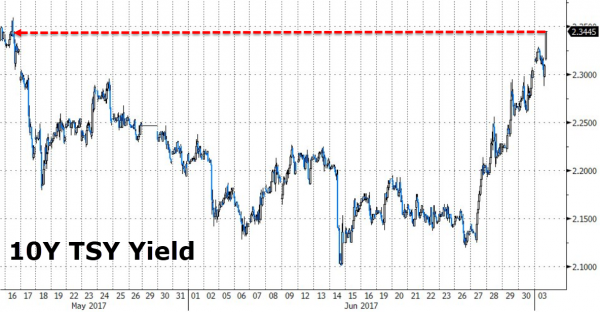

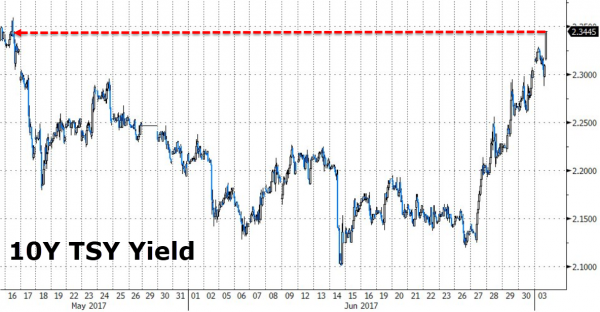

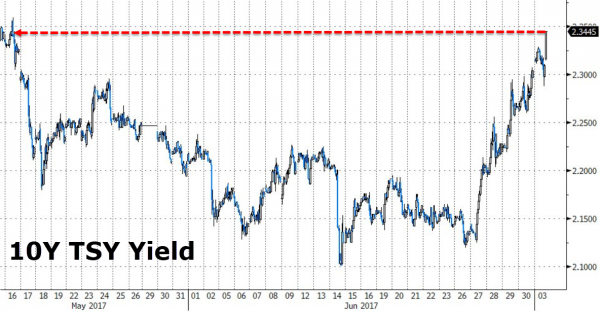

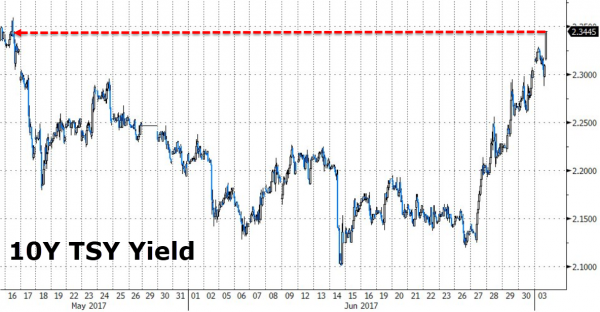

10 Year U.S. Treasury Note Yield Falls to 2.2212% then steadies at 2.1888%

(Chart courtesy of Zerohedge.com).

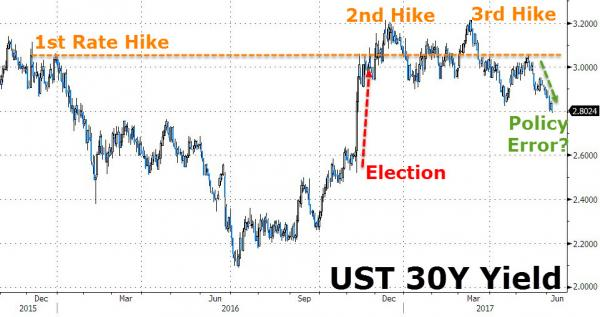

This gyration in bond yields looks like it wants to resolve itself by moving much lower into the gap that was formed post-election last November. If so, we will get another run at historically low rates before the final blow-off in Credit Markets sends Mortgage Interest rates up for good.

10 Year U.S. Treasury Note Yield Longer-term View back below 50-Day MA at 2.26%

(Chart courtesy of Zerohedge.com).

The above Chart does suggest that a constructive set-up is forming in the 10 Year Treasury Note with the potential to push the yield to around 2.00% over the next month. It is crucial that Mortgage Rates stay at or below 4.00% or demand for mortgage loans will dry up. The window of opportunity for borrowers seeking mortgage refinancing & home purchases is still open for now.

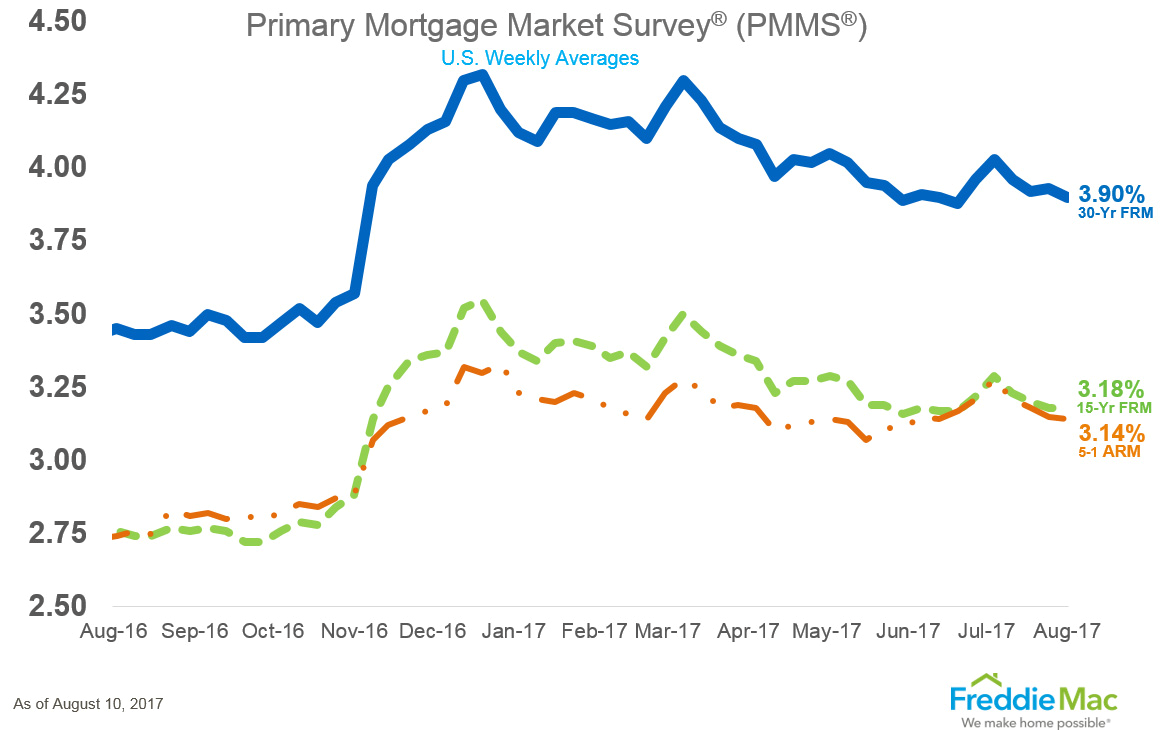

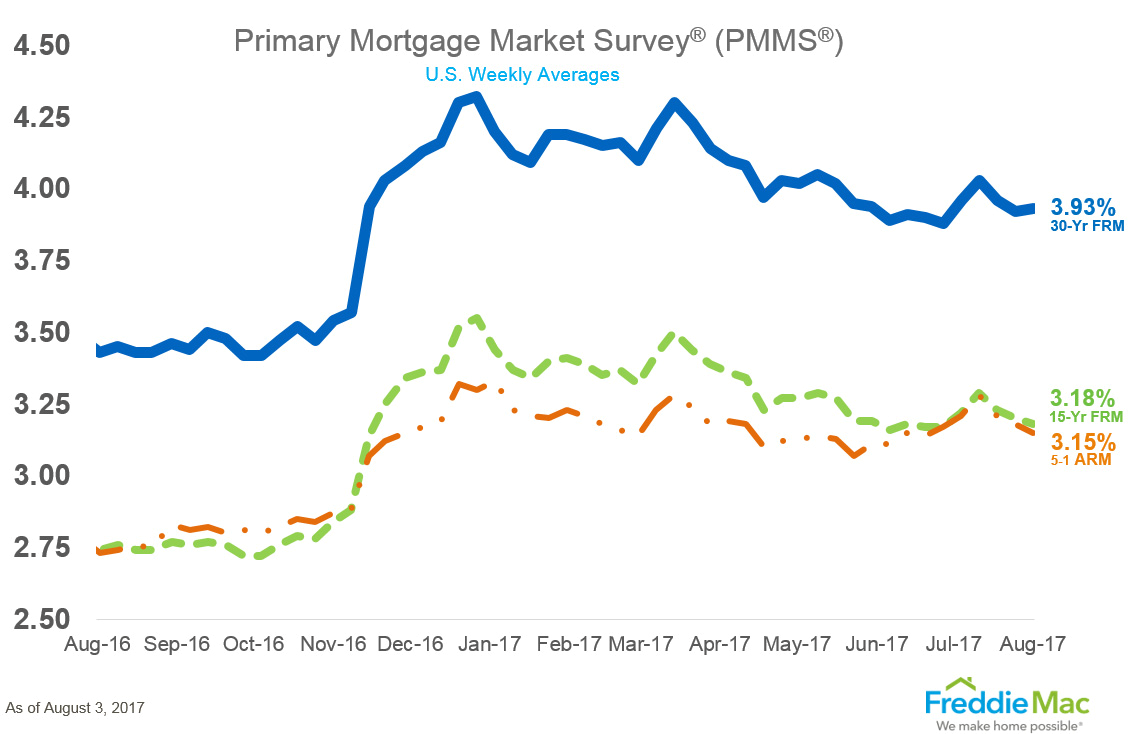

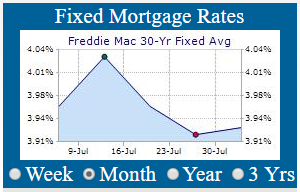

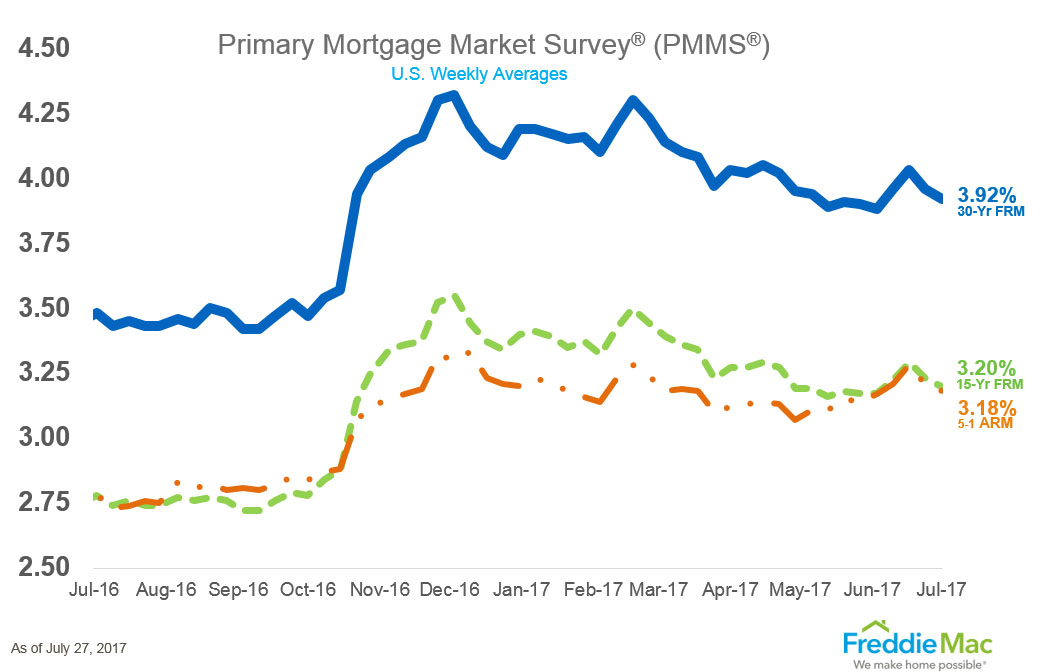

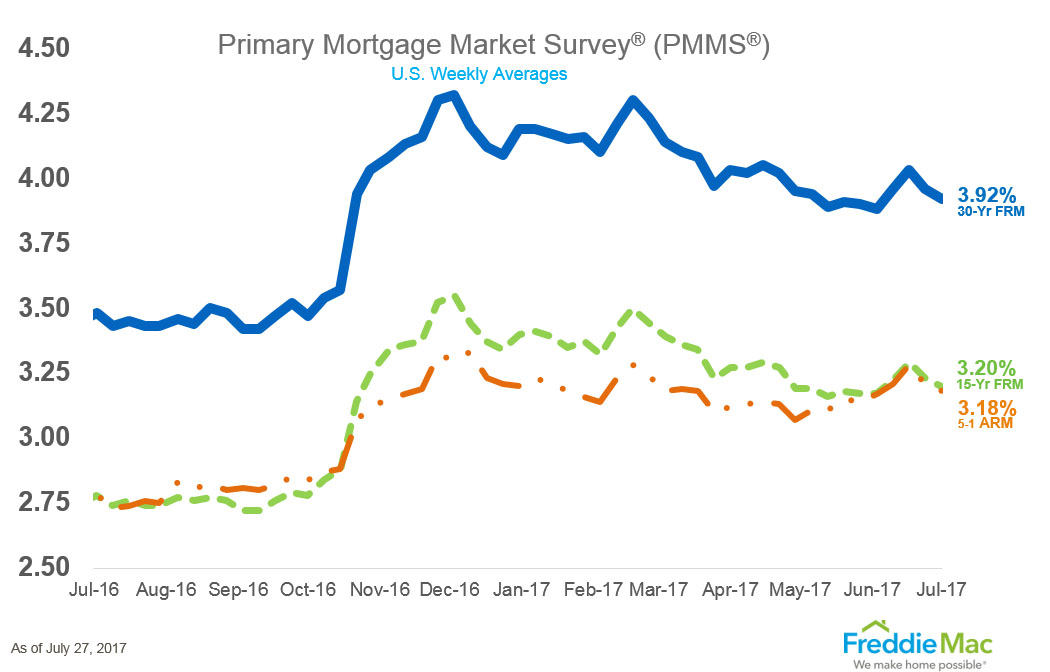

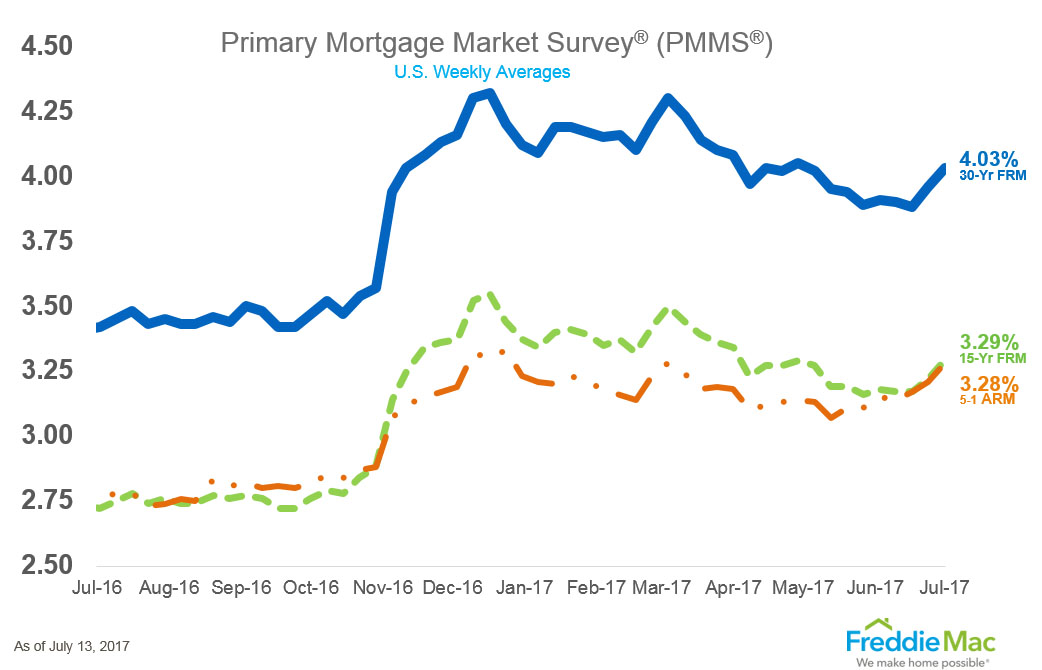

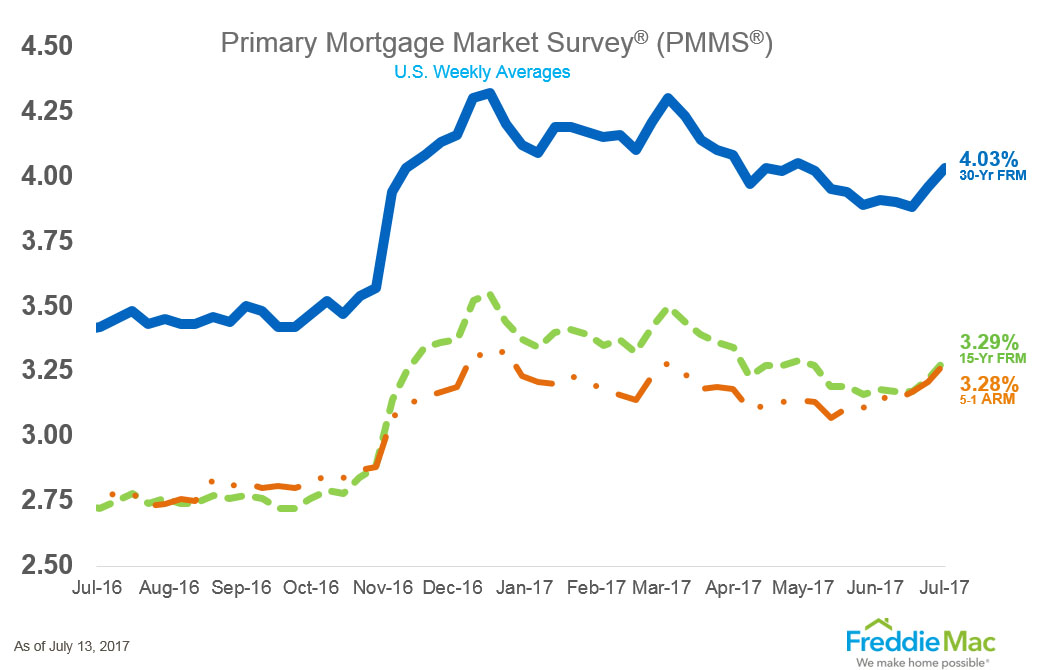

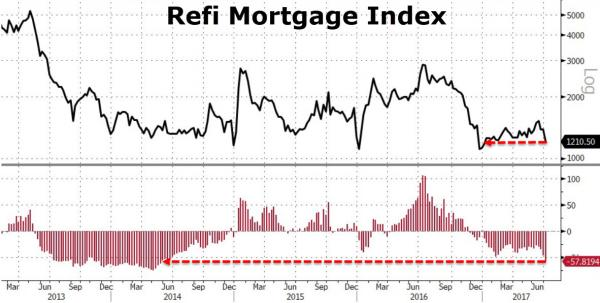

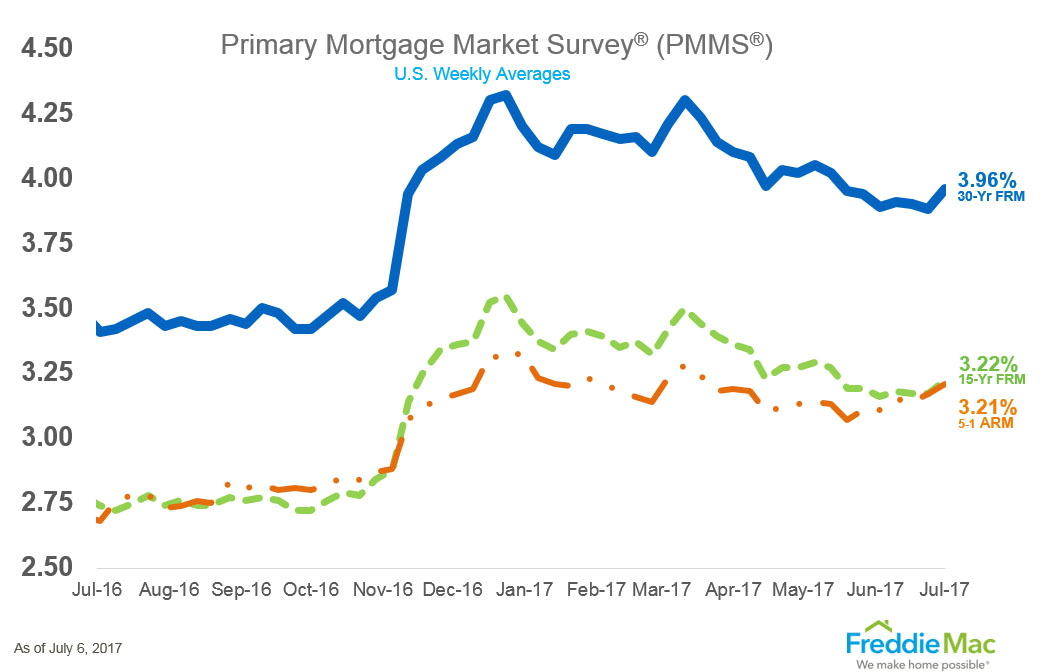

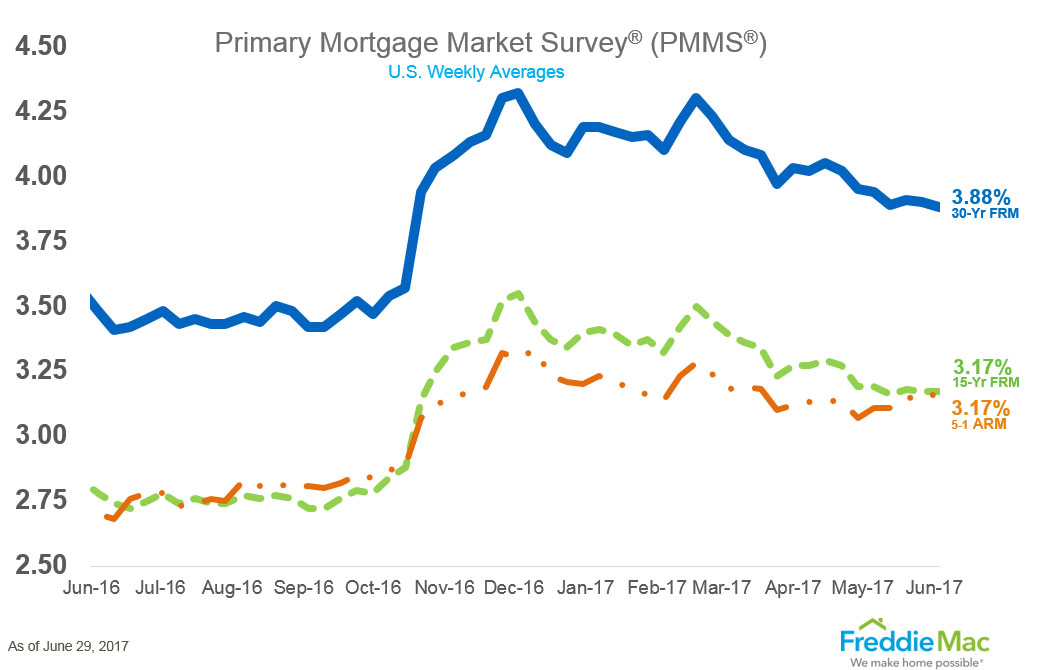

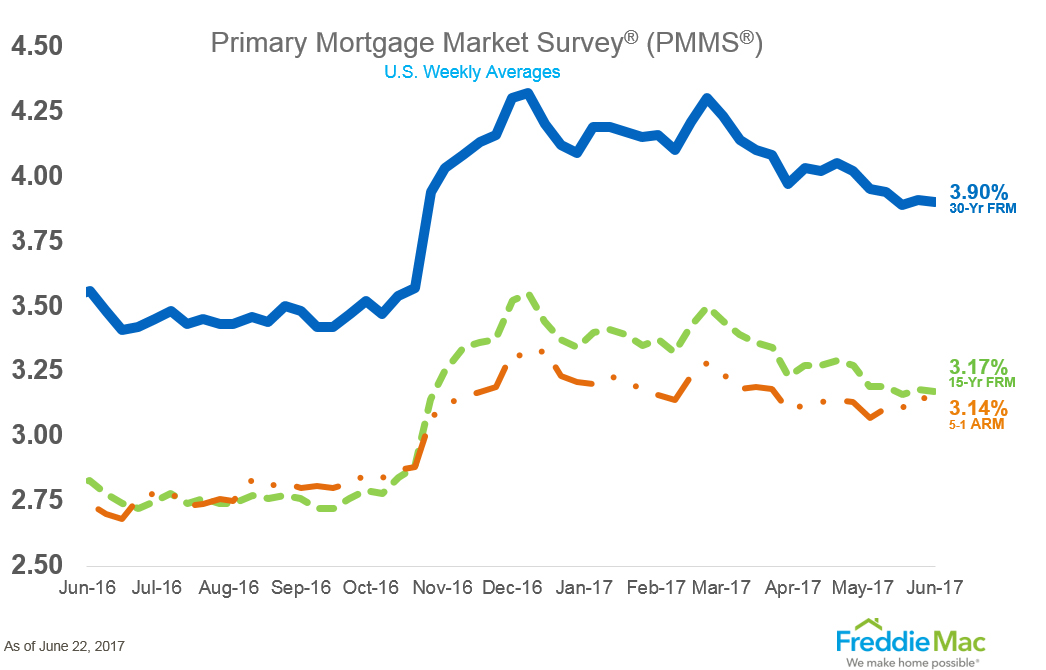

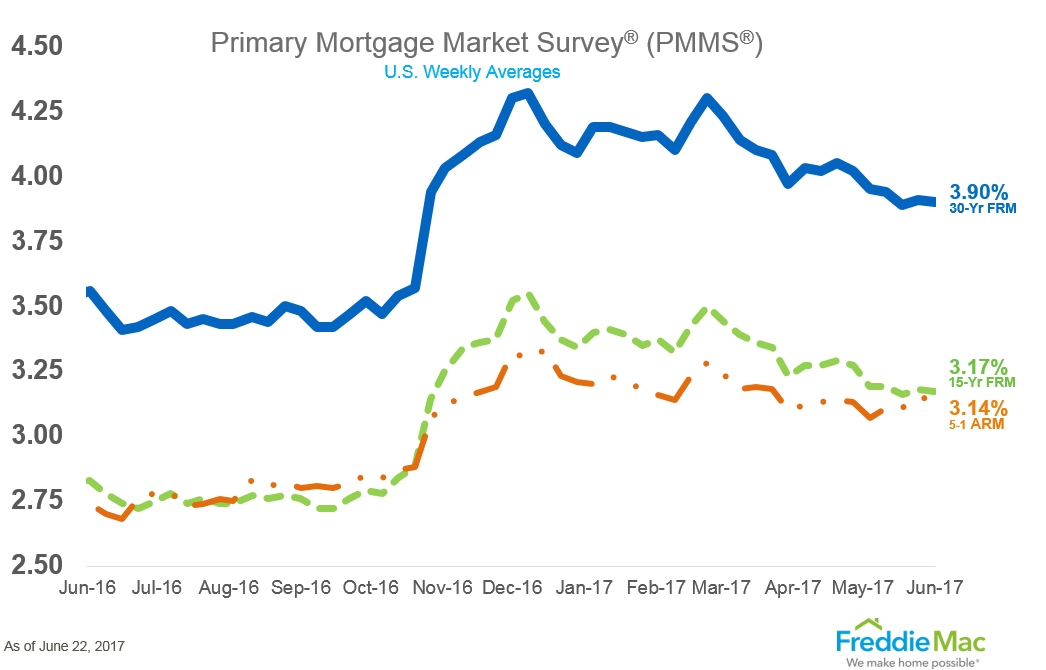

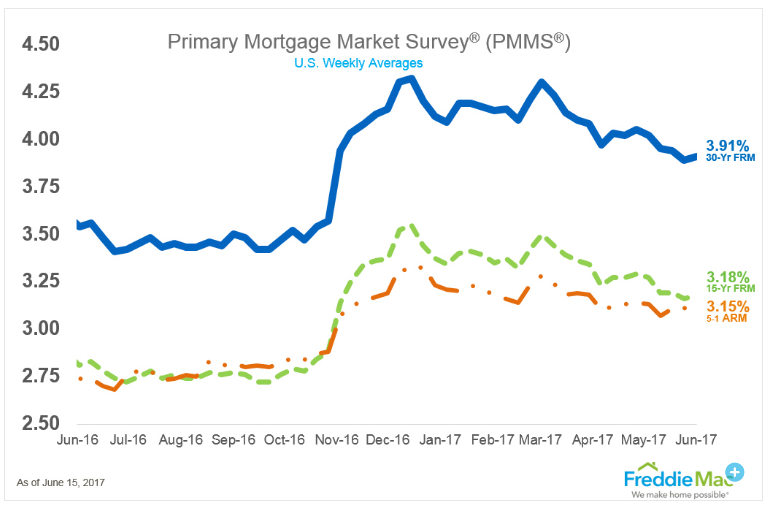

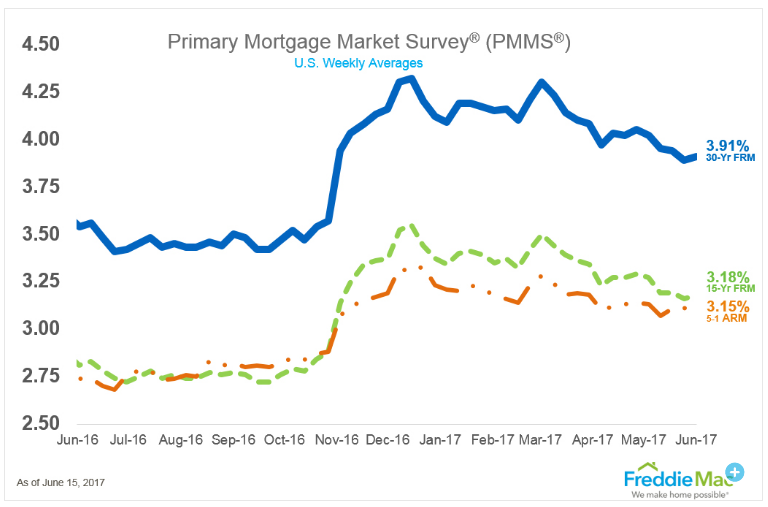

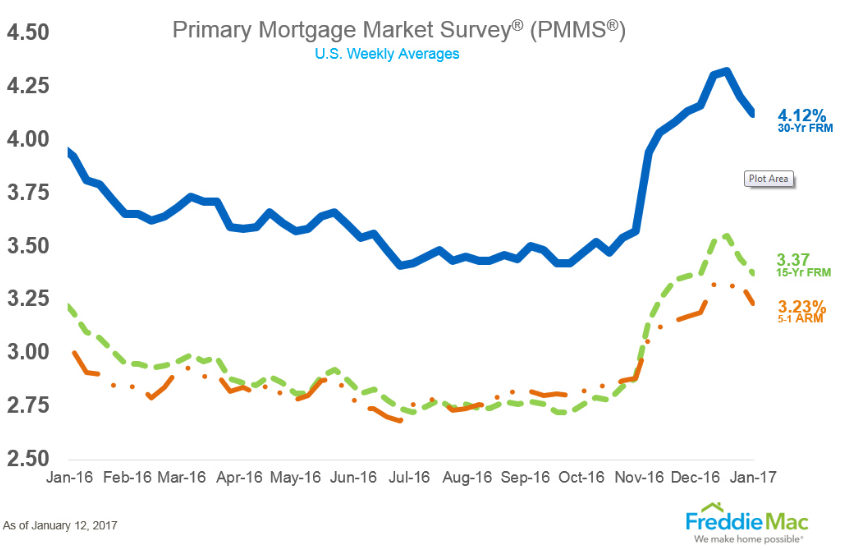

Weekly Mortgage Rates Analysis

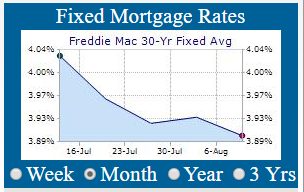

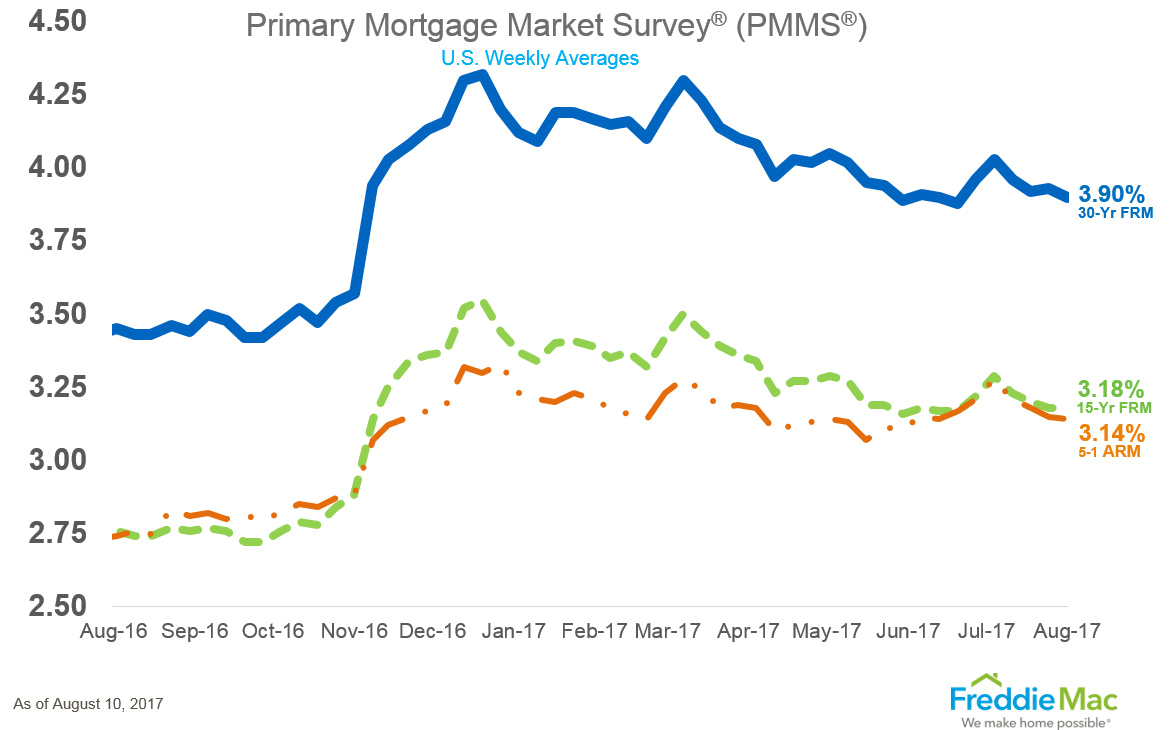

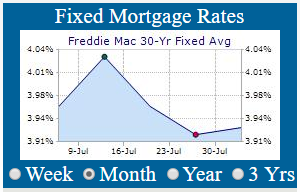

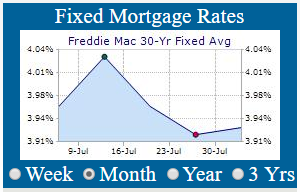

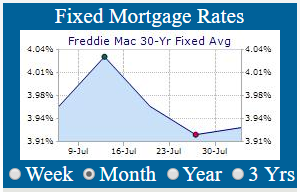

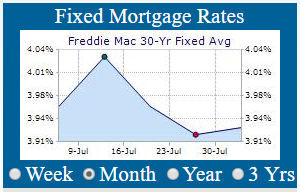

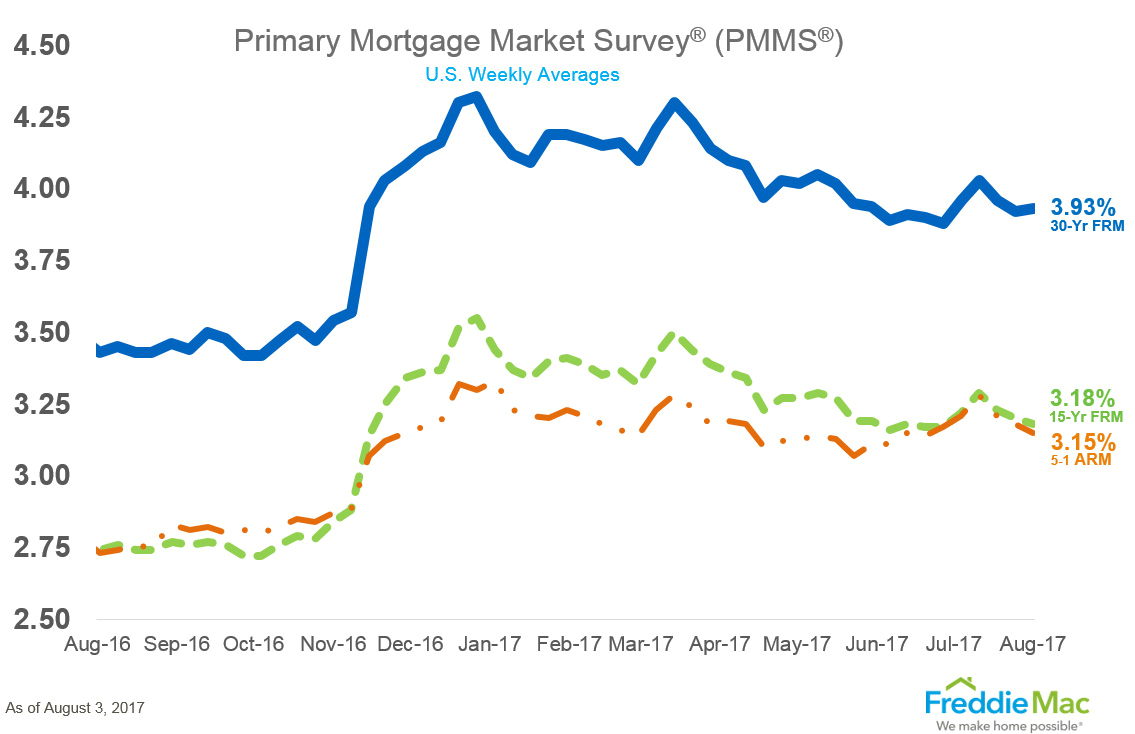

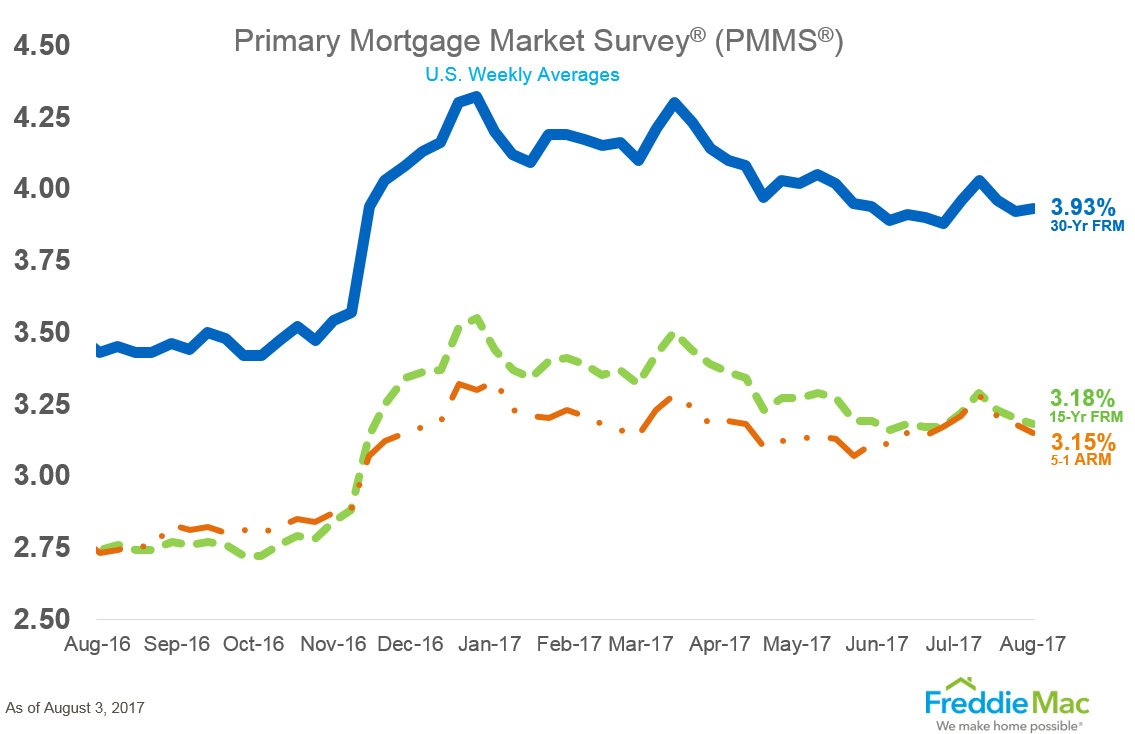

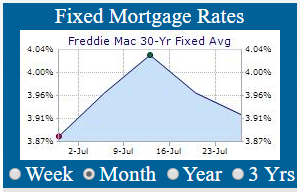

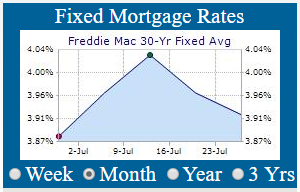

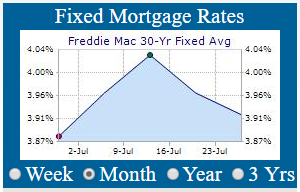

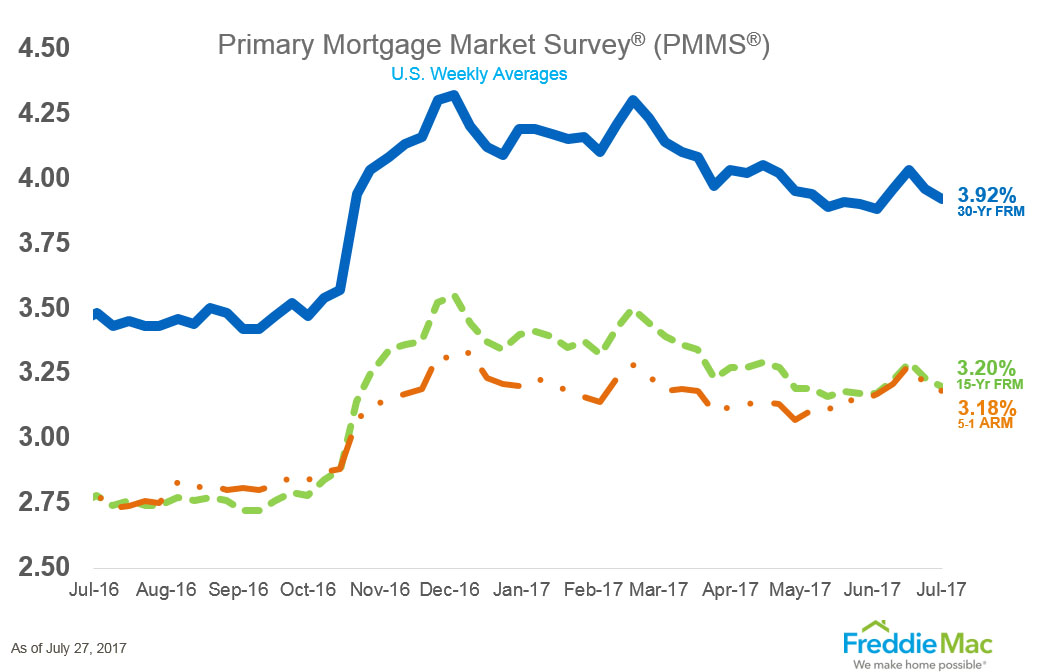

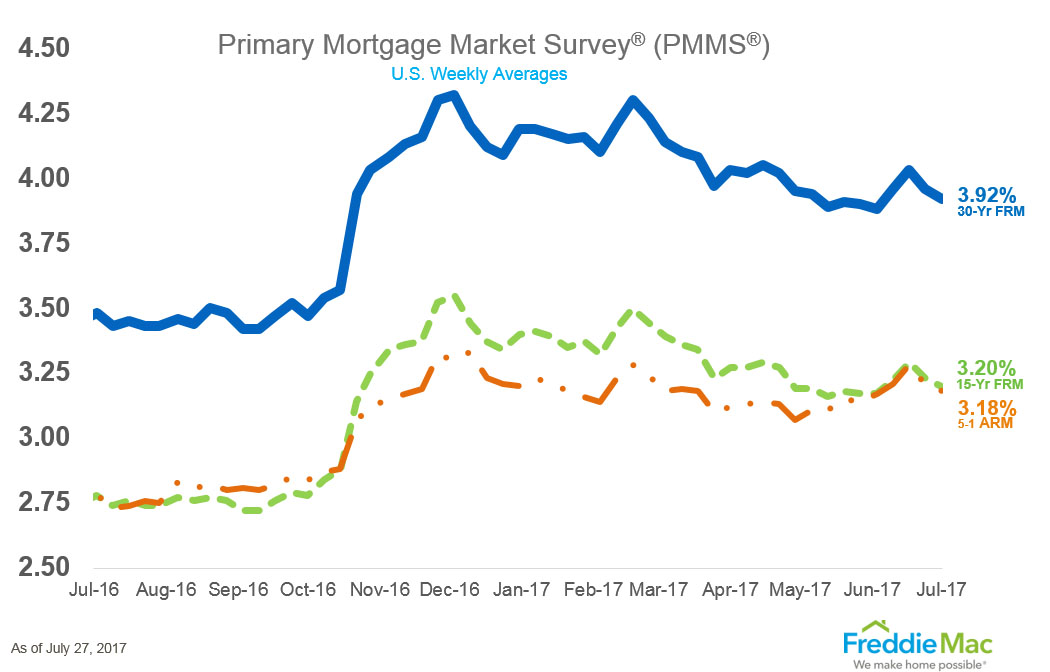

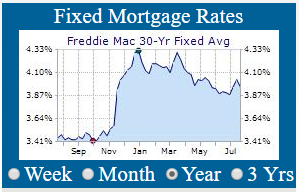

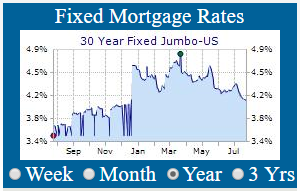

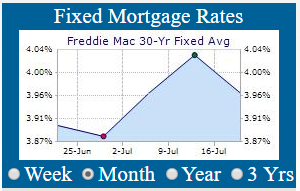

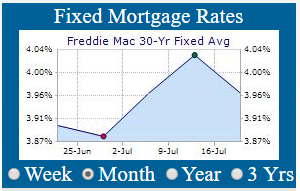

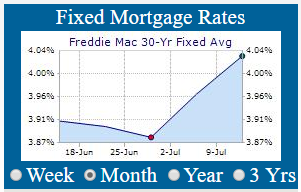

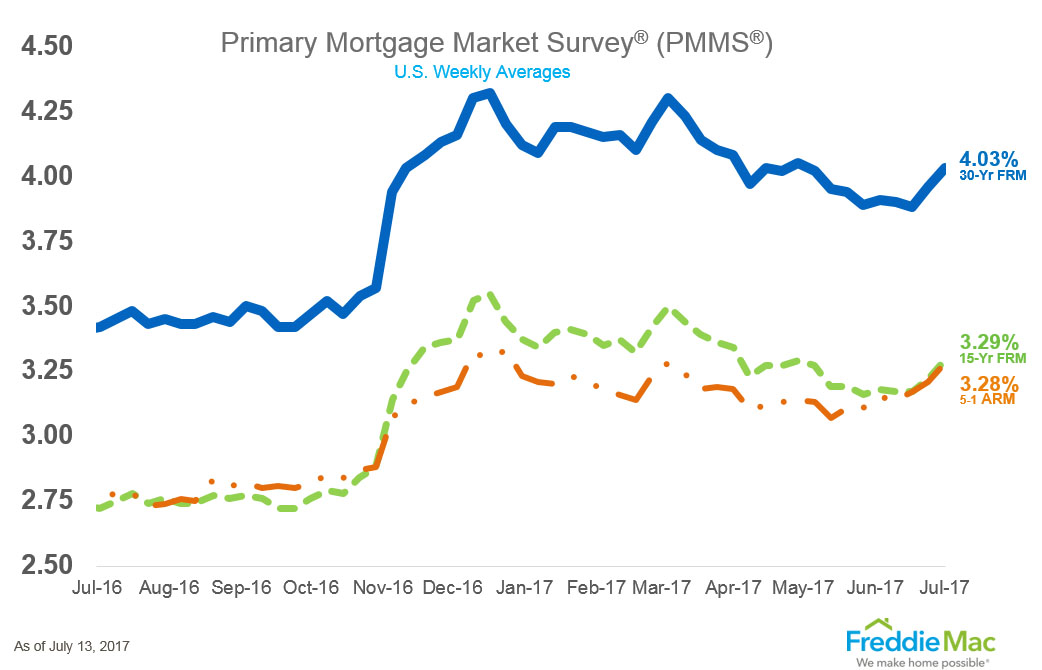

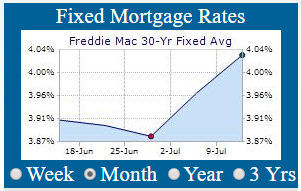

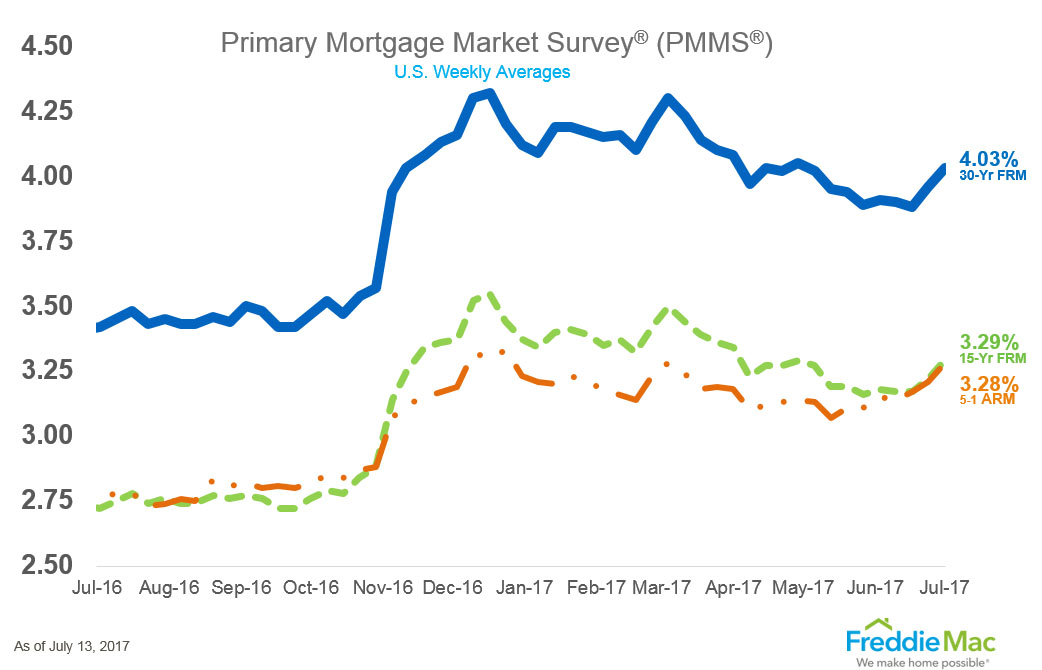

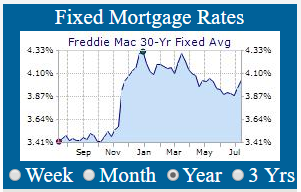

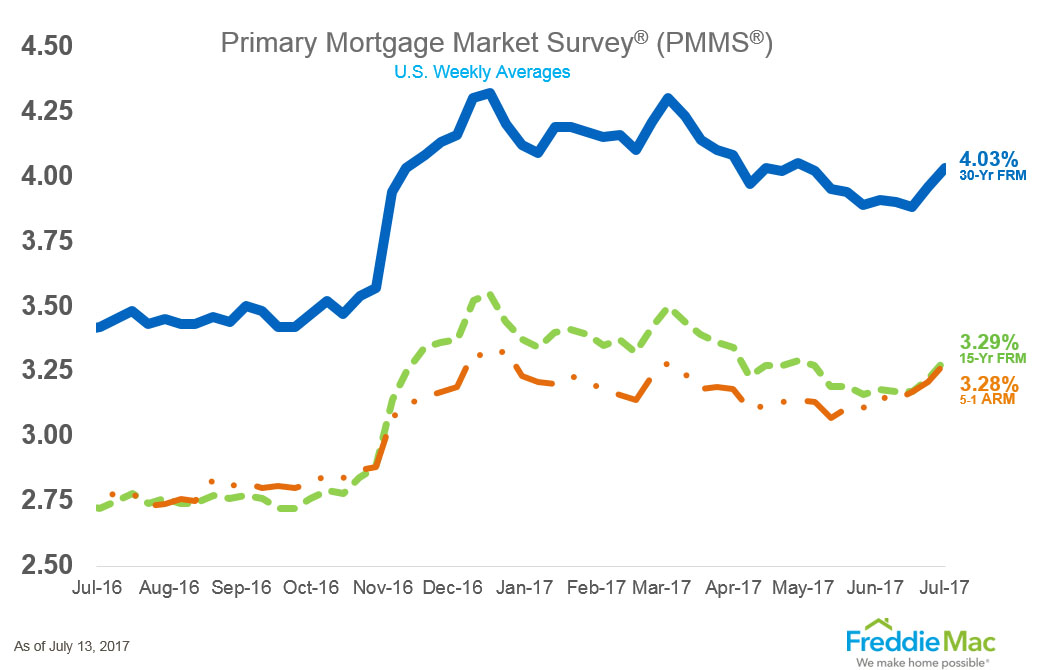

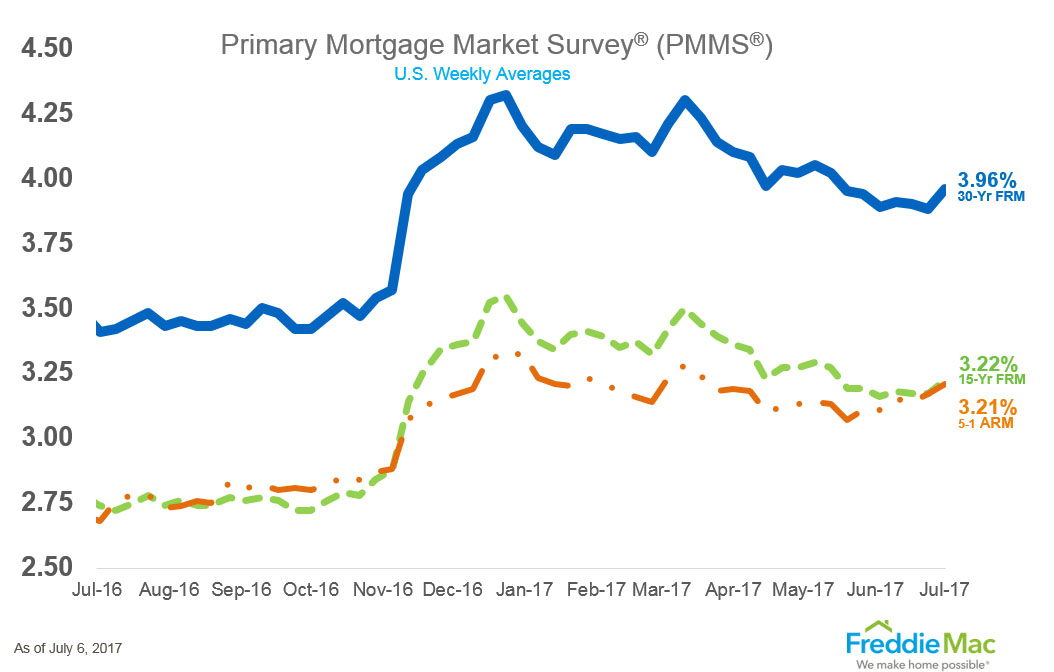

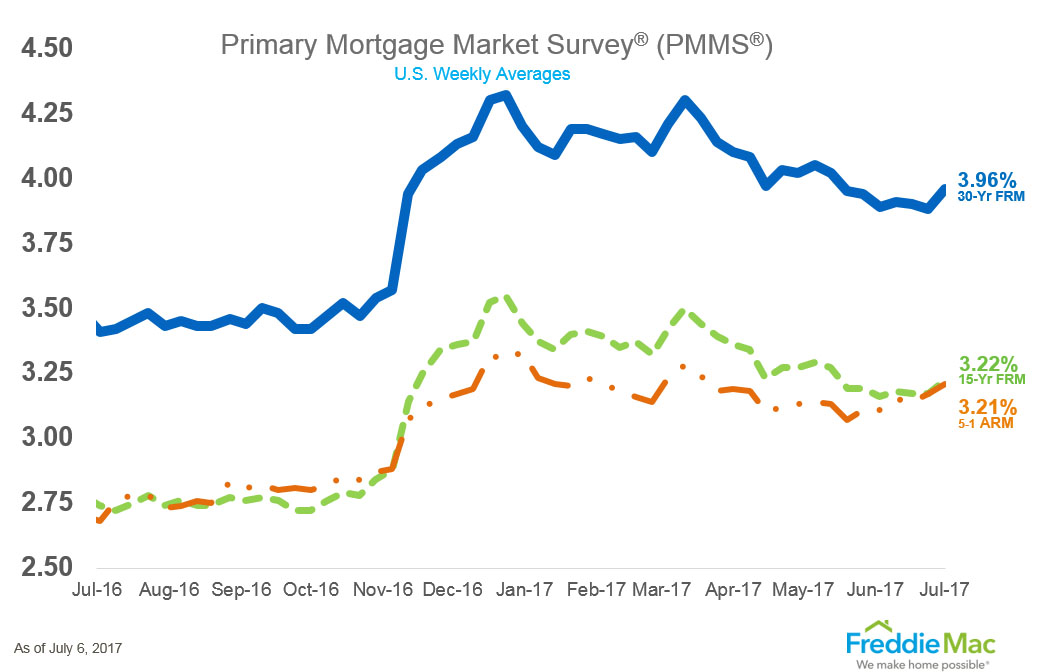

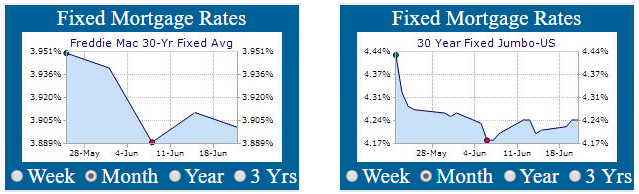

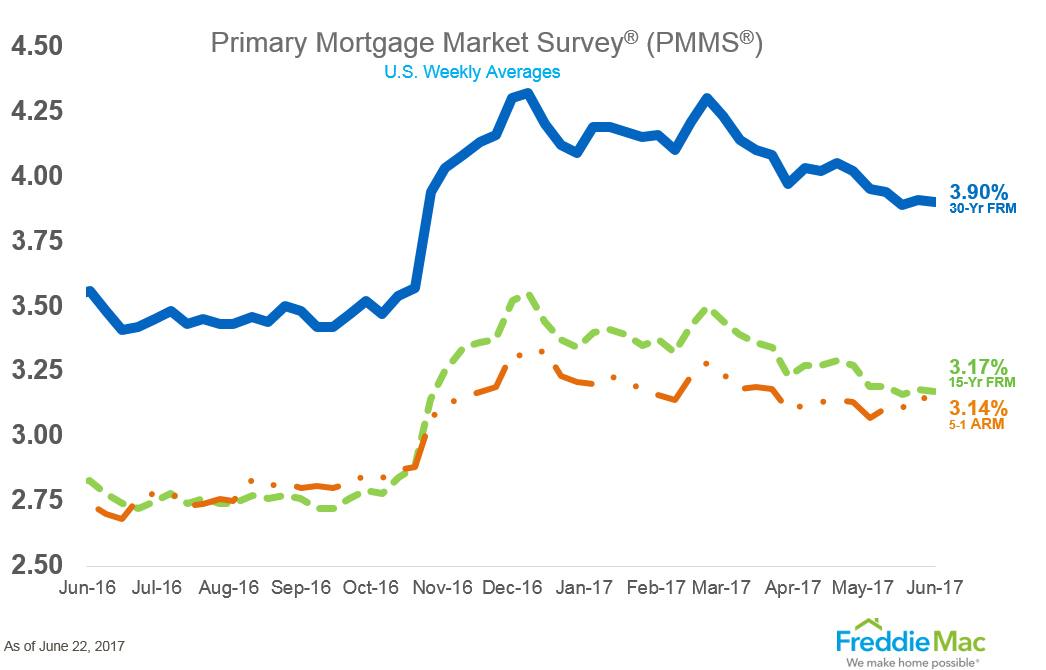

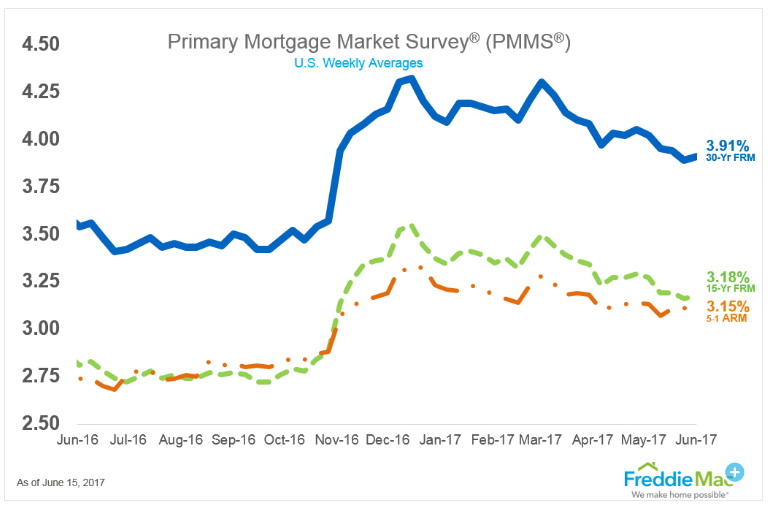

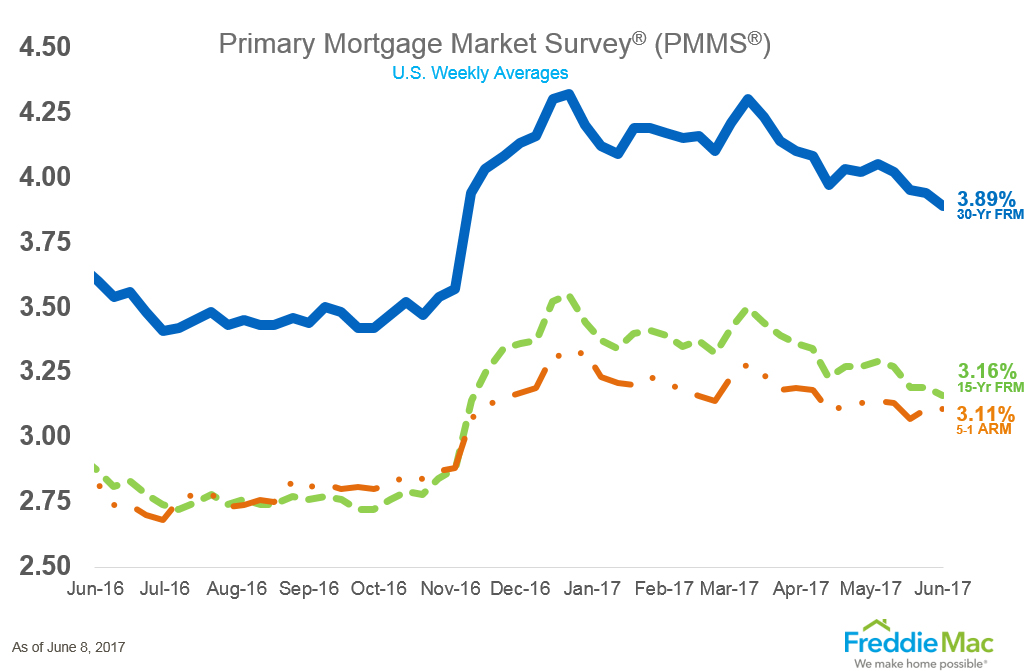

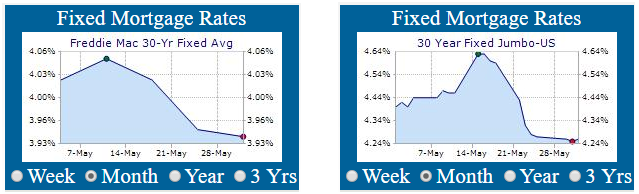

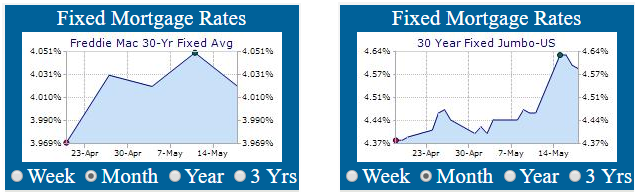

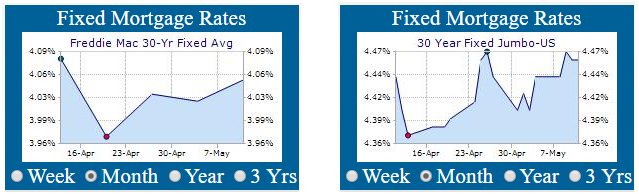

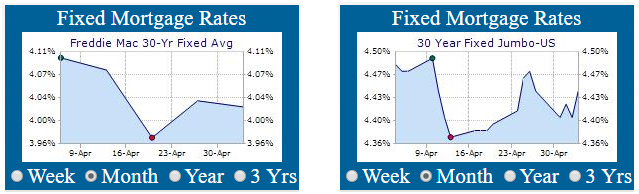

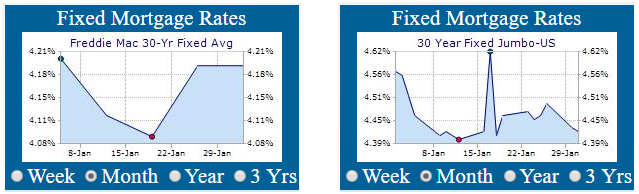

As can be seen from Freddie Mac’s Mortgage Market Survey, last week, 30 Yr. Fixed Mortgage rates for conforming loans hit 3.90% with the rate falling 0.03% basis points from the previous week.

Treasury Prices Rise and Yields Fall for U.S. 10 Yr. and 30 Yr. Treasuries.

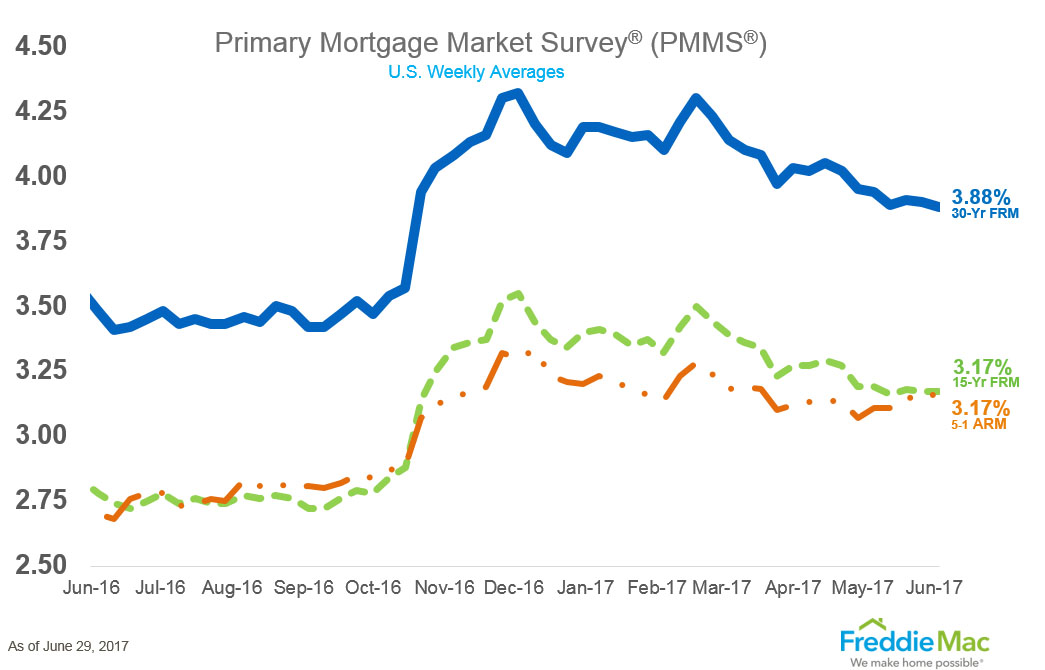

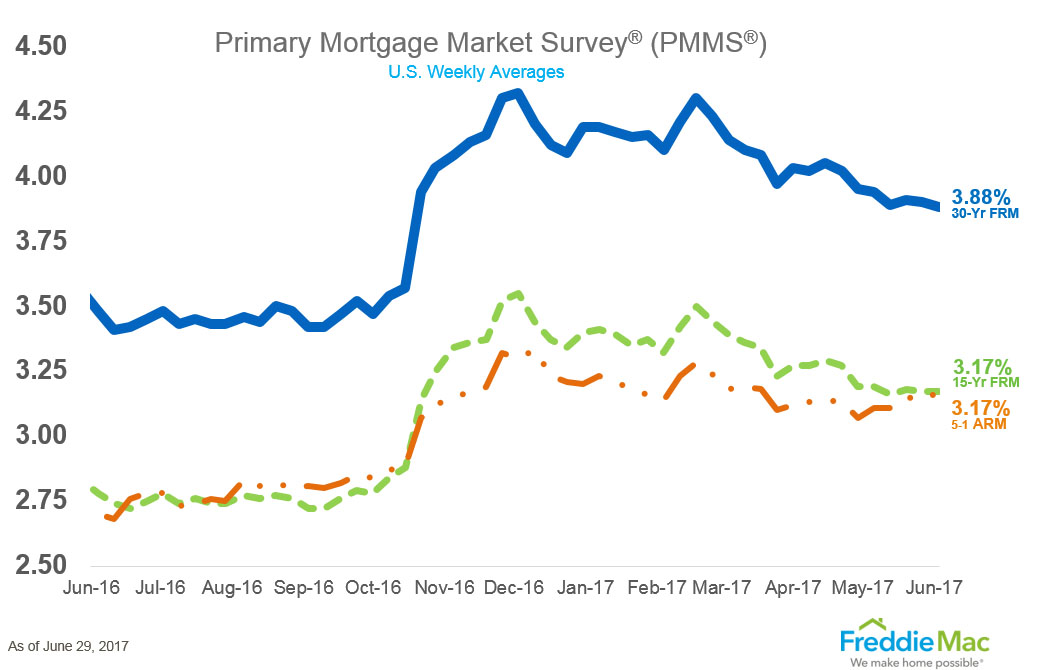

At the Chicago Board of Trade (CBOT): the US 10 Year Treasury Note futures Contract for September settlement closed at a price of 126’26 / 32nds; the 10 Year Note was up 8 basis points (bps) on the day, yielding 2.1888%. The US 30 Year Treasury Bond futures Contract for Sept. settlement closed at a price of 155’15 / 32nds; the 30 Year Bond was up 4 basis points (bps) on the day, yielding 2.7855%. Mortgage Rates have come off their 2017 lows and are down 0.03% bps from the previous Freddie Mac Survey last week.

Thanks to ZeroHedge.com, Goldman Sachs, Bloomberg.com, and FreddieMac.com for Charts and Graphics.

With the 30 year fixed rate mortgage, the interest rate remains the same from day one, meaning borrowers can depend on the same bill amount from month to month and year to year. For the 30-year term, borrowers pay down the principal, or actual loan amount, along with unchanging interest amount on the mortgage. Homeowners gradually increase equity in the home over time. A 30 year fixed-rate mortgage is often perfect for budgeting homeowners who wish to stay in the same house for a long time, but does have the drawback of paying more interest over the length of the loan compared with shorter-term loans.

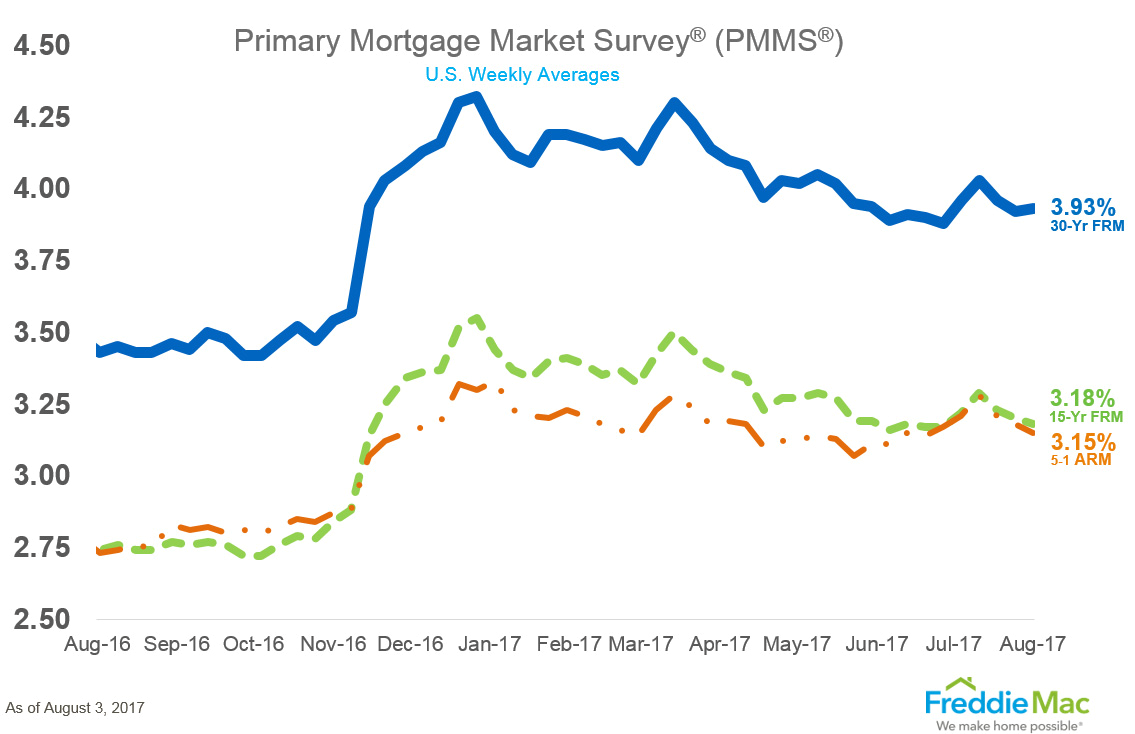

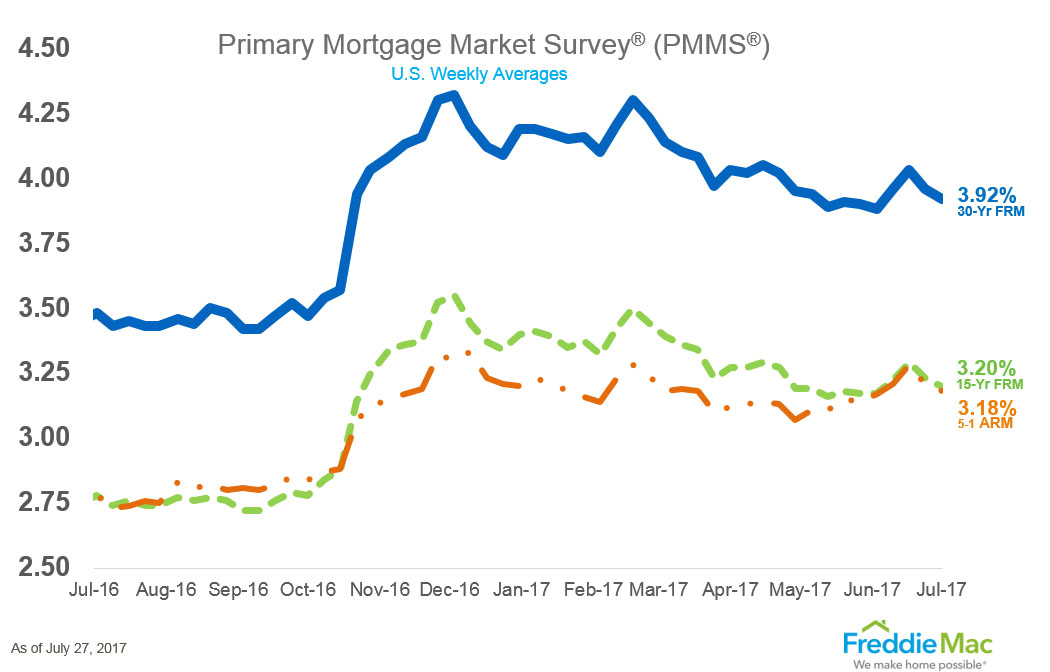

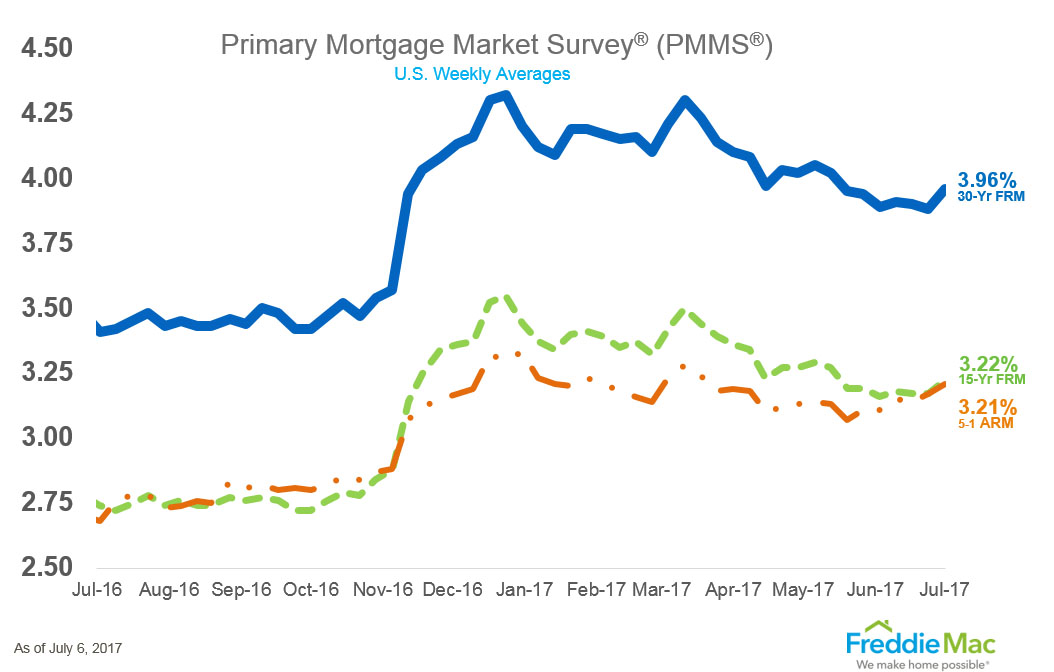

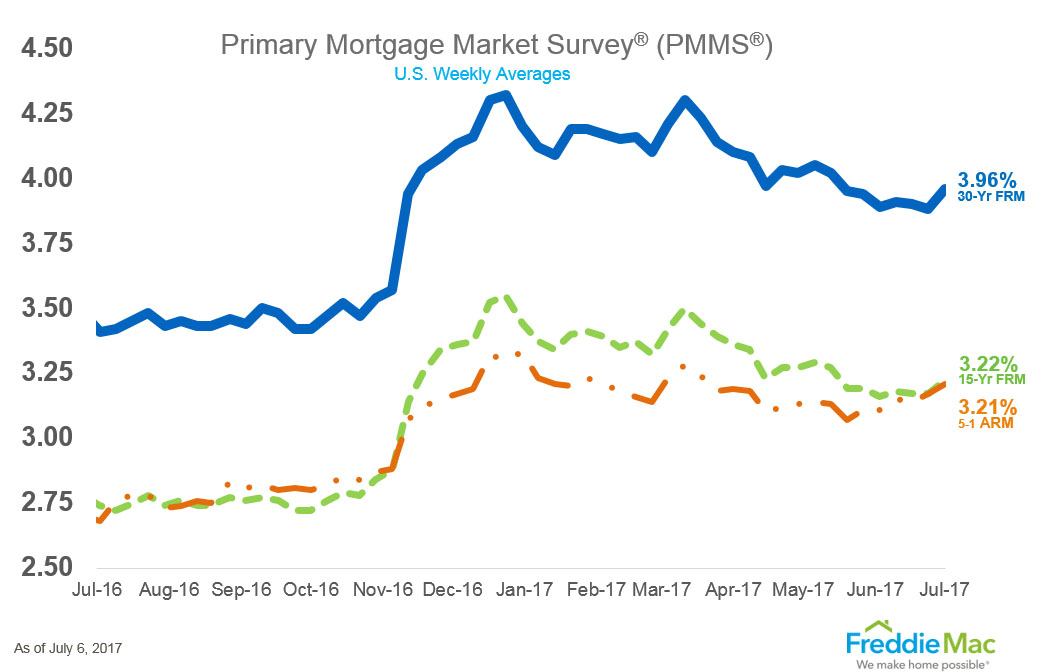

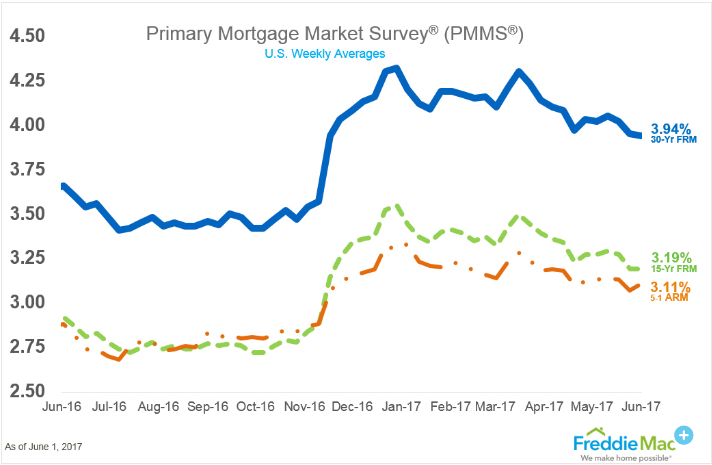

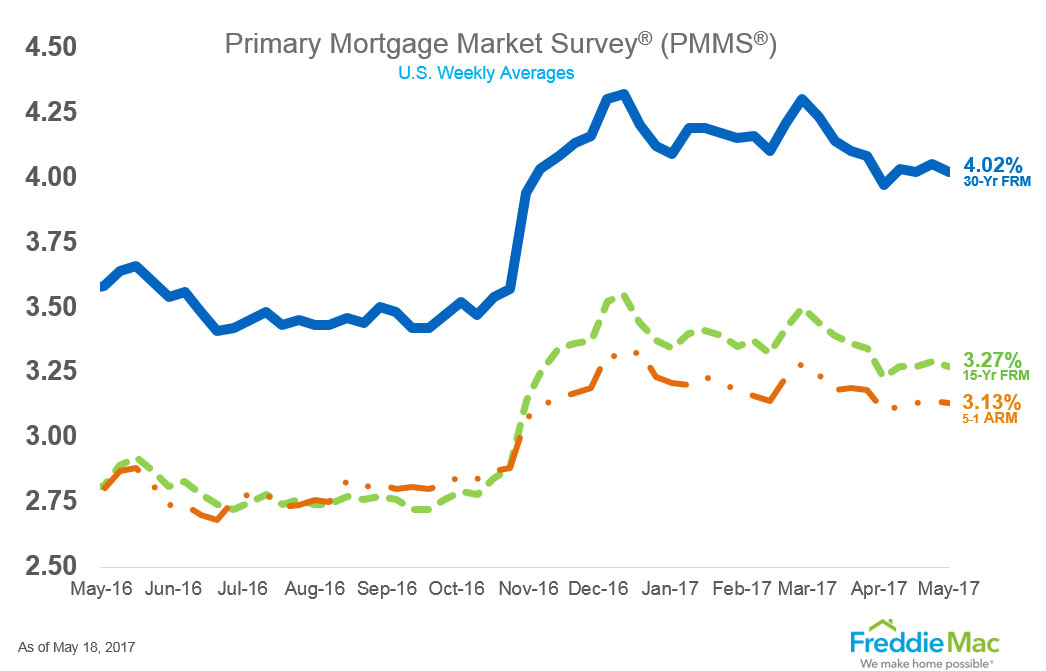

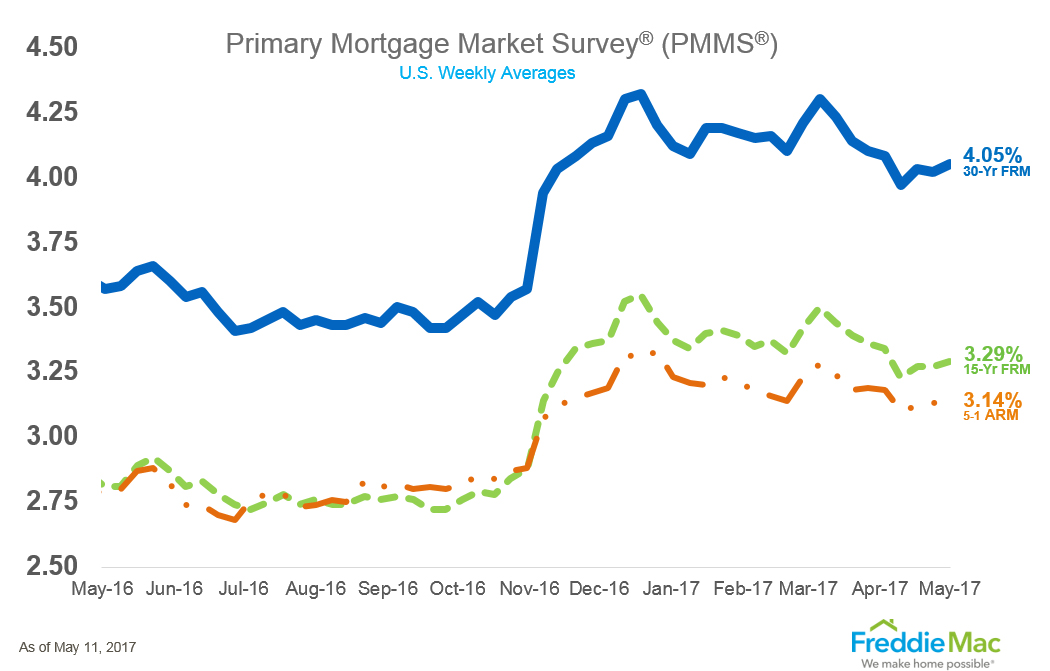

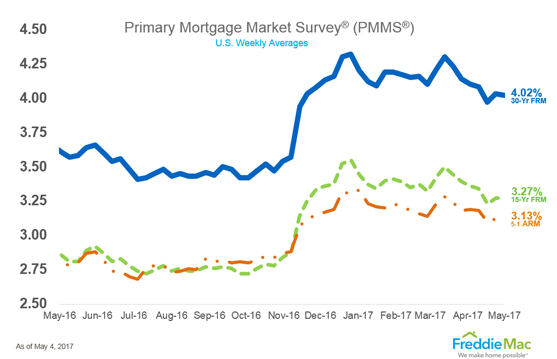

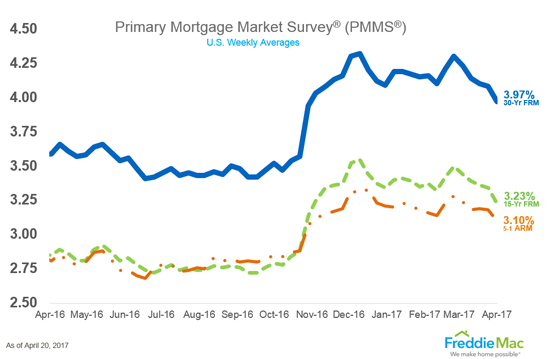

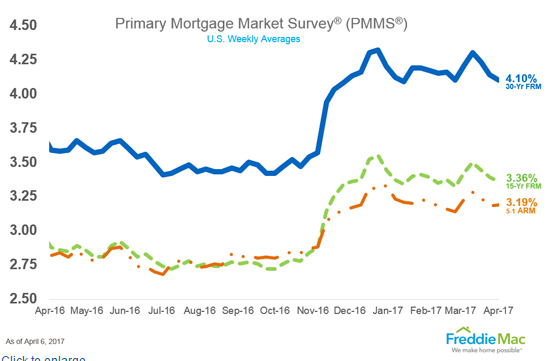

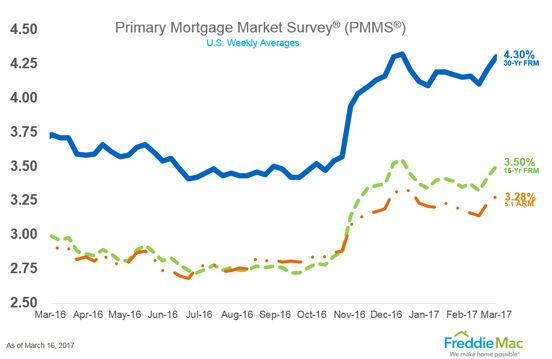

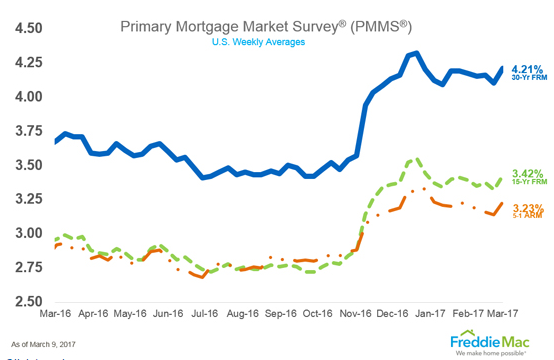

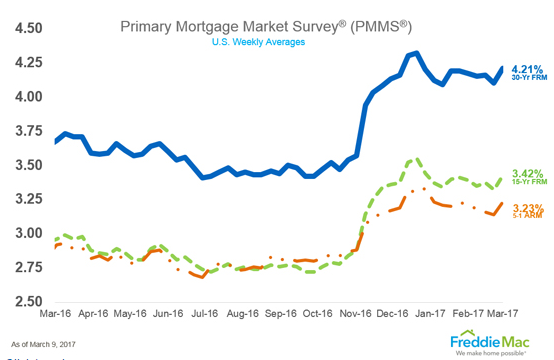

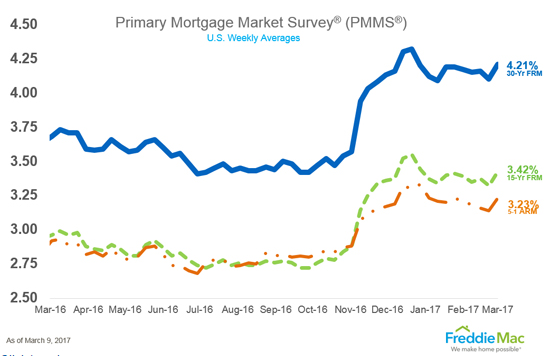

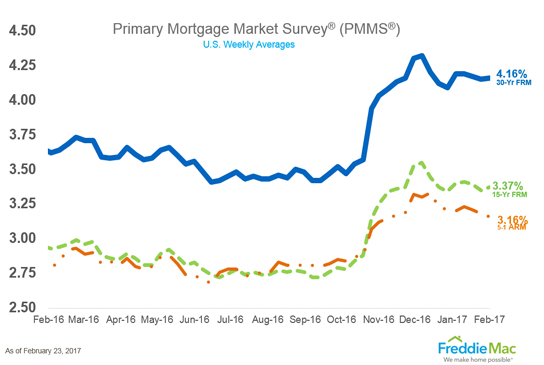

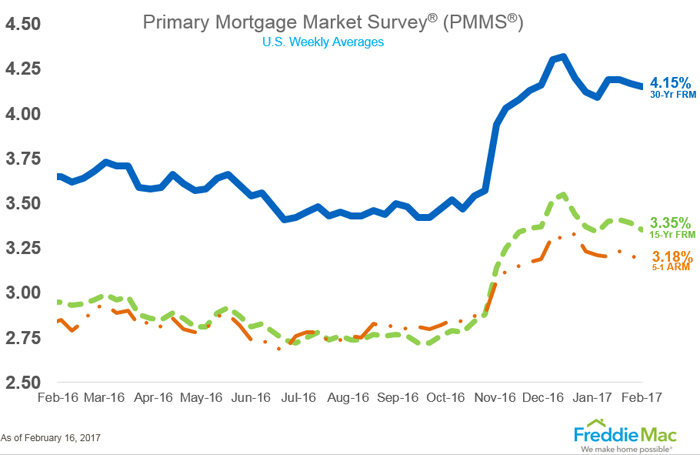

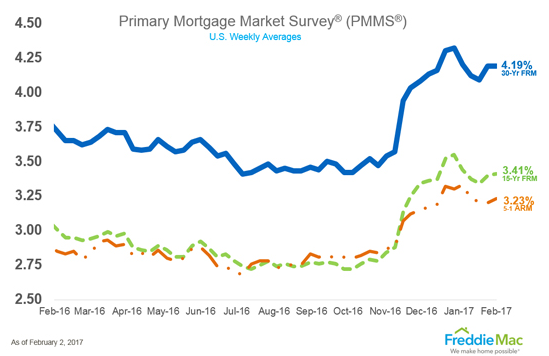

Freddie Mac Weekly Rate Summary

30-year fixed-rate mortgage (FRM) averaged 3.59 percent with an average 0.5 point for the week ending April 7, 2016, down from last week when they averaged 3.71 percent. A year ago at this time, the 30-year FRM averaged 3.66 percent.

15-year FRM this week averaged 2.88 percent with an average 0.4 point, down from last week when it averaged 2.98 percent. A year ago at this time, the 15-year FRM averaged 2.93 percent.

5-year Treasury-indexed hybrid adjustable-rate mortgage (ARM) averaged 2.82 percent this week with an average 0.5 point, down from last week when it averaged 2.90 percent. A year ago, the 5-year ARM averaged 2.83 percent.

ERATE's Daily Rate Summary

August 11, 2017

Mortgage Rates and Treasury Yields Fall.

On Thursday, Treasury bond yields and Mortgage interest rates fell as Credit Market participants bet on volatility and interest rate moderation in ‘quiet’ period in August. The September 10 Yr. U.S. Treasury Note stood at a yield of 2.1975% and the 30 Yr. U.S. Treasury Bond is yielding 2.7729%. 30 Year Mortgages according to Freddie Mac were around 3.90% for conforming and 4.10% for Jumbo products.

The Commerce Department released Core Consumer Price Index and the reading came in at 1.7% below the hoped for 2.00% inflation target the Fed was expecting. On the heels of 'disappointing' (to some) producer price data, consumer prices missed expectations for the 5th month in a row with a mere 0.1% rise MoM (0.2% exp). Year-over-year growth in core consumer prices also slowed for the 7th straight month dropping to just 1.7% - the slowest since Jan 2015. Amid this dismal report, there is a silver lining for Americans, the cost of shelter rose just 0.1% - the smallest rise since March.

Core Consumer Price Index Falls to 1.70% (YoY)

(Chart courtesy of Zerohedge.com).

This is an unwelcome signpost for Central Planners trying desperately to conjure some inflationary ‘animal spirits’ to assist them in their interest rate raising & balance sheet normalization policy trip.

30 Year U.S. Treasury Bond Yield fall to 2.7972% then steadies at 2.7729%

(Chart courtesy of Zerohedge.com).

The 30 Year U.S. Treasury Bond is now expanded its trading range between 2.80% and 2.94%; as market participants try to guess whether we get a manufacturing recovery this summer or we dip back into recession in the real-goods producing sector of the economy.

30 Year U.S. Treasury Bond Yield Rangebound between 2.80% and 2.94%.

(Chart courtesy of Zerohedge.com).

At the extremes of this range buyers of long bonds can be counted on to appears in force when the 30 Year U.S. Treasury Yield moves to the top of this range around 2.94%; conversely, sellers come out when the yield falls to 2.80%.

10 Year U.S. Treasury Note Yield Falls to 2.2212% then steadies at 2.1975%

(Chart courtesy of Zerohedge.com).

This gyration in bond yields looks like it wants to resolve itself by moving much lower into the gap that was formed post-election last November. If so, we will get another run at historically low rates before the final blow-off in Credit Markets sends Mortgage Interest rates up for good.

10 Year U.S. Treasury Note Yield Longer-term View back below 50-Day MA at 2.26%

(Chart courtesy of Zerohedge.com).

The above Chart does suggest that a constructive set-up is forming in the 10 Year Treasury Note with the potential to push the yield to around 2.00% over the next month. It is crucial that Mortgage Rates stay at or below 4.00% or demand for mortgage loans will dry up. The window of opportunity for borrowers seeking mortgage refinancing & home purchases is still open for now.

Weekly Mortgage Rates Analysis

As can be seen from Freddie Mac’s Mortgage Market Survey, last week, 30 Yr. Fixed Mortgage rates for conforming loans hit 3.90% with the rate falling 0.03% basis points from the previous week.

Treasury Prices Rise and Yields Fall for U.S. 10 Yr. and 30 Yr. Treasuries.

At the Chicago Board of Trade (CBOT): the US 10 Year Treasury Note futures Contract for September settlement closed at a price of 126’18 / 32nds; the 10 Year Note was up 7 basis points (bps) on the day, yielding 2.1975%. The US 30 Year Treasury Bond futures Contract for Sept. settlement closed at a price of 155’11 / 32nds; the 30 Year Bond was up 20 basis points (bps) on the day, yielding 2.7729%. Mortgage Rates have come off their 2017 lows and are down 0.03% bps from the previous Freddie Mac Survey last week.

Thanks to ZeroHedge.com, Commerce Department, Bloomberg.com, and FreddieMac.com for Charts and Graphics.

ERATE's Daily Rate Summary

August 10, 2017

Mortgage Rates and Treasury Yields Fall.

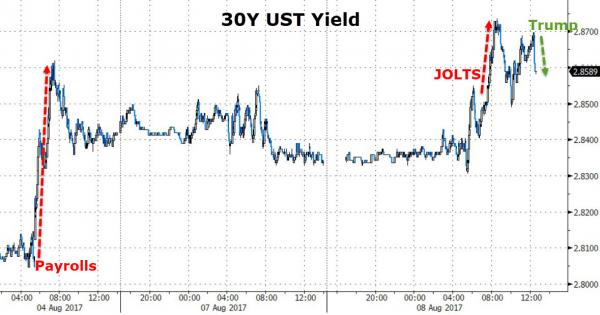

On Wednesday, Treasury bond yields and Mortgage interest rates fell as Credit Market participants bet on volatility and interest rate moderation in ‘quiet’ period in August. The September 10 Yr. U.S. Treasury Note stood at a yield of 2.2476% and the 30 Yr. U.S. Treasury Bond is yielding 2.8222%. 30 Year Mortgages according to Freddie Mac were around 3.90% for conforming and 4.10% for Jumbo products.

The Bond market continues to improve day by day and mortgage rates continue to improve slowly. The Credit Markets are in a lull before the Jackson Hole Symposium slated for August 21st to 24th. The key speaker of note will be Mario Draghi ECB President and he is expected to speak about the timetable for eventually tapering the ECB Corporate Bond Purchase program & tightening European credit conditions to reflect the EU recovery. Also, Janet Yellen Fed President should have words outlining the Fed’s plan to normalize their $4.5 Trillion Balance Sheet and path of Fed Funds Rate increases going forward and interest rates in general.

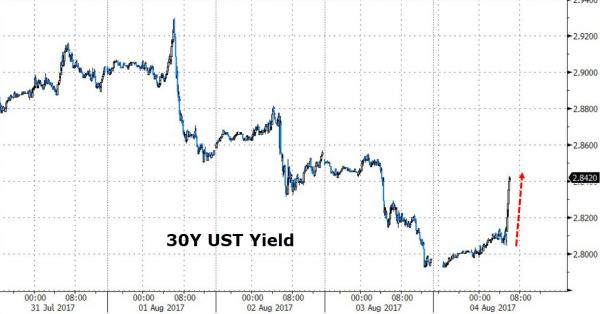

30 Year U.S. Treasury Bond Yield fall to 2.7972% then steadies at 2.8222%

(Chart courtesy of Zerohedge.com).

The 30 Year U.S. Treasury Bond is now expanded its trading range between 2.80% and 2.94%; as market participants try to guess whether we get a manufacturing recovery this summer or we dip back into recession in the real-goods producing sector of the economy.

30 Year U.S. Treasury Bond Yield Rangebound between 2.80% and 2.94%.

(Chart courtesy of Zerohedge.com).

At the extremes of this range buyers of long bonds can be counted on to appears in force when the 30 Year U.S. Treasury Yield moves to the top of this range around 2.94%; conversely, sellers come out when the yield falls to 2.80%.

10 Year U.S. Treasury Note Yield Falls to 2.2212% then steadies at 2.2476%

(Chart courtesy of Zerohedge.com).

This gyration in bond yields looks like it wants to resolve itself by moving much lower into the gap that was formed post-election last November. If so, we will get another run at historically low rates before the final blow-off in Credit Markets sends Mortgage Interest rates up for good.

10 Year U.S. Treasury Note Yield Longer-term View back below 50-Day MA at 2.26%

(Chart courtesy of Zerohedge.com).

The above Chart does suggest that a constructive set-up is forming in the 10 Year Treasury Note with the potential to push the yield to around 2.00% over the next month. It is crucial that Mortgage Rates stay at or below 4.00% or demand for mortgage loans will dry up. The window of opportunity for borrowers seeking mortgage refinancing & home purchases is still open for now.

Weekly Mortgage Rates Analysis

As can be seen from Freddie Mac’s Mortgage Market Survey, last week, 30 Yr. Fixed Mortgage rates for conforming loans hit 3.90% with the rate falling 0.03% basis points from the previous week.

Treasury Prices Rise and Yields Fall for U.S. 10 Yr. and 30 Yr. Treasuries.

At the Chicago Board of Trade (CBOT): the US 10 Year Treasury Note futures Contract for September settlement closed at a price of 126’11 / 32nds; the 10 Year Note was up 11 basis points (bps) on the day, yielding 2.2476%. The US 30 Year Treasury Bond futures Contract for Sept. settlement closed at a price of 154’23 / 32nds; the 30 Year Bond was up 32 basis points (bps) on the day, yielding 2.8222%. Mortgage Rates have come off their 2017 lows and are down 0.03% bps from the previous Freddie Mac Survey last week.

Thanks to ZeroHedge.com, Bureau of Labor Statistics, Bloomberg.com, and FreddieMac.com for Charts and Graphics.

ERATE's Daily Rate Summary

August 9, 2017

Mortgage Rates and Treasury Yields Rise.

On Tuesday, Treasury bond yields and Mortgage interest rates rose as Credit Market participants bet on volatility and interest rate moderation in ‘quiet’ period in August. The September 10 Yr. U.S. Treasury Note stood at a yield of 2.2619% and the 30 Yr. U.S. Treasury Bond is yielding 2.8428%. 30 Year Mortgages according to Freddie Mac were around 3.93% for conforming and 4.09% for Jumbo products.

The Bond market continues to improve day by day and mortgage rates continue to improve slowly. The economy is not lifting off as anticipated (this is the seventh summer of recovery in a row) and I’m not buying it. The CB’s with all their talk, emergency measures, cheerleading, QE, ZIRP, and NIRP must have missed an important fundamental economic linkage in the monetary policy transmission mechanism; because at the base of it all folks are broke and cannot increase their spending with the income available to them. Inflation is not happening in an economy this mature and indebted, we are going to grind slowly down to a crawl and then stop. That’s when the fun begins!

30 Year U.S. Treasury Bond Yield fall to 2.7972% then steadies at 2.8428%

(Chart courtesy of Zerohedge.com).

The 30 Year U.S. Treasury Bond is now expanded its trading range between 2.80% and 2.94%; as market participants try to guess whether we get a manufacturing recovery this summer or we dip back into recession in the real-goods producing sector of the economy.

30 Year U.S. Treasury Bond Yield Rangebound between 2.80% and 2.94%.

(Chart courtesy of Zerohedge.com).

At the extremes of this range buyers of long bonds can be counted on to appears in force when the 30 Year U.S. Treasury Yield moves to the top of this range around 2.94%; conversely, sellers come out when the yield falls to 2.80%.

10 Year U.S. Treasury Note Yield Falls to 2.2212% then steadies at 2.2619%

(Chart courtesy of Zerohedge.com).

This gyration in bond yields looks like it wants to resolve itself by moving much lower into the gap that was formed post-election last November. If so, we will get another run at historically low rates before the final blow-off in Credit Markets sends Mortgage Interest rates up for good.

10 Year U.S. Treasury Note Yield Longer-term View back at 50-Day MA at 2.26%

(Chart courtesy of Zerohedge.com).

The above Chart does suggest that a constructive set-up is forming in the 10 Year Treasury Note with the potential to push the yield to around 2.00% over the next month. It is crucial that Mortgage Rates stay at or below 4.00% or demand for mortgage loans will dry up. The window of opportunity for borrowers seeking mortgage refinancing & home purchases is still open for now.

Weekly Mortgage Rates Analysis

As can be seen from Freddie Mac’s Mortgage Market Survey, last week, 30 Yr. Fixed Mortgage rates for conforming loans hit 3.93% with the rate rising 0.01% basis points from the previous week.

Treasury Prices Fall and Yields Rise for U.S. 10 Yr. and 30 Yr. Treasuries.

At the Chicago Board of Trade (CBOT): the US 10 Year Treasury Note futures Contract for September settlement closed at a price of 126’00.5 / 32nds; the 10 Year Note was down 5 basis points (bps) on the day, yielding 2.2619%. The US 30 Year Treasury Bond futures Contract for Sept. settlement closed at a price of 153’23 / 32nds; the 30 Year Bond was down 19 basis points (bps) on the day, yielding 2.8428%. Mortgage Rates have come off their 2017 lows and are up 0.01% bps from the previous Freddie Mac Survey last week.

Thanks to ZeroHedge.com, Bureau of Labor Statistics, Bloomberg.com, and FreddieMac.com for Charts and Graphics.

ERATE's Daily Rate Summary

August 8, 2017

Mortgage Rates and Treasury Yields Fall.

On Monday, Treasury bond yields and Mortgage interest rates fell as Credit Market participants bet on volatility and interest rate moderation in ‘quiet’ period in August. The September 10 Yr. U.S. Treasury Note stood at a yield of 2.2530% and the 30 Yr. U.S. Treasury Bond is yielding 2.8336%. 30 Year Mortgages according to Freddie Mac were around 3.93% for conforming and 4.09% for Jumbo products.

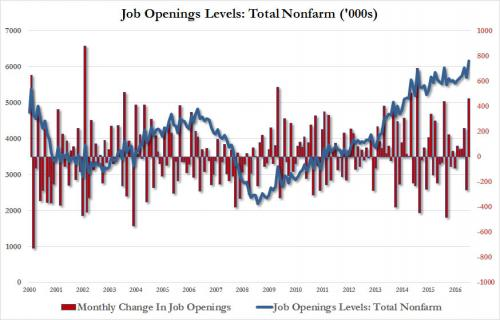

We have been talking about jobs & employment a lot lately and why this recovery seems a bit different…The JOLTS report was just released by the Bureau of Labor Statistics (BLS) for June. “After nearly two years of being rangebound, between 5.5 and 6 million, the BLS's JOLTS report - Janet Yellen's favorite labor market indicator- showed that in June, the number of job openings soared by 461,000 from 5.7 million to a new all-time high of 6.163 million, smashing expectations of a far more subdued print of 5.75K, and resulting in a job openings rate of 4.0%, also tied for record high”, as articulated by Zerohedge.com in analyzing BLS report.

Total Nonfarm Job Openings Hits All-Time High of 6,136,000 in June

(Chart courtesy of Zerohedge.com).

The biggest increase in job openings was in the Professional and Business Services category, which rose by 179K, Education and Health services which rose by 123K, Construction up by 62K, and Trade transportation up by 41K. Curiously, even manufacturing job openings increased by 38K in June, while Other Services and Retail job openings both declined, by 62K and 42K, respectively. The number of job openings increased in the Midwest and West regions.

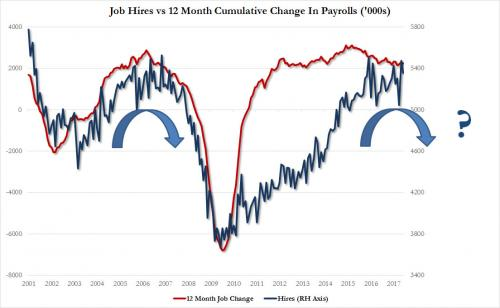

Job Hires vs Change in Payrolls (‘000s) in June

(Chart courtesy of Zerohedge.com).

The data is extended and can be seen to flatten suggesting maturity and eventual decline. Aside from the unexpected surge in job openings, the rest of the report was more subdued, with the pace of hiring actually declining from 5.459MM to 5.356MM... With wage gains having yet to materialize.

30 Year U.S. Treasury Bond Yield fall to 2.7972% then steadies at 2.8336%

(Chart courtesy of Zerohedge.com).

The 30 Year U.S. Treasury Bond is now expanded its trading range between 2.80% and 2.94%; as market participants try to guess whether we get a manufacturing recovery this summer or we dip back into recession in the real-goods producing sector of the economy.

30 Year U.S. Treasury Bond Yield Rangebound between 2.80% and 2.94%.

(Chart courtesy of Zerohedge.com).

At the extremes of this range buyers of long bonds can be counted on to appears in force when the 30 Year U.S. Treasury Yield moves to the top of this range around 2.94%; conversely, sellers come out when the yield falls to 2.80%.

10 Year U.S. Treasury Note Yield Falls to 2.2212% then steadies at 2.2530%

(Chart courtesy of Zerohedge.com).

This gyration in bond yields looks like it wants to resolve itself by moving much lower into the gap that was formed post-election last November. If so, we will get another run at historically low rates before the final blow-off in Credit Markets sends Mortgage Interest rates up for good.

10 Year U.S. Treasury Note Yield Longer-term View back below 50-Day MA at 2.26%

(Chart courtesy of Zerohedge.com).

The above Chart does suggest that a constructive set-up is forming in the 10 Year Treasury Note with the potential to push the yield to around 2.00% over the next month. It is crucial that Mortgage Rates stay at or below 4.00% or demand for mortgage loans will dry up. The window of opportunity for borrowers seeking mortgage refinancing & home purchases is still open for now.

Weekly Mortgage Rates Analysis

As can be seen from Freddie Mac’s Mortgage Market Survey, last week, 30 Yr. Fixed Mortgage rates for conforming loans hit 3.93% with the rate rising 0.01% basis points from the previous week.

Treasury Prices Rise and Yields Fall for U.S. 10 Yr. and 30 Yr. Treasuries.

At the Chicago Board of Trade (CBOT): the US 10 Year Treasury Note futures Contract for September settlement closed at a price of 126’05.5 / 32nds; the 10 Year Note was up 3 basis points (bps) on the day, yielding 2.2530%. The US 30 Year Treasury Bond futures Contract for Sept. settlement closed at a price of 154’10 / 32nds; the 30 Year Bond was up 7 basis points (bps) on the day, yielding 2.8336%. Mortgage Rates have come off their 2017 lows and are up 0.01% bps from the previous Freddie Mac Survey last week.

Thanks to ZeroHedge.com, Bureau of Labor Statistics, Bloomberg.com, and FreddieMac.com for Charts and Graphics.

ERATE's Daily Rate Summary

August 7, 2017

Mortgage Rates and Treasury Yields Rose.

On Friday, Treasury bond yields and Mortgage interest rates rose as Credit Market participants bet on volatility and interest rate moderation in ‘quiet’ period in August. The September 10 Yr. U.S. Treasury Note stood at a yield of 2.2620% and the 30 Yr. U.S. Treasury Bond is yielding 2.8420%. 30 Year Mortgages according to Freddie Mac were around 3.93% for conforming and 4.10% for Jumbo products.

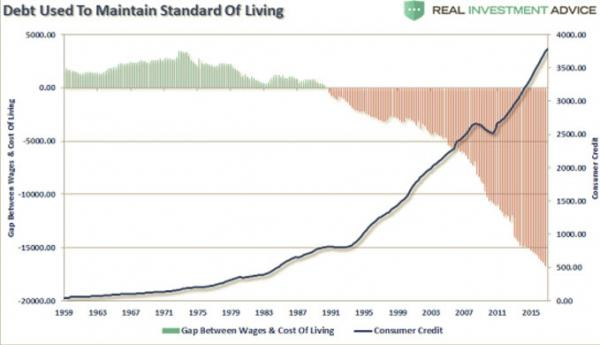

The Gap between Wages paid & Cost of Living has never been higher. The Chart below courtesy of Real Investment Advice show a very long historical view of this dynamic shortfall between Wages and the Cost of Living which has been mitigated over the years by reliance on Consumer Credit to fill the gap; which after a small jog in 2008-2009 is once again at record highs.

Debt Used To Maintain Standard of Living

(Chart courtesy of REAL Investment Advice).

It is widely known that both Thorstein Veblen and James Duesenberry recognized the significance of social influences on consumption patterns...

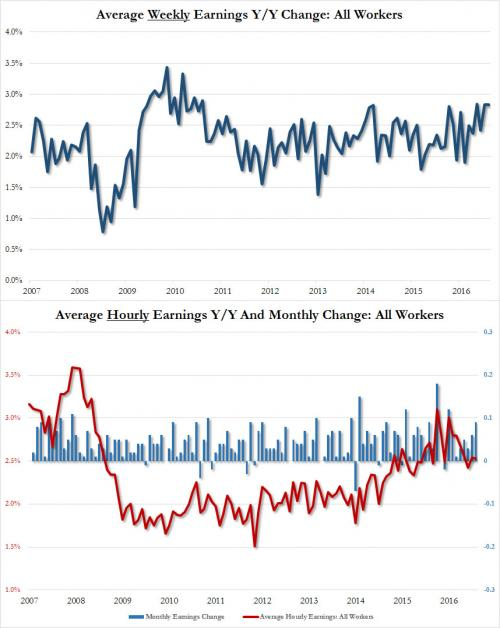

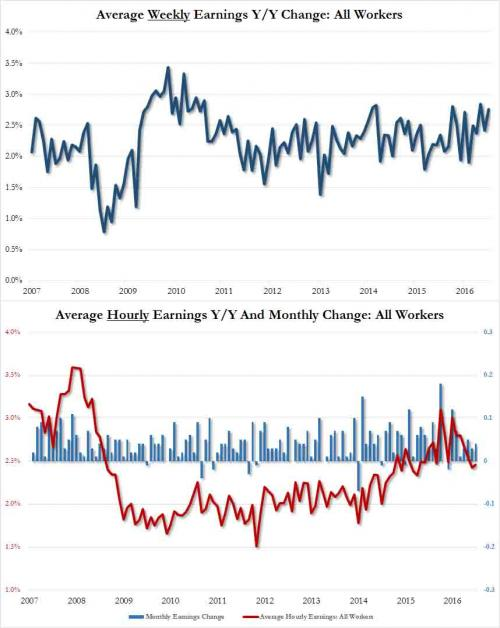

Average Weekly Earnings Rose 2.8% & Hourly Earnings Rose 2.5% in July

(Chart courtesy of Zerohedge.com).

As can be seen by Monthly & Hourly Average Earning Charts consumer income growth from wages has been flat or in slow growth mode for the whole of this recovery. This creates what financial economists call the “Dusenberry Effect” which (as Zerohedge.com) basically states that consumers do not give up their consumption patterns very easy even if their incomes decline.

They, in effect, “ratchet” down their living standard very slowly by first having a second wage earner enter the workforce as we saw in the 1970’s when women began to enter the workforce en masse and then by taking on debt to finance their previous standard of living.

According to Zerohedge.com, “…[a] significant part of Duesenberry’s relative income hypothesis is that it suggests that when income of individuals or households falls, their consumption expenditure does not fall much. This is often called a ratchet effect. This is because, according to Duesenberry, the people try to maintain their consumption at the highest level attained earlier. This is partly due to the demonstration effect explained above. People do not want to show to their neighbors that they no longer afford to maintain their high standard of living.”

Further, this is also partly due to the fact that they become accustomed to their previous higher level of consumption and it is quite hard and difficult to reduce their consumption expenditure when their income has fallen. They maintain their earlier consumption level by reducing their savings. Therefore, the fall in their income, as during the period of recession or depression, does not result in decrease in consumption expenditure very much as one would conclude from family budget studies.

As Real Investment Advice opines, “We suspect the cumulative policy decisions of bailing out debt holders and punishing savers over the past 30 years has changed attitudes on debt accumulation.

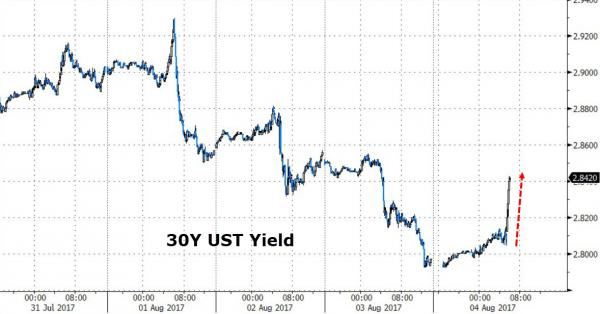

30 Year U.S. Treasury Bond Yield fall to 2.7972% then rebounds to 2.8420% after NFP.

(Chart courtesy of Zerohedge.com).

The 30 Year U.S. Treasury Bond is now expanded its trading range between 2.80% and 2.94%; as market participants try to guess whether we get a manufacturing recovery this summer or we dip back into recession in the real-goods producing sector of the economy.

30 Year U.S. Treasury Bond Yield Rangebound between 2.80% and 2.94%.

(Chart courtesy of Zerohedge.com).

At the extremes of this range buyers of long bonds can be counted on to appears in force when the 30 Year U.S. Treasury Yield moves to the top of this range around 2.94%; conversely, sellers come out when the yield falls to 2.80%.

10 Year U.S. Treasury Note Yield Falls to 2.2212% then pops to 2.2620% on NFP

(Chart courtesy of Zerohedge.com).

This gyration in bond yields looks like it wants to resolve itself by moving much lower into the gap that was formed post-election last November. If so, we will get another run at historically low rates before the final blow-off in Credit Markets sends Mortgage Interest rates up for good.

10 Year U.S. Treasury Note Yield Longer-term View back above 50-Day MA at 2.26%

(Chart courtesy of Zerohedge.com).

The above Chart does suggest that a constructive set-up is forming in the 10 Year Treasury Note with the potential to push the yield to around 2.00% over the next month. It is crucial that Mortgage Rates stay at or below 4.00% or demand for mortgage loans will dry up. The window of opportunity for borrowers seeking mortgage refinancing & home purchases is still open for now.

Weekly Mortgage Rates Analysis

As can be seen from Freddie Mac’s Mortgage Market Survey, last week, 30 Yr. Fixed Mortgage rates for conforming loans hit 3.93% with the rate rising 0.01% basis points from the previous week.

Treasury Prices Fall and Yields Rise for U.S. 10 Yr. and 30 Yr. Treasuries.

At the Chicago Board of Trade (CBOT): the US 10 Year Treasury Note futures Contract for September settlement closed at a price of 126’02.5 / 32nds; the 10 Year Note was down 9 basis points (bps) on the day, yielding 2.2620%. The US 30 Year Treasury Bond futures Contract for Sept. settlement closed at a price of 154’03 / 32nds; the 30 Year Bond was down 29 basis points (bps) on the day, yielding 2.8420%. Mortgage Rates have come off their 2017 lows and are up 0.01% bps from the previous Freddie Mac Survey last week.

Thanks to ZeroHedge.com, Bloomberg.com, Real Investment Advice, and FreddieMac.com for Charts and Graphics.

ERATE's Daily Rate Summary

August 4, 2017

Mortgage Rates and Treasury Yields Fall.

On Thursday, Treasury bond yields and Mortgage interest rates fell sharply as Credit Market participants bet on volatility and interest rate moderation in 'quiet' period in August. The September 10 Yr. U.S. Treasury Note stood at a yield of 2.2212% and the 30 Yr. U.S. Treasury Bond is yielding 2.7972%. 30 Year Mortgages according to Freddie Mac were around 3.93% for conforming and 4.10% for Jumbo products.

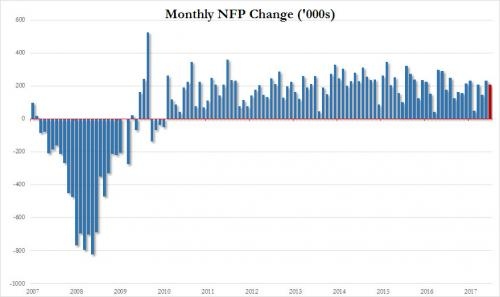

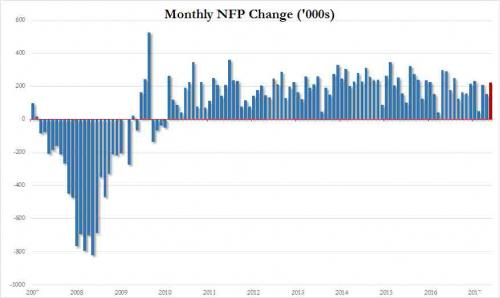

The Bureau of Labor Statistics (BLS) reports that in July the US added 209K jobs, beating consensus expectations of a 180K print, while June was revised higher to 231K from 222K, even as May was revised modestly lower from 152K to 145K, for a net gain of +2,000 in the prior two months.

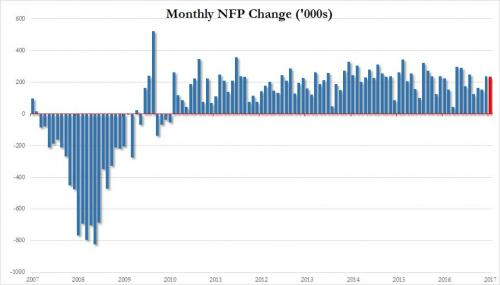

BLS Non-Farm Payroll increased +209,000 in July

(Chart courtesy of Zerohedge.com).

Nonfarm private payrolls rose 205k vs last month's 194k, and above the estimate of 180k, as the drop from durable manufacturing failed to materialize. In a familiar refrain, bars and restaurants hired the most workers of any sector in July.

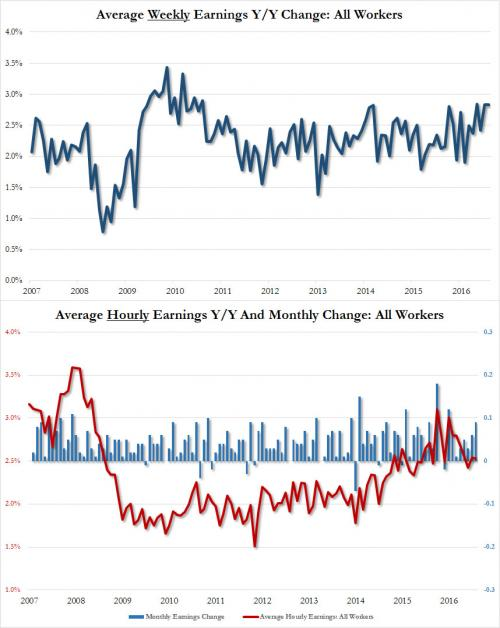

Average Weekly Earnings Rose 2.8% & Hourly Earnings Rose 2.5% in July

(Chart courtesy of Zerohedge.com).

The BLS reported that Average Weekly & Hourly earnings both rose in July, which is consistent with the current narrative that Labor conditions are tightening and wages are finally beginning to see some inflationary pressure coming from the Labor Markets which we would expect from an economy which should now be in a strong recovery after 9 years.

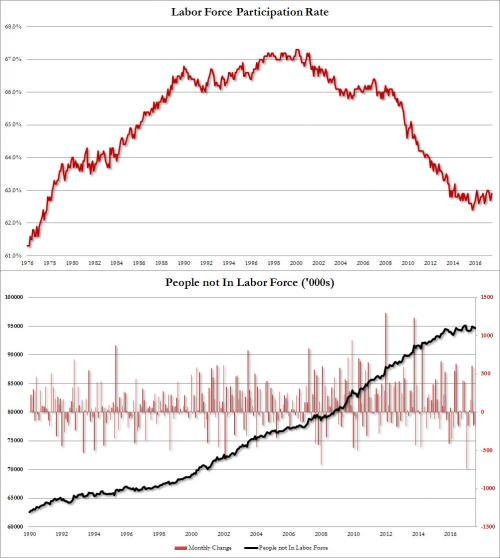

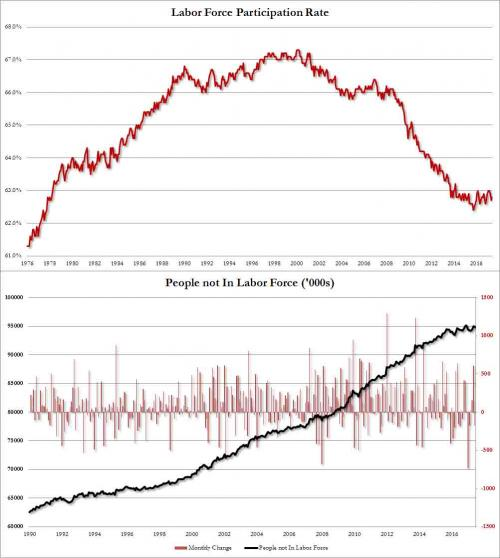

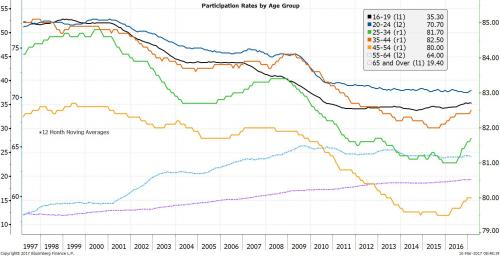

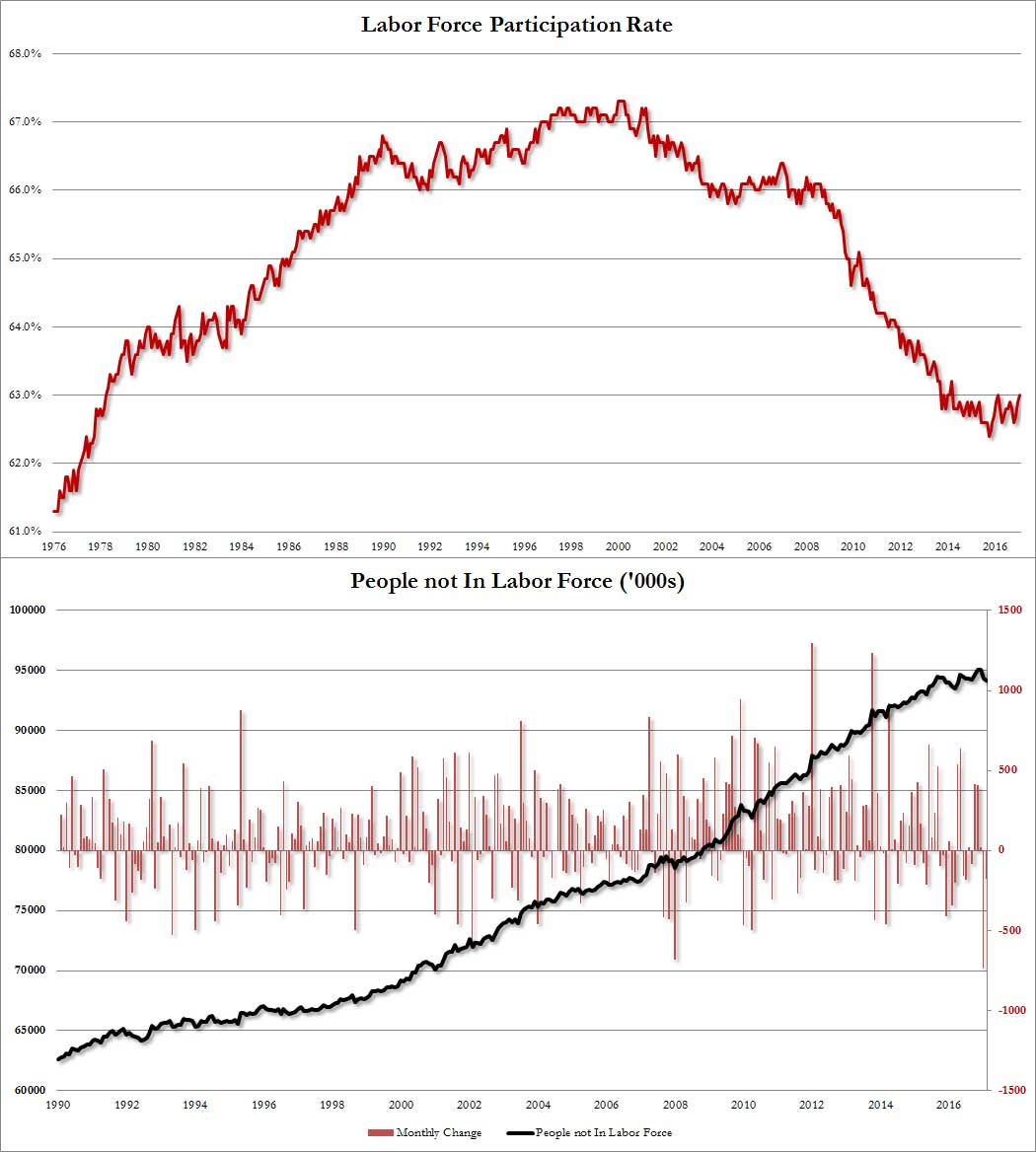

Labor Force Participation Rate Rises to 62.9% Vs. People not In Labor Force totals 94 Million

(Chart courtesy of Zerohedge.com).

The unemployment rate dropped from 4.4% to 4.3% as expected, while the participation rate rose from 62.8% to 62.9%, as the number of workers out of the labor force declined by 156K to 94.657 million.

Total nonfarm payroll employment increased by 209,000 in July. Job gains occurred in food services and drinking places, professional and business services, and health care. Employment growth has averaged 184,000 per month thus far this year, in line with the average monthly gain in 2016 of (+187,000) jobs per month.

30 Year U.S. Treasury Bond Yield Falls to 2.7972% then rebounds to 2.8420% after NFP.

(Chart courtesy of Zerohedge.com).

The 30 Year U.S. Treasury Bond is now expanded its trading range between 2.80% and 2.94%; as market participants try to guess whether we get a manufacturing recovery this summer or we dip back into recession in the real-goods producing sector of the economy.

At the extremes of this range buyers of long bonds can be counted on to appears in force when the 30 Year U.S. Treasury Yield moves to the top of this range around 2.94%; conversely, sellers come out when the yield falls to 2.80%.

10 Year U.S. Treasury Note Yield Falls to 2.2212% then pops to 2.2869% on NFP

(Chart courtesy of Zerohedge.com).

This gyration in bond yields looks like it wants to resolve itself by moving much lower into the gap that was formed post-election last November. If so, we will get another run at historically low rates before the final blow-off in Credit Markets sends Mortgage Interest rates up for good.

10 Year U.S. Treasury Note Yield Longer-term View back above 50-Day MA at 2.26%

(Chart courtesy of Zerohedge.com).

The above Chart does suggest that a constructive set-up is forming in the 10 Year Treasury Note with the potential to push the yield to around 2.00% over the next month. It is crucial that Mortgage Rates stay at or below 4.00% or demand for mortgage loans will dry up. The window of opportunity for borrowers seeking mortgage refinancing & home purchases is still open for now.

Weekly Mortgage Rates Analysis

As can be seen from Freddie Mac's Mortgage Market Survey, last week, 30 Yr. Fixed Mortgage rates for conforming loans hit 3.93% with the rate rising 0.01% basis points from the previous week.

Treasury Prices Rise and Yields Fall for U.S. 10 Yr. and 30 Yr. Treasuries.

At the Chicago Board of Trade (CBOT): the US 10 Year Treasury Note futures Contract for September settlement closed at a price of 126'11.5 / 32nds; the 10 Year Note was up 8 basis points (bps) on the day, yielding 2.2212%. The US 30 Year Treasury Bond futures Contract for Sept. settlement closed at a price of 155'00 / 32nds; the 30 Year Bond was up 25 basis points (bps) on the day, yielding 2.7972%. Mortgage Rates have come off their 2017 lows and are up 0.01% bps from the previous Freddie Mac Survey last week.

Thanks to ZeroHedge.com, Bloomberg.com, Bureau of Labor Statistics, and FreddieMac.com for Charts and Graphics.

ERATE's Daily Rate Summary

August 3, 2017

Mortgage Rates and Treasury Yields Mixed.

On Wednesday, Treasury bond yields and Mortgage interest rates were mixed as Credit Market volatility increases and interest rates plumb lower reaches of the price range. The September 10 Yr. U.S. Treasury Note stood at a yield of 2.2710% and the 30 Yr. U.S. Treasury Bond is yielding 2.8559%. 30 Year Mortgages according to Freddie Mac were around 3.93% for conforming and 4.11% for Jumbo products.

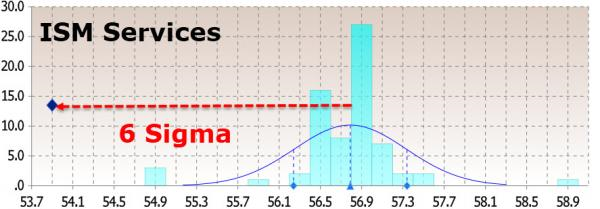

The ISM Services Index fell sharply to a reading of 53.9 while the Services PMI rose to 54.7 in July; according to the Institute for Supply Management (ISM). Expectations were for a reading of 54.6 in the Services Index and 56.9 for the Services PMI.

ISM Services Index Falls to 53.9 & Services PMI Rises to 54.7 in July

(Chart courtesy of Zerohedge.com).

US Services were even more mixed with PMI printing at 6-month highs (new business expanding at its fastest in two years), and ISM collapsing to 11-month lows. In the context of the continuing collapse in 'hard' economic data (against even weaker expectations), Zerohedge.com noted; "surveys of US Services employers by PMI are ebullient, but it seems the people that ISM are talking to are dysphoric....and the 53.9 print below the lowest economist estimate of 54.9...missing expectations by 6 standard deviations...".

ISM Services Expectations Miss was a 6 Sigma Event

(Chart courtesy of Zerohedge.com).

ISM Respondents do not seem to be as exuberant as PMI respondents.

"A typical and expected midsummer slowdown in hiring activity by employers is causing a normal slowdown in business for this time of year. We expect a sharp ramp-up of business activity over the next three months." (Management of Companies & Support Services)

"Business volume slowed some in June." (Health Care & Social Assistance)

"Business in third quarter is looking up, but it may be delayed from slower than expected second quarter. The next couple of months will determine the outcome." (Professional, Scientific & Technical Services)

There is one thing to pay attention to however: Input costs paid by service providers continued to rise in July, thereby extending the trend seen every month since data collection began in October 2009."

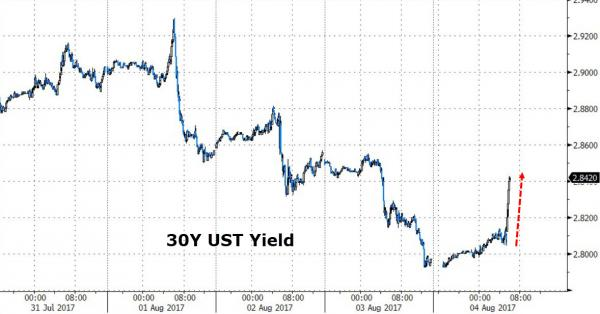

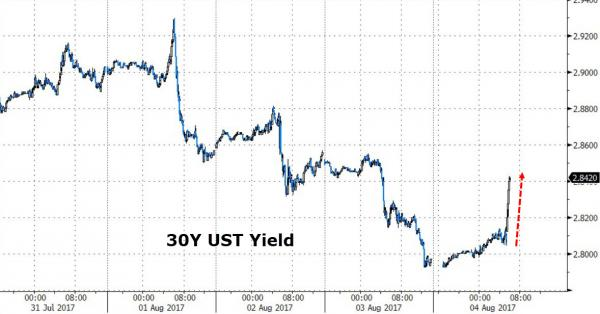

30 Year U.S. Treasury Bond Yield Falls to 2.8559%

(Chart courtesy of Zerohedge.com).

The 30 Year U.S. Treasury Bond is oscillating between 2.85% and 2.94%; as market participants try to guess whether we get a manufacturing recovery this summer or we dip back into recession in the real-goods producing sector of the economy.

A buyer for long bonds always appears in force when the 30 Year U.S. Treasury Yield inches back up around the top of this range. Watch for Bond price volatility to increase sharply over the next several weeks as a tug-of-war between "Hawks" and "Doves" emerge in the quiet period between now and Jackson Hole, Wyoming conference, and the next Central Bank meetings in September.

10 Year U.S. Treasury Note Yield Rises to 2.2710%

(Chart courtesy of Zerohedge.com).

This gyration in bond yields looks like it wants to resolve itself by moving much lower into the gap that was formed post-election last November. If so, we will get another run at historically low rates before the final blow-off in Credit Markets sends Mortgage Interest rates up for good.

10 Year U.S. Treasury Note Yield Longer-term View back above 50-Day MA at 2.26%

(Chart courtesy of Zerohedge.com).

The above Chart does suggest that a constructive set-up is forming in the 10 Year Treasury Note with the potential to push the yield to around 2.00% over the next month. It is crucial that Mortgage Rates stay at or below 4.00% or demand for mortgage loans will dry up. The window of opportunity for borrowers seeking mortgage refinancing & home purchases is still open for now.

Weekly Mortgage Rates Analysis

As can be seen from Freddie Mac's Mortgage Market Survey, last week, 30 Yr. Fixed Mortgage rates for conforming loans hit 3.93% with the rate rising 0.01% basis points from the previous week.

Treasury Prices Fall and Yields Rise Slightly for U.S. 10 Yr. and 30 Yr. Treasuries.

At the Chicago Board of Trade (CBOT): the US 10 Year Treasury Note futures Contract for September settlement closed at a price of 126'03.5 / 32nds; the 10 Year Note was down 4 basis points (bps) on the day, yielding 2.2710%. The US 30 Year Treasury Bond futures Contract for Sept. settlement closed at a price of 154'07 / 32nds; the 30 Year Bond was up 6 basis points (bps) on the day, yielding 2.8559%. Mortgage Rates have come off their 2017 lows and are down 0.04% bps from the previous Freddie Mac Survey last week.

Thanks to ZeroHedge.com, Bloomberg.com, Institute for Supply Management, and FreddieMac.com for Charts and Graphics.

ERATE's Daily Rate Summary

August 2, 2017

Mortgage Rates and Treasury Yields Fall.

On Tuesday, Treasury bond yields and Mortgage interest rates fell moderately as Credit Market volatility increases and interest rates plumb lower reaches of the price range. The September 10 Yr. U.S. Treasury Note stood at a yield of 2.2532% and the 30 Yr. U.S. Treasury Bond is yielding 2.8567%. 30 Year Mortgages according to Freddie Mac were around 3.92% for conforming and 4.10% for Jumbo products.

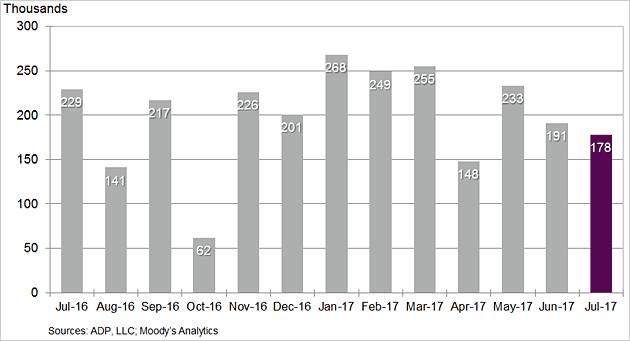

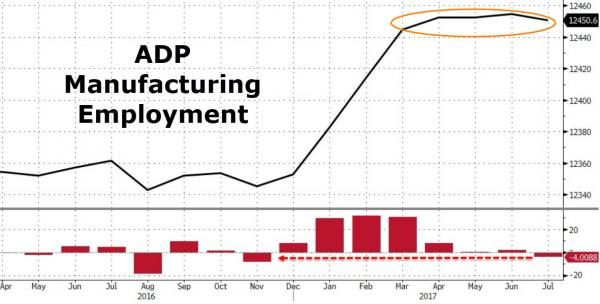

In July, the ADP Payrolls Employment Survey for July increased by 178,000 jobs. While the ADP Manufacturing Employment Index was flat losing -4,000 jobs. Service Jobs added the bulk of those gains in employment in July adding 174,000 while Goods Producing had a +4,000 gain in jobs. On a total employment change basis this was the second worst month since October:

ADP Payroll Employment Survey Gains +178,000 Jobs in July

(Sources: ADP, LLC; Moody's Analytics).

Two months in a row, ADP has weakened as ISM surveys suggested employment is rolling over. After April and June's disappointment, ADP reports the US economy added 178k jobs in July (less than the 190k expectation and below June's upwardly revised 191k). This is somewhat in line with the 180k expectation for NFP on Friday.

ADP Manufacturing Employment Flat

(Chart courtesy of Zerohedge.com).

From a longer-term perspective, after 3 months of adding manufacturing jobs the economy has taken a breather in Manufacturing Employment since March according to ADP Survey. "Job gains continued to be strong in the month of July," said Ahu Yildirmaz, vice president and co-head of the ADP Research Institute. "However, as the labor market tightens employers may find it more difficult to recruit qualified workers."

Mark Zandi, chief economist of Moody's Analytics, said, "The American job machine continues to operate in high gear. Job gains are broad-based across industries and company sizes, with only manufacturers reducing their payrolls. At this pace of job growth, unemployment will continue to quickly decline."

30 Year U.S. Treasury Bond Yield Falls to 2.8559%

(Chart courtesy of Zerohedge.com).

The 30 Year U.S. Treasury Bond is oscillating between 2.85% and 2.94%; as market participants try to guess whether we get a manufacturing recovery this summer or we dip back into recession in the real-goods producing sector of the economy.

A buyer for long bonds always appears in force when the 30 Year U.S. Treasury Yield inches back up around the top of this range. Watch for Bond price volatility to increase sharply over the next several weeks as a tug-of-war between "Hawks" and "Doves" emerge in the quiet period between now and Jackson Hole, Wyoming conference, and the next Central Bank meetings in September.

10 Year U.S. Treasury Note Yield Falls to 2.2532%

(Chart courtesy of Zerohedge.com).

This gyration in bond yields looks like it wants to resolve itself by moving much lower into the gap that was formed post-election last November. If so, we will get another run at historically low rates before the final blow-off in Credit Markets sends Mortgage Interest rates up for good.

10 Year U.S. Treasury Note Yield Longer-term View back below 50-Day MA at 2.26%

(Chart courtesy of Zerohedge.com).

The above Chart does suggest that a constructive set-up is forming in the 10 Year Treasury Note with the potential to push the yield to around 2.00% over the next month. It is crucial that Mortgage Rates stay at or below 4.00% or demand for mortgage loans will dry up. The window of opportunity for borrowers seeking mortgage refinancing & home purchases is still open for now.

Weekly Mortgage Rates Analysis

As can be seen from Freddie Mac's Mortgage Market Survey, last week, 30 Yr. Fixed Mortgage rates for conforming loans hit 3.92% with the rate falling 0.04% basis points from the previous week.

Treasury Prices Rise and Yields Fall Moderately for U.S. 10 Yr. and 30 Yr. Treasuries.

At the Chicago Board of Trade (CBOT): the US 10 Year Treasury Note futures Contract for September settlement closed at a price of 126'07.5 / 32nds; the 10 Year Note was up 11 basis points (bps) on the day, yielding 2.2532%. The US 30 Year Treasury Bond futures Contract for Sept. settlement closed at a price of 154'02 / 32nds; the 30 Year Bond was up 34 basis points (bps) on the day, yielding 2.8567%. Mortgage Rates have come off their 2017 lows and are down 0.04% bps from the previous Freddie Mac Survey last week.

Thanks to ZeroHedge.com, ADP, LLC; Moody's Analytics, and FreddieMac.com for Charts and Graphics.

ERATE's Daily Rate Summary

August 1, 2017

Mortgage Rates and Treasury Yields Rose Slightly.

On Monday, Treasury bond yields and Mortgage interest rates rose slightly as Credit Markets volatility increase and interest rates search around seeking direction. The September 10 Yr. U.S. Treasury Note stood at a yield of 2.2942% and the 30 Yr. U.S. Treasury Bond is yielding 2.8999%. 30 Year Mortgages according to Freddie Mac were around 3.92% for conforming and 4.10% for Jumbo products.

In July, ISM Manufacturing Index fell to 56.3, while the Manufacturing PMI rose to 53.3 in a mixed bag of reports about the U.S. Manufacturing economy. The U.S. Macro 'Hard' Data picture remains where it has been all spring in the dumps with depressed overall conditions.

ISM Manufacturing, PMI Index, Vs. U.S. Macro 'Hard' Data

(Chart courtesy of Zerohedge.com).

From a longer-term perspective, economic conditions based on 'Hard' Data and not 'Soft' data surveys asking about buoyant outlook & perspectives as Stocks continue to hit all-time highs; has led to a dichotomy of historic proportions regarding future expectations. After hitting a 9-month low in June, Markit's US Manufacturing PMI bounced to 53.3 in July with new orders, output, and employment rebounding. In a China-like moment, ISM disappointed, modestly dropping to 56.3 with prices paid surging and new orders tumbling. All of this uncertainty is happening as 'hard' data in the American economy is collapsing. After six straight months lower, PMI bounced in July (very slightly beating the 53.2 expectation) but ISM dipped and missed expectations.

U.S. Treasury Bond Yield Rises to 2.8999%

(Chart courtesy of Zerohedge.com).

The 30 Year U.S. Treasury Bond is oscillating between 2.88% and 2.94%; as market participants try to guess whether we get a manufacturing recovery this summer or we dip back into recession in the real-goods producing sector of the economy. A buyer for long bonds always appears in force when the 30 Year U.S. Treasury Yield inches back up around the top of this range. Watch for Bond price volatility to increase sharply over the next several weeks as a tug-of-war between "Hawks" and "Doves" emerge in the quiet period between now the next Central Bank meetings in September.

10 Year U.S. Treasury Note Yield Falls to 2.2942%

(Chart courtesy of Zerohedge.com).

This gyration in bond yields looks like it wants to resolve itself by moving much lower into the gap that was formed post-election last November. If so, we will get another run at historically low rates before the final blow-off in Credit Markets sends Mortgage Interest rates up for good.

10 Year U.S. Treasury Note Yield Longer-term View back above 50-Day MA at 2.26%

(Chart courtesy of Zerohedge.com).

The above Chart does suggest that a constructive set-up is forming in the 10 Year Treasury Note with the potential to push the yield to around 2.00% over the next month. As Congress turns its attention to negotiations regarding the raising of the Debt-Ceiling and U.S. Government finances once again. It is crucial that Mortgage Rates stay at or below 4.00% or demand for mortgage loans will dry up. The window of opportunity for borrowers seeking mortgage refinancing & home purchases is still open for now, but for how long?

Weekly Mortgage Rates Analysis

As can be seen from Freddie Mac's Mortgage Market Survey, last week, 30 Yr. Fixed Mortgage rates for conforming loans hit 3.92% with the rate falling 0.04% basis points from the previous week.

Treasury Prices Rise and Yields Rise Slightly for U.S. 10 Yr. and 30 Yr. Treasuries.

At the Chicago Board of Trade (CBOT): the US 10 Year Treasury Note futures Contract for September settlement closed at a price of 125'28.5 / 32nds; the 10 Year Note was down 2 basis points (bps) on the day, yielding 2.2942%. The US 30 Year Treasury Bond futures Contract for Sept. settlement closed at a price of 152'31 / 32nds; the 30 Year Bond was down 7 basis points (bps) on the day, yielding 2.8999%. Mortgage Rates have come off their 2017 lows and are down 0.04% bps from the previous Freddie Mac Survey last week.

Thanks to ZeroHedge.com, Markit.com, and FreddieMac.com for Charts and Graphics.

ERATE's Daily Rate Summary

July 31, 2017

Mortgage Rates and Treasury Yields Fell Slightly.

On Friday, Treasury bond yields and Mortgage interest rates fell slightly as Credit Markets volatility increase and interest rates search around seeking direction. The September 10 Yr. U.S. Treasury Note stood at a yield of 2.2889% and the 30 Yr. U.S. Treasury Bond is yielding 2.8953%. 30 Year Mortgages according to Freddie Mac were around 3.92% for conforming and 4.10% for Jumbo products.

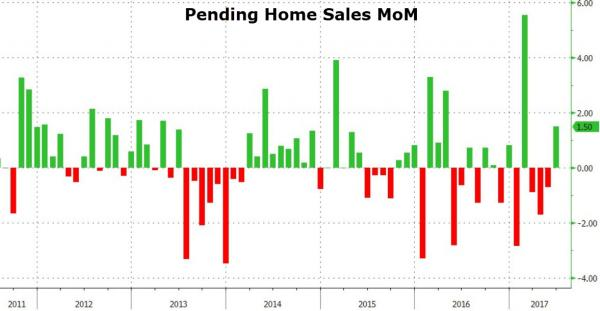

In June, Pending Home Sales Rose 1.5% (MoM) from the previous month.

Pending Home Sales MoM Rise 1.5%

(Chart courtesy of Zerohedge.com).

From a longer-term perspective, Pending Home Sales have increased just 0.7% year-over-year and the index is up to 110.2 in the past six years.

Market conditions in many areas continue to be fast paced, with few properties to choose from, which is forcing buyers to act almost immediately on an available home that fits their criteria," Lawrence Yun, NAR's chief economist, said in a statement.

"Low supply is an ongoing issue holding back activity. Housing inventory declined last month and is a staggering 7.1 percent lower than a year ago."

Two things do stand out though: 13 percent of sales went to investors, smallest share this year; and All-cash transactions accounted for 18 percent of signings, the smallest share since June 2009.

Pending Home Sales Historical View (2011 to Present) +10.2%

(Chart courtesy of Zerohedge.com).

30 Year U.S. Treasury Bond Yield Falls to 2.8953%

(Chart courtesy of Zerohedge.com).

The 30 Year U.S. Treasury Bond is being whipsawed back-and-forth as successive Central Bank speakers take turns sounding-off on the near-term course of interest rate policy. Watch for Bond price volatility to increase sharply over the next several weeks as a tug-of-war between "Hawks" and "Doves" emerge in the quiet period between now the next Central Bank meetings in September.

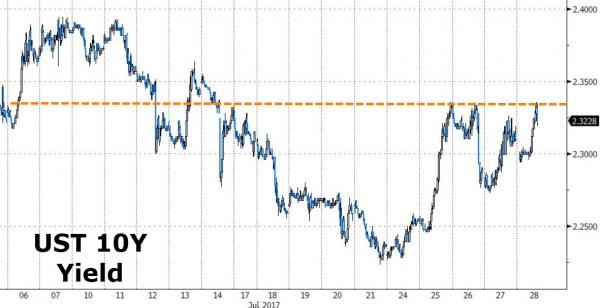

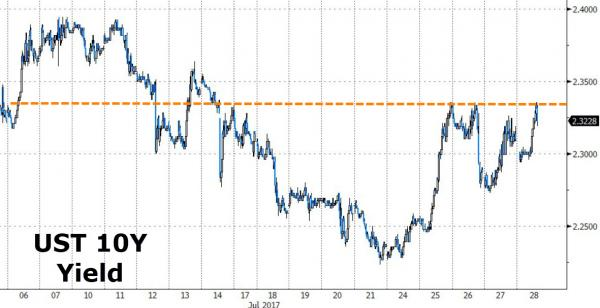

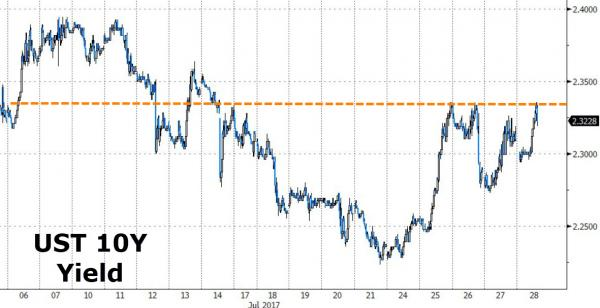

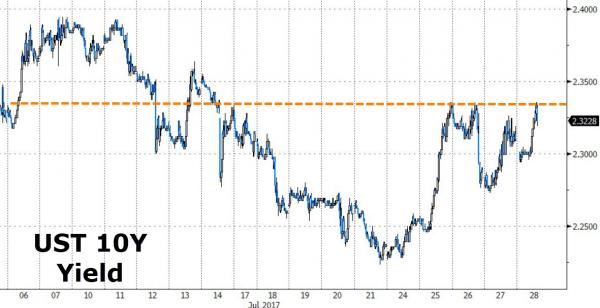

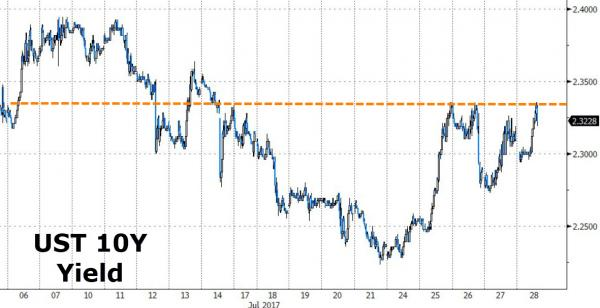

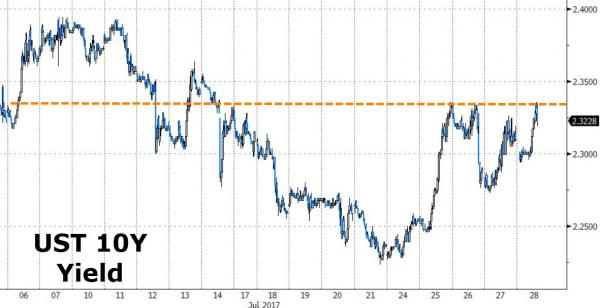

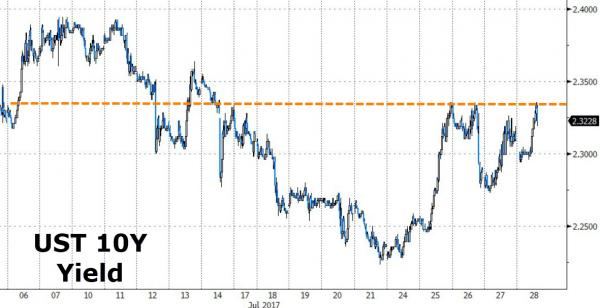

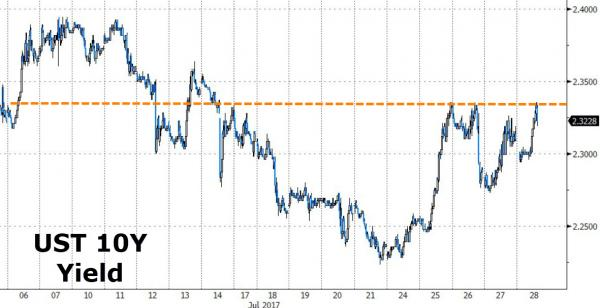

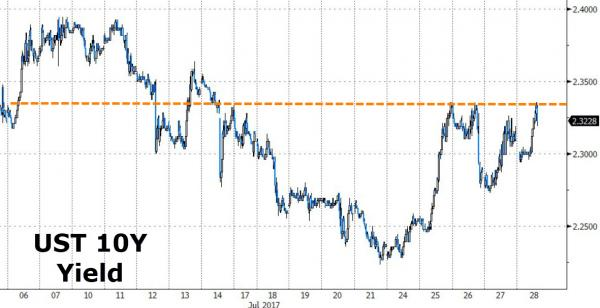

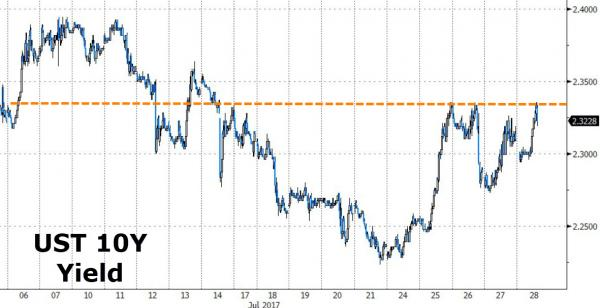

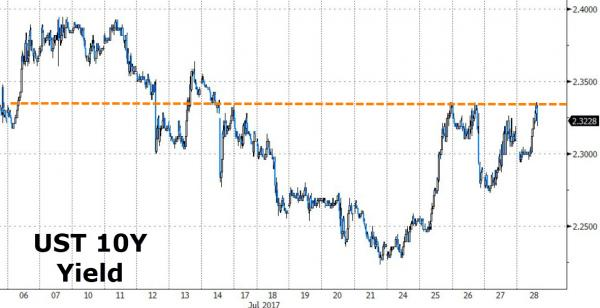

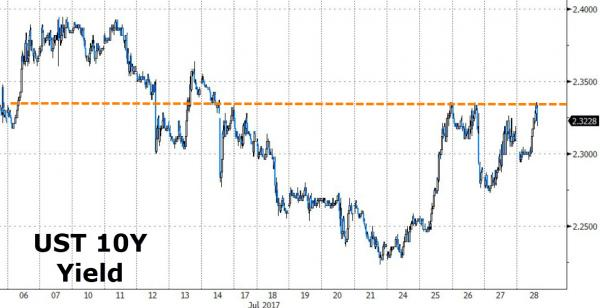

10 Year U.S. Treasury Note Yield Rises to 2.3228%

(Chart courtesy of Zerohedge.com).

This gyration in yields is most unwelcome and will put a damper on the summer homebuying season which was already one of the weakest in recent years due to lack of supply & affordability according to Larry Yun chief economist at the National Association of Realtors (NAR).

10 Year U.S. Treasury Note Yield Longer-term View back above 50-Day MA at 2.26%

(Chart courtesy of Zerohedge.com).

The above Chart does suggest that a constructive set-up is forming in the 10 Year Treasury Note with the potential to push the yield to around 2.00% over the next month. As Congress turns its attention to negotiations regarding the raising of the Debt-Ceiling and U.S. Government finances once again. It is crucial that Mortgage Rates stay at or below 4.00% or demand for mortgage loans will dry up. The window of opportunity for borrowers seeking mortgage refinancing & home purchases is still open for now, but for how long?

Weekly Mortgage Rates Analysis

As can be seen from Freddie Mac's Mortgage Market Survey, last week, 30 Yr. Fixed Mortgage rates for conforming loans hit 3.92% with the rate falling 0.04% basis points from the previous week.

Treasury Prices Rise and Yields Fall Slightly for U.S. 10 Yr. and 30 Yr. Treasuries.

At the Chicago Board of Trade (CBOT): the US 10 Year Treasury Note futures Contract for September settlement closed at a price of 125'30.5 / 32nds; the 10 Year Note was up 4 basis points (bps) on the day, yielding 2.2889%. The US 30 Year Treasury Bond futures Contract for Sept. settlement closed at a price of 153'06 / 32nds; the 30 Year Bond was up 19 basis points (bps) on the day, yielding 2.8953%. Mortgage Rates have come off their 2017 lows and are down 0.04% bps from the previous Freddie Mac Survey last week.

Thanks to ZeroHedge.com and FreddieMac.com for Charts and Graphics.

ERATE's Daily Rate Summary

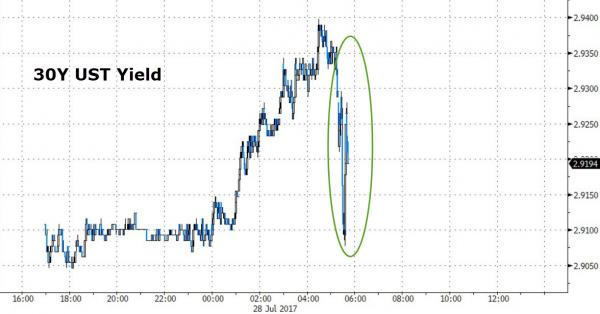

July 28, 2017

Mortgage Rates and Treasury Yields Rose Slightly.

On Thursday, Treasury bond yields and Mortgage interest rates rose slightly as Credit Markets volatility increase and interest rates bounce around seeking direction. The September 10 Yr. U.S. Treasury Note stood at a yield of 2.3103% and the 30 Yr. U.S. Treasury Bond is yielding 2.9194%. 30 Year Mortgages according to Freddie Mac were around 3.92% for conforming and 4.10% for Jumbo products.

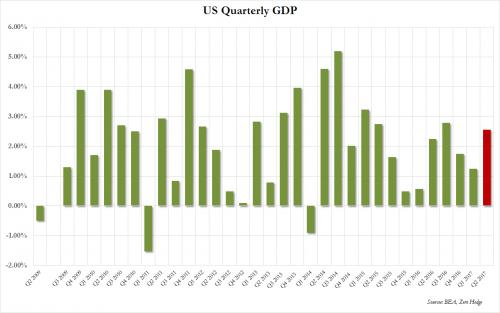

Real gross domestic product increased at an annual rate of 2.6 percent in the second quarter of 2017 (see Chart below), according to the "advance" estimate released by the Bureau of Economic Analysis (BEA). In the first quarter, real GDP increased 1.2 percent (revised downward from 1.4%).

The increase in real GDP in the second quarter reflected positive contributions from personal consumption expenditures (PCE), nonresidential fixed investment, exports, and federal government spending that were partly offset by negative contributions from private residential fixed investment, private inventory investment, and state and local government spending.

U.S. Quarterly GDP for Q2 is pegged at 2.6%

(Chart courtesy of Zerohedge.com).

In the latest disappointment for the Federal Reserve about the economy, not only did Q2 GDP miss consensus expectations of 2.7%, but Q1 GDP of 1.4% was also revised slightly lower, to 1.2%. While the Fed's favorite inflationary metric, core Personal Consumption Expenditures (PCE), tumbled Qtr.-over- Qtr. from a downward revised 1.8% in Q1 to just 0.9% in Q2, but remained a positive contributor in the report (just barely). PCE represents about of 70% of the economy.

30 Year U.S. Treasury Bond Yield Rises to 2.9194%

(Chart courtesy of Zerohedge.com).

The 30 Year U.S. Treasury Bond is being whipsawed back-and-forth as successive Central Bank speakers take turns sounding-off on the near-term course of interest rate policy. Watch for Bond price volatility to increase sharply over the next several weeks as a tug-of-war between "Hawks" and "Doves" emerge in the quiet period between now the next Central Bank meetings in September.

10 Year U.S. Treasury Note Yield Rises to 2.3228%

(Chart courtesy of Zerohedge.com).

This gyration in yields is most unwelcome and will put a damper on the summer homebuying season which was already one of the weakest in recent years due to lack of supply & affordability according to Larry Yun chief economist at the National Association of Realtors (NAR).

10 Year U.S. Treasury Note Yield Longer-term View back above 50-Day MA at 2.26%

(Chart courtesy of Zerohedge.com).

The above Chart does suggest that a constructive set-up is forming in the 10 Year Treasury Note with the potential to push the yield to around 2.00% over the next month. As Congress turns its attention to negotiations regarding the raising of the Debt-Ceiling and U.S. Government finances once again. It is crucial that Mortgage Rates stay at or below 4.00% or demand for mortgage loans will dry up. The window of opportunity for borrowers seeking mortgage refinancing & home purchases is still open for now, but for how long?

Weekly Mortgage Rates Analysis

As can be seen from Freddie Mac's Mortgage Market Survey, last week, 30 Yr. Fixed Mortgage rates for conforming loans hit 3.92% with the rate falling 0.04% basis points from the previous week.

Treasury Prices Fall and Yields Rise Slightly for U.S. 10 Yr. and 30 Yr. Treasuries.

At the Chicago Board of Trade (CBOT): the US 10 Year Treasury Note futures Contract for September settlement closed at a price of 125'26.5 / 32nds; the 10 Year Note was down 6 basis points (bps) on the day, yielding 2.3103%. The US 30 Year Treasury Bond futures Contract for Sept. settlement closed at a price of 152'19 / 32nds; the 30 Year Bond was down 18 basis points (bps) on the day, yielding 2.9194%. Mortgage Rates have come off their 2017 lows and are down 0.04% bps from the previous Freddie Mac Survey last week.

Thanks to ZeroHedge.com and FreddieMac.com for Charts and Graphics.

ERATE's Daily Rate Summary

July 27, 2017

Mortgage Rates and Treasury Yields Fall Slightly.

On Wednesday, Treasury bond yields and Mortgage interest rates fell slightly as Credit Markets digest FOMC Statement for changes in interest rate policy & intentions. The September 10 Yr. U.S. Treasury Note stood at a yield of 2.2872% and the 30 Yr. U.S. Treasury Bond is yielding 2.8914%. 30 Year Mortgages according to Freddie Mac were around 3.92% for conforming and 4.10% for Jumbo products.

Wednesday's release of the July FOMC Statement, cast doubt on the Fed's determination with its stated program of continued rate hikes & balance sheet normalization. With ECB president Mario Drahi's hawkish comments, and Janet Yellen's dovish statement last week, 30 Year Treasury Yields are again rising above 2.85%. The big uncertainties are: interest rate neutrality, the pace & timing of Balance Sheet normalization, and will the ECB taper securities purchases in September?

U.S. Financial Conditions Index Vs. U.S. Fed Funds Rate

(Chart courtesy of Zerohedge.com).

The Chart above displays the four quarter-point increases in the U.S. Federal Funds Rate since December 2015 compared with the U.S. Financial Conditions Index. As can be seen, the reality is that U.S. Financial Conditions are not "tighter" since the Fed Fund Rate increases and are in fact the "easier" than ever before. The credit markets are keying off this Financial Conditions Index and not the nominal increase in the Fed Funds Rate itself. When the Fed actually wants to "tighten" it will implement Reverse Repo operations and remove accommodation from the monetary system (i.e. money-markets) and until they execute this technical operation; the Credit Markets know that the Fed is not really serious about removing the punchbowl from the party table.

30 Year U.S. Treasury Bond Yield Rises to 2.9007%

(Chart courtesy of Zerohedge.com).

The 30 Year U.S. Treasury Bond is being whipsawed back-and-forth as successive Central Bank speakers take turns sounding-off on the near-term course of interest rate policy. Watch for Bond price volatility to increase sharply over the next several weeks as a tug-of-war between "Hawks" and "Doves" emerge in the quiet period between now the next Central Bank meetings in September.

10 Year U.S. Treasury Note Yield Rises to 2.3122%

(Chart courtesy of Zerohedge.com).

This rapid turn-around in yield is most unwelcome and will put a damper on the summer homebuying season which was already one of the weakest in recent years due to lack of supply & affordability according to Larry Yun chief economist at the National Association of Realtors (NAR).

10 Year U.S. Treasury Note Yield Longer-term View back above 50-Day MA at 2.26%

(Chart courtesy of Zerohedge.com).

The above Chart does suggest that a constructive set-up is forming in the 10 Year Treasury Note with the potential to push the yield to around 2.00% over the next few weeks. As Congress turns its attention to negotiations regarding the raising of the Debt-Ceiling and U.S. Government finances once again. It is crucial that Mortgage Rates stay at or below 4.00% or demand for mortgage loans will dry up. The window of opportunity for borrowers seeking mortgage refinancing & home purchases is still open for now, but for how long?

Weekly Mortgage Rates Analysis

As can be seen from Freddie Mac's Mortgage Market Survey, last week, 30 Yr. Fixed Mortgage rates for conforming loans hit 3.92% with the rate falling 0.04% basis points from the previous week.

Treasury Prices Rise and Yields Fall Slightly for U.S. 10 Yr. and 30 Yr. Treasuries.

At the Chicago Board of Trade (CBOT): the US 10 Year Treasury Note futures Contract for September settlement closed at a price of 126'005 / 32nds; the 10 Year Note was up 14 basis points (bps) on the day, yielding 2.2872%. The US 30 Year Treasury Bond futures Contract for Sept. settlement closed at a price of 153'05 / 32nds; the 30 Year Bond was up 17 basis points (bps) on the day, yielding 2.8914%. Mortgage Rates have come off their 2017 lows and are down 0.04% bps from the previous Freddie Mac Survey last week.

Thanks to ZeroHedge.com and FreddieMac.com for Charts and Graphics.

ERATE's Daily Rate Summary

July 26, 2017

Mortgage Rates and Treasury Yields Rise.

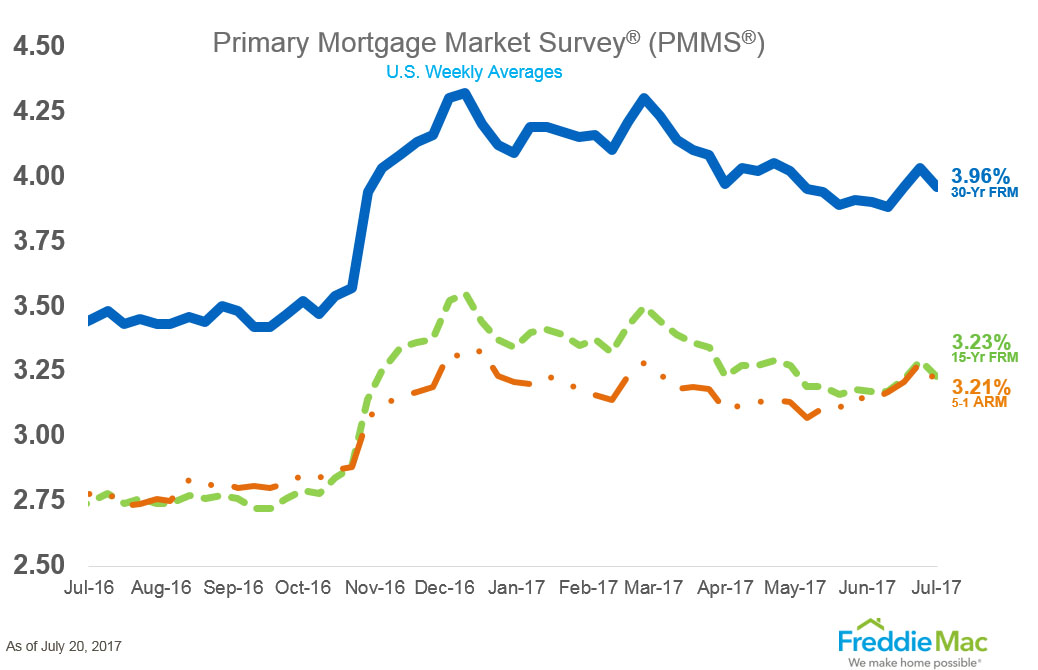

On Tuesday, Treasury bond yields and Mortgage interest rates rose slightly as market participants await news from FOMC about the path of interest rates, inflation expectations, and BS normalization. The September 10 Yr. U.S. Treasury Note stood at a yield of 2.3354% and the 30 Yr. U.S. Treasury Bond is yielding 2.9171%. 30 Year Mortgages according to Freddie Mac were around 3.96% for conforming and 4.10% for Jumbo products.

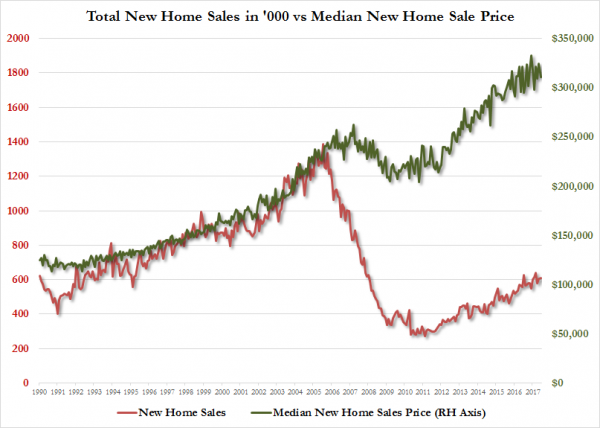

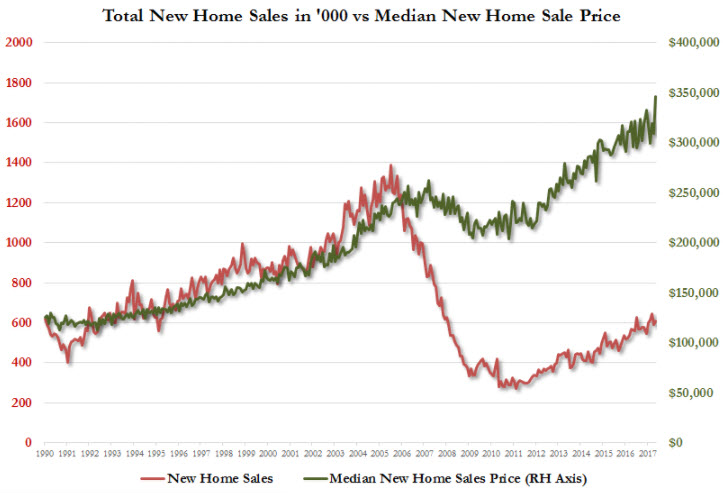

The Commerce Department said Wednesday that in June New-Home Sales edged up 0.8 percent to a seasonally adjusted annual rate of 610,000 (SAAR). Sales have registered a healthy 10.9 percent increase so far this year. May was revised down for both Sales and Median prices. This is disappointing as expectations were for a rise to 615k units (SAAR) rate. For comparison, the Chart displays the average 30 Year Mortgage interest rate for conventional loans was 4.17% in June.

New Home Sales Vs. 30Yr. Mortgage Rates (Inv)

(Chart courtesy of Zerohedge.com).

In June, the median sales price of a new home fell 3.3 percent to $310,800 down slightly from May's revised $323,400 Median Sale Price. The May median price was originally reported at $345,800 (a record).

New Home Sale (000's) vs Median Sales Prices Historical Comparison (1990 to Present)

(Chart courtesy of Zerohedge.com).

Rates have improved with rates falling back below 4.00% again (this compares to a year ago when they were at all-time lows of 3.60% this time last summer). "When taking into account the size of the U.S., new home sales are still about 30 percent below the 50-year average," said Ralph McLaughlin, chief economist at the real estate firm Trulia. "But the signs for home builders are clear: if you build, they will come."

Sales last month advanced in the Midwest and West, but purchases were unchanged in the Northeast and dropped in the South.

The June sales report indicates that the price and supply pressures will continue.

Homebuilder Optimism Vs. New Home Sale Historical (1990 to Present)

(Chart courtesy of Zerohedge.com).

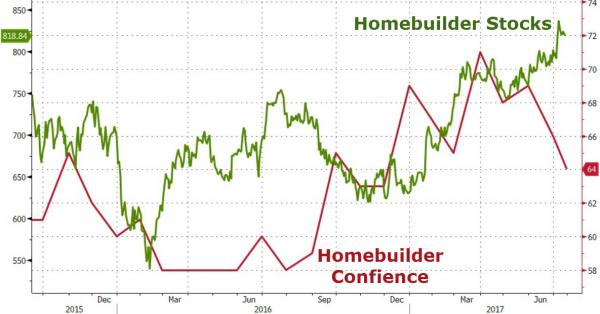

The above Chart of Homebuilder Optimism when compared to New Home Sales shows is that levels of Sales never rebounded to previous levels before the GFC; even though Homebuilder Optimism is at levels that were achieved prior to the GFC in 2006. Of course, homebuilders remain blissfully ignorant of the actual state of the housing 'recovery' - with the biggest gap between hope and home sales ever...when looking at the historical record & cyclical nature of the homebuilding industry.

10 Year U.S. Treasury Note Yield has since Risen to 2.3247%

(Chart courtesy of Zerohedge.com).

The recent action in the above Chart is disappointing as a constructive set-up was forming in the 10 Year Treasury Note at the 2.23% level with the potential to push the yield to around 2.00% over the next month. It is crucial that Mortgage Rates stay at or below 4.00% or demand for mortgage loans will dry up. The window of opportunity for borrowers seeking mortgage refinancing & home purchases is still open for now, but for how long?

Weekly Mortgage Rates Analysis

As can be seen from Freddie Mac's Mortgage Market Survey, last week, 30 Yr. Fixed Mortgage rates for conforming loans hit 3.96% with the rate falling 0.07% basis points from the previous week.

Treasury Prices Fall and Yields Rise for U.S. 10 Yr. and 30 Yr. Treasuries.

At the Chicago Board of Trade (CBOT): the US 10 Year Treasury Note futures Contract for September settlement closed at a price of 125'18.5 / 32nds; the 10 Year Note was down 18.5 basis points (bps) on the day, yielding 2.3354%. The US 30 Year Treasury Bond futures Contract for Sept. settlement closed at a price of 152'20 / 32nds; the 30 Year Bond was down 52 basis points (bps) on the day, yielding 2.9171%. Mortgage Rates have come off their 2017 lows and are down 0.07% bps from the previous Freddie Mac Survey last week.

Thanks to ZeroHedge.com, National Association of Realtors (NAR), and FreddieMac.com for Charts and Graphics.

ERATE's Daily Rate Summary

July 25, 2017

Mortgage Rates and Treasury Yields Rise Slightly.

On Monday, Treasury bond yields and Mortgage interest rates rose slightly as Credit Markets digest Central Banks interest rate intentions. The September 10 Yr. U.S. Treasury Note stood at a yield of 2.2552% and the 30 Yr. U.S. Treasury Bond is yielding 2.8345%. 30 Year Mortgages according to Freddie Mac were around 3.96% for conforming and 4.09% for Jumbo products.

In the aftermath of the June Fed Rate Hike, ECB president Mario Drahi's hawkish comments, and Janet Yellen's dovish statement last week, 30 Year Treasury Yields are again rising above 2.85%. The big uncertainties are interest rate rises almost done, what will be the pace & timing of Balance Sheet normalization, and will the ECB begin to curtail its securities purchases in September?

30 Year U.S. Treasury Bond Yield Rises to 2.9007%

(Chart courtesy of Zerohedge.com).

This rapid increase in Yields also affected the 10 Year U.S. Treasury Note as well which is the benchmark for Mortgage interest rates. With a 10 Bps rise in just over 24 hours to above 2.30%. This is indicative of a market searching for direction in the light of contradictory communication.

10 Year U.S. Treasury Note Yield Rises to 2.3122%

(Chart courtesy of Zerohedge.com).

This rapid turn-around in yield is most unwelcome and will put a damper on the summer homebuying season which was already one of the weakest in recent years due to lack of supply & affordability according to Larry Yun chief economist at the National Association of Realtors (NAR).

10 Year U.S. Treasury Note Yield Longer-term View back above 50-Day MA at 2.26%

(Chart courtesy of Zerohedge.com).

The above Chart does suggest that a constructive set-up is forming in the 10 Year Treasury Note with the potential to push the yield to around 2.00% over the next few weeks. As Congress turns its attention to negotiations regarding the raising of the Debt-Ceiling and U.S. Government finances once again. It is crucial that Mortgage Rates stay at or below 4.00% or demand for mortgage loans will dry up. The window of opportunity for borrowers seeking mortgage refinancing & home purchases is still open for now, but for how long?

Weekly Mortgage Rates Analysis

As can be seen from Freddie Mac's Mortgage Market Survey, last week, 30 Yr. Fixed Mortgage rates for conforming loans hit 3.96% with the rate falling 0.07% basis points from the previous week.

Treasury Prices Fall and Yields Rise for U.S. 10 Yr. and 30 Yr. Treasuries.

At the Chicago Board of Trade (CBOT): the US 10 Year Treasury Note futures Contract for September settlement closed at a price of 126'05 / 32nds; the 10 Year Note was down 5 basis points (bps) on the day, yielding 2.2552%. The US 30 Year Treasury Bond futures Contract for Sept. settlement closed at a price of 154'08 / 32nds; the 30 Year Bond was down 17 basis points (bps) on the day, yielding 2.8345%. Mortgage Rates have come off their 2017 lows and are down 0.07% bps from the previous Freddie Mac Survey last week.

Thanks to ZeroHedge.com, National Association of Realtors (NAR), and FreddieMac.com for Charts and Graphics.

ERATE's Daily Rate Summary

July 24, 2017

Mortgage Rates and Treasury Yields Fall.

On Friday, Treasury bond yields and Mortgage interest rates fell slightly as Central Banks hint at lower for longer interest rates due to a pause in inflation expectations. The September 10 Yr. U.S. Treasury Note stood at a yield of 2.2375% and the 30 Yr. U.S. Treasury Bond is yielding 2.8087%. 30 Year Mortgages according to Freddie Mac were around 3.96% for conforming and 4.09% for Jumbo products.

In June, Existing Home Sales fell -1.8% to 5.52 million units on a Seasonally Adjusted Annual Rate (SAAR) from May's 5.62 million unit (SAAR) rate. This is the slowest existing home selling rate since the 5.47 million unit rate print in February 2017. Existing home sales are now unchanged since September 2016, but we note that average prices are up 6.5% YoY. Interest rates & home affordability are becoming an issue in select pricier markets (coastal & major metro areas).

Existing Home Sales Vs. 30Yr. Mortgage Rates (Inv)

(Chart courtesy of Zerohedge.com).

In July, Mortgage Rates have improved with rates falling back below 4.00% again (this compares to a year ago when they were at all-time lows of 3.60% this time last summer). Existing Home Sales are only up 0.7% on a year-over-year basis, while affordability in not helping sales. Lawrence Yun, NAR chief economist, says the previous three-month lull in contract activity translated to a pullback in existing sales in June.

"Closings were down in most of the country last month because interested buyers are being tripped up by supply that remains stuck at a meager level and price growth that's straining their budget," he said.

"The demand for buying a home is as strong as it has been since before the Great Recession. Listings in the affordable price range continue to be scooped up rapidly, but the severe housing shortages inflicting many markets are keeping a large segment of would-be buyers on the sidelines."

For context, this is the weakest summer selling season since 2011... a time when seasonally sales have tended to increase...

Existing Home Sales Historical Comparison (2012 – 2017Ytd)

(Chart courtesy of Zerohedge.com).

First-time buyers made up 32 percent of sales in June, which is down from 33 percent both in May and a year ago. NAR's 2016 Profile of Home Buyers and Sellers – released in late 2016 – revealed that the annual share of first-time buyers was 35 percent.

"It's shaping up to be another year of below average sales to first-time buyers despite a healthy economy that continues to create jobs," said Yun.

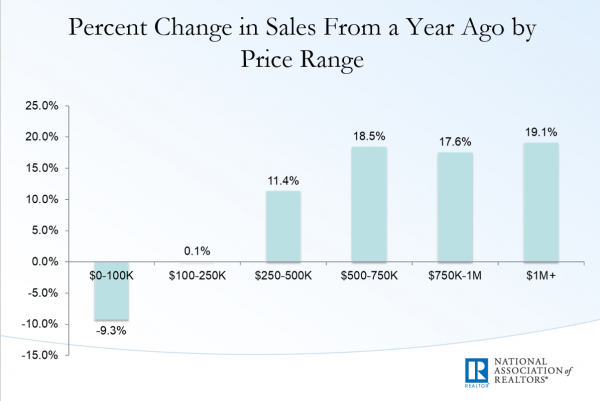

"Worsening supply and affordability conditions in many markets have unfortunately put a temporary hold on many aspiring buyers' dreams of owning a home this year." The median existing-home price for all housing types in June was $263,800, up 6.5 percent from June 2016 ($247,600).

Percent Change in Sales From a Year Ago by Price Range

Chart courtesy of National Association of Realtors (NAR).

What the Chart from (NAR) shows is that supply of affordable existing homes is being squeezed, and new home buyers are increasingly being priced out of the market.

10 Year U.S. Treasury Note Yield has since Fallen to 2.2375%

(Chart courtesy of Zerohedge.com).

The above Chart does suggest that a constructive set-up is forming in the 10 Year Treasury Note with the potential to push the yield to around 2.00% over the next few weeks. As Congress turns its attention to negotiations regarding the raising of the Debt-Ceiling and U.S. Government finances once again. It is crucial that Mortgage Rates stay at or below 4.00% or demand for mortgage loans will dry up. The window of opportunity for borrowers seeking mortgage refinancing & home purchases is still open for now, but for how long?

Weekly Mortgage Rates Analysis

As can be seen from Freddie Mac's Mortgage Market Survey, last week, 30 Yr. Fixed Mortgage rates for conforming loans hit 3.96% with the rate falling 0.07% basis points from the previous week.

Treasury Prices Rise and Yields Fall for U.S. 10 Yr. and 30 Yr. Treasuries.

At the Chicago Board of Trade (CBOT): the US 10 Year Treasury Note futures Contract for September settlement closed at a price of 126'10 / 32nds; the 10 Year Note was up 8 basis points (bps) on the day, yielding 2.2375%. The US 30 Year Treasury Bond futures Contract for Sept. settlement closed at a price of 154'25 / 32nds; the 30 Year Bond was up 23 basis points (bps) on the day, yielding 2.8087%. Mortgage Rates have come off their 2017 lows and are down 0.07% bps from the previous Freddie Mac Survey last week.

Thanks to ZeroHedge.com, National Association of Realtors (NAR), and FreddieMac.com for Charts and Graphics.

ERATE's Daily Rate Summary

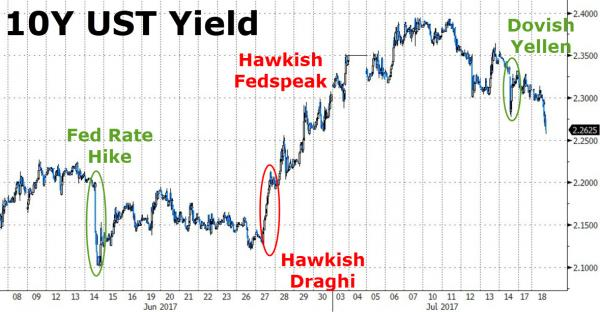

July 21, 2017

Mortgage Rates and Treasury Yields Fall Slightly.

On Thursday, Treasury bond yields and Mortgage interest rates fell slightly as ECB President, Mario Draghi's 'dovish' comments signaled he's in no hurry to taper bond buying put a bid under Treasury Prices. The September 10 Yr. U.S. Treasury Note stood at a yield of 2.2589% and the 30 Yr. U.S. Treasury Bond is yielding 2.8254%. 30 Year Mortgages according to Freddie Mac were around 3.96% for conforming and 4.09% for Jumbo products.

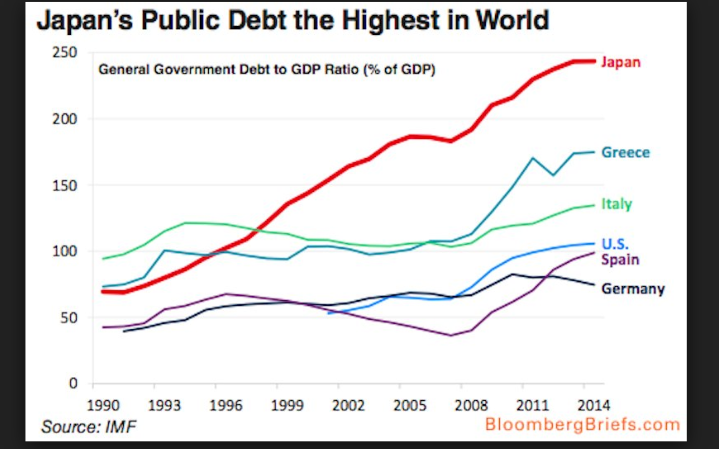

Japan's Public Debt is the highest in the world at just under 250% of GDP. Why is this important? As the chart below shows, other Western nations (including the U.S.) have breached what economist say is the key level of 90% of GDP. Anything above this level is lethal in the long-run to a Sovereign Fiat currency and economy tied to it. Mess with a medium-of-exchange and all manner of economic relationships unravel.

General Government Debt to GDP Ratio (% of GDP)

(Chart courtesy of BloombergBriefs.com).

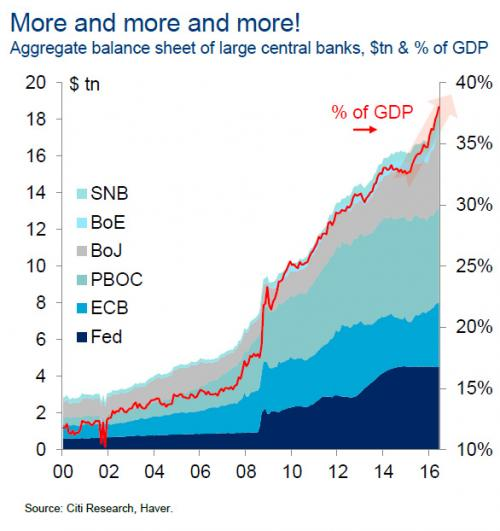

Combined Central Bank Balance Sheet >$13.5 Trillion (USD)

(Chart courtesy of Zerohedge.com).

The Central Bank's Balance Sheets now total greater than $13.5 Trillion dollars. From the Chart above the Fed, ECB, and BOJ are now on a path of unsustainable debt increase. Up until the present, the detrimental effects of this policy have been muted while the positive effects have been embraced. My economics professor taught me the lesson that 'there is no free lunch' and that consequences always follow from believing there is. The most dangerous mainstream economic idea going is that Inflation is too low. Insurance companies, defined benefit pensions and savers have been paying the price for this misguided theory. Inflation helps greatly those who are deeply indebted by making payments 'more affordable' because their paid back in cheaper dollars.

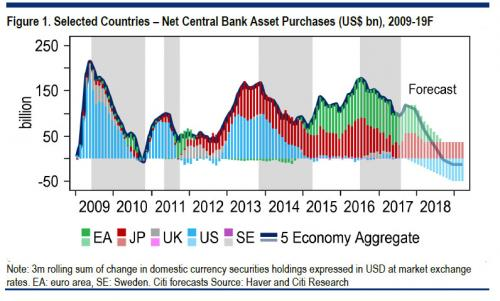

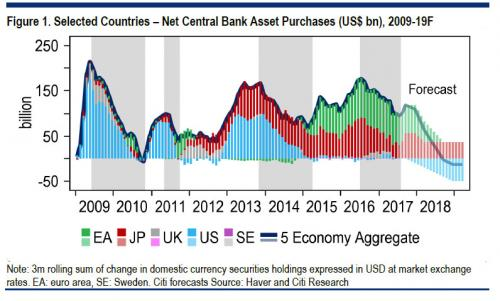

Net Central Bank Asset Purchases from 2009 to Present (US $ Billions)

(Chart courtesy of Haver and Citi Research).

If the Central Banks are going to now back away from buying additional Assets and begin to reverse course and pare down their Balance Sheets; who in the private sector is going to be the buyer and at what price? After all, Central Banks acquired these assets at full value from private sellers as the buyer of last resort when no one else could or would. There are consequences for foolish actions and I don't think that the CB's have thought through all the capital losses & market turmoil that will ensue; if in fact, true price discovery and the marketplace is allowed to work and a market clearing price is found for these securities. Can you say, 'Big Bond Bubble Top' coming?

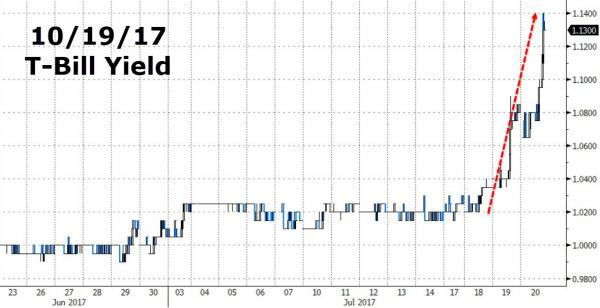

U.S. Short-term Gov't T-Bill Yields Rise to 1.13%

(Chart courtesy of Zerohedge.com).

All things financial seem calm at the moment. But the game is quietly changing and we are seeing the same signs of trouble with Money Markets as prior to the Great Financial Crisis. The Debt-Ceiling negotiations and Budget Showdown in Congress is going shock the unprepared this fall, as trust in counter-parties is again eroding under the surface. We've seen this movie before, is there no one going to be left standing the next time it falls apart and a 'Buyer of last resort' cannot be found.

10 Year U.S. Treasury Note Yield Falls to 2.2625%

(Chart courtesy of Zerohedge.com).

Here is a longer timeframe view of the 10 Yr. Treasury Note yield…

The above Chart does suggest that a constructive set-up is forming in the 10 Year Treasury Note with the potential to push the yield to around 2.00% over the next few weeks. As Congress turns its attention to negotiations regarding the raisin of the Debt-Ceiling and U.S. Government finances once again. It is crucial that Mortgage Rates stay at or below 4.00% or demand for mortgage loans will dry up. The window of opportunity for borrowers seeking mortgage refinancing & home purchases is still open for now, but for how long?

Weekly Mortgage Rates Analysis

As can be seen from Freddie Mac's Mortgage Market Survey, last week, 30 Yr. Fixed Mortgage rates for conforming loans hit 3.96% with the rate falling 0.07% basis points from the previous week.

Treasury Prices and Yields Steady for U.S. 10 Yr. and 30 Yr. Treasuries.

At the Chicago Board of Trade (CBOT): the US 10 Year Treasury Note futures Contract for September settlement closed at a price of 126'02 / 32nds; the 10 Year Note was up a half basis points (bps) on the day, yielding 2.2589%. The US 30 Year Treasury Bond futures Contract for Sept. settlement closed at a price of 154'02 / 32nds; the 30 Year Bond was up 4 basis points (bps) on the day, yielding 2.8254%. Mortgage Rates have come off their 2017 lows and are down 0.07% bps from the previous Freddie Mac Survey last week.

Thanks to ZeroHedge.com, Haver and Citi Research, BloombergBriefs.com, FreddieMac.com for Charts and Graphics.

ERATE's Daily Rate Summary

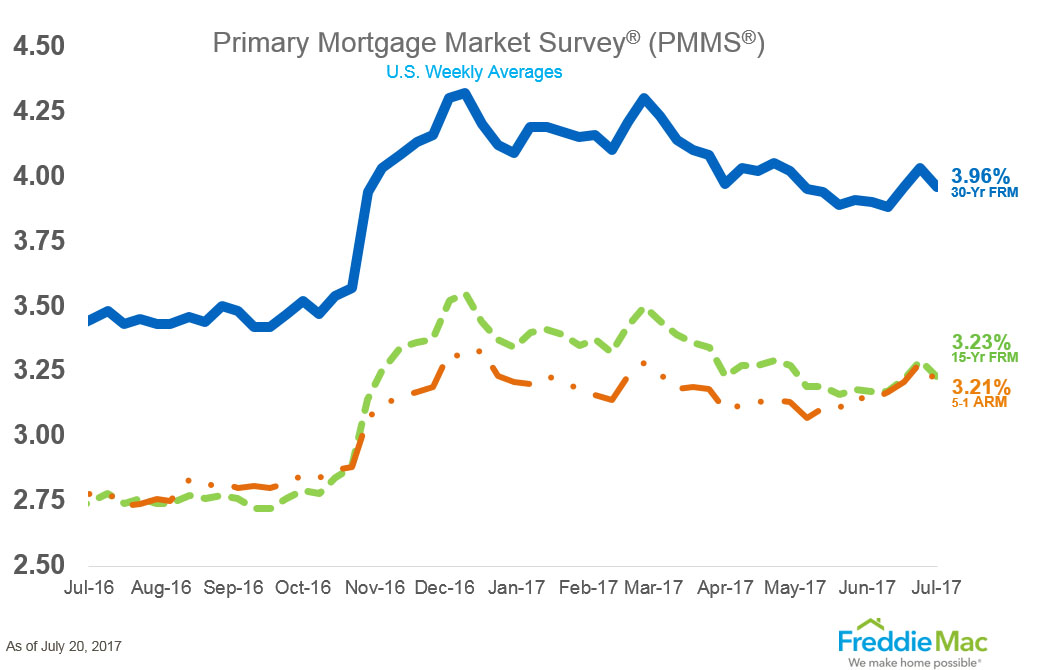

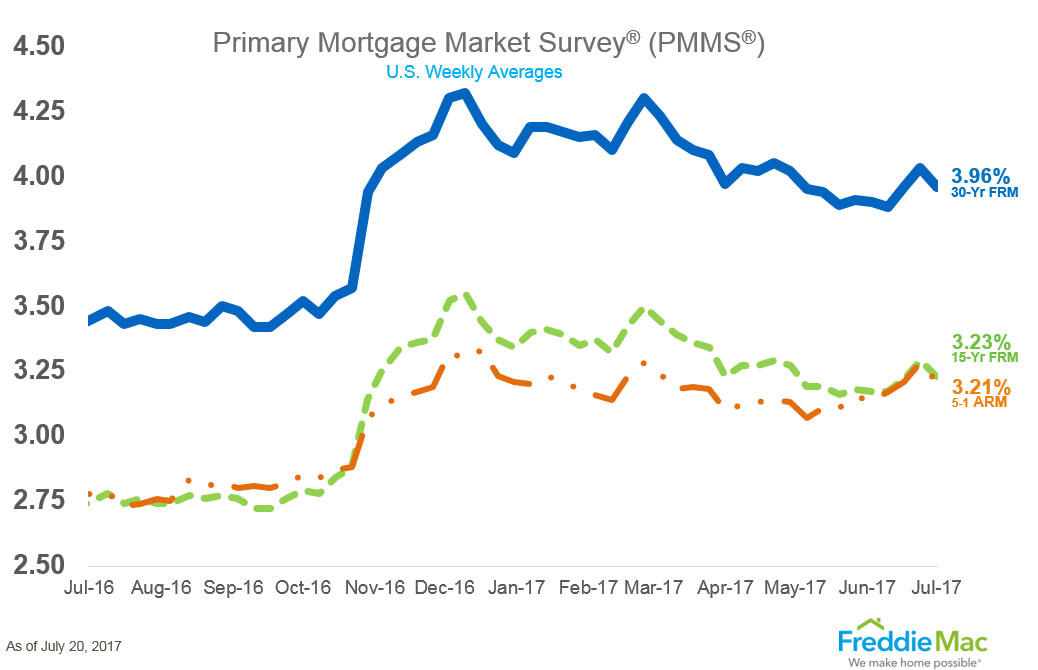

July 20, 2017

Mortgage Rates and Treasury Yields Slightly Mixed.

On Wednesday, Treasury bond yields and Mortgage interest rates were mostly unchanged as Markets awaits ECB President, Mario Draghi's comments. It is the ECB's turn for QE and next on deck will be the Kuroda's BOJ in this merry-go-round of endless & pointless liquidity. The point of no return has long been reached where Central Banks have to admit that they are the markets' (every & at all times) and there can be no real net removal of accommodation or things will break greatly in this synthetically controlled command economy. Either the CB's make up fake markets or securities go bid-less; it's that simple! The September 10 Yr. U.S. Treasury Note stood at a yield of 2.2696% and the 30 Yr. U.S. Treasury Bond is yielding 2.8514%. 30 Year Mortgages according to Freddie Mac were around 3.96% for conforming and 4.09% for Jumbo products.

As the chart below confirms, every Central Bank in this daisy-chain of Quantitative Easing has now taken their turn and each CB Balance Sheet is now individually at or over $4.5 Trillion. Just stop and think what this represents: many multiples of future annual World GDP have been conjured-up (borrowed into existence) to pull future consumption into the present to fill the hole (depression) in present world-wide consumptive activity for going-on nine years to solve a problem initially on the order of only $800B during the GFC. Pitiful problem analysis, reasoning & solutions applied from the smartest guys in the room!

Central Bank Balance Sheets (USD) (Chart courtesy of Zerohedge.com).

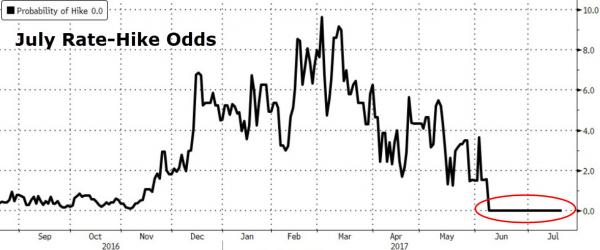

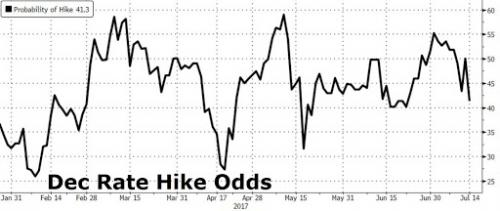

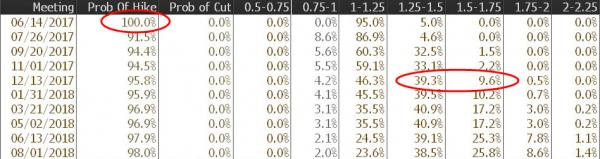

From the Chart below the Odds of a surprise FOMC July Rate-Hike have flatlined at 0% probability. The CB's really have no intention to "normalize" anything; interest rates, balance sheets, liquidity, and/or QE because they can't and know the system will destabilize again the moment they stop becoming the "Market" for assets. Their cornered and committed to doing the same things that haven't worked up to this point, hoping for a different outcome. Definition of Insanity…

July Rate-Hike Odds Hit 0%

(Chart courtesy of Zerohedge.com).

As can be seen from the from the below Chart courtesy of Haver and Citi Research the CB's have been taking turns the U.S. Fed is mostly done since 2014, it was the Bank of Japan's turn next, and now ECB is in the driver's seat of Quantitative Easing. What happens when/if the 2019 Forecast is true and it all ends? Will the markets suddenly come back to life on their own and provide liquidity, true real-time price-discovery for asset values again and make fake markets disappear?

Net Central Bank Asset Purchases from 2009 to Present (US $ Billions)

(Chart courtesy of Haver and Citi Research).