Maintaining credit health much like maintaining physical health

by Broderick Perkins

(10/23/2012) - Monitoring your credit is a lot like preventive health care. Keep tabs on your credit and your health - and chances are you'll spot problems earlier and correct them sooner.

Regular checkups with your physician allow you to catch early indicators of failing health and that gives you a better shot at a quick, long-term cures. That means a longer, more active life.

Monitoring your credit, likewise catches early signs trouble, giving you a jump on making things right and maintaining excellent credit for life. That means a more active credit life.

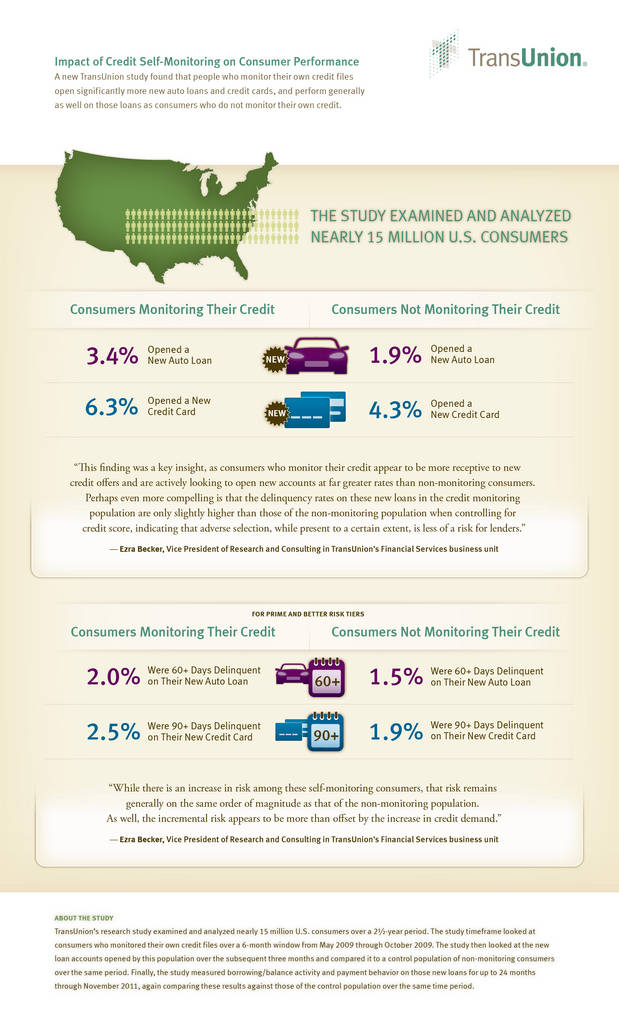

Credit reporting agency Transunion recently discovered that consumers who monitor their credit files have significantly more credit accounts than those who don't bother to monitor their credit.

"Our study started with the conjecture that individuals who monitor their credit health might be motivated the same way as people who monitor their physical health," said Ezra Becker, vice president of research and consulting in TransUnion's financial services business unit.

"We have found that consumers who monitor their credit tend to fall into two groups: credit-healthy consumers who wish to maintain that health and/or guard against identity theft; and riskier consumers who are looking to take proactive measures to better manage their credit profiles in anticipation of acquiring additional credit," Becker added.

That's particularly important for mortgage shoppers. Underwriting standards are as strict as they've ever been. The healthier your credit report, the higher your credit score, and the greater chance you'll have landing a mortgage at the lowest cost.

TransUnion's "Impact of Credit Self-Monitoring on Consumer Performance" study revealed that 3.4 percent of consumers who monitored their credit opened a new auto loan, while only 1.9 percent of consumers who did not monitor their credit opened an auto loan.

The same was true for general-purpose credit cards. Nearly 6.3 percent of consumers who monitored their credit opened new credit cards. However, only 4.3 percent of consumers who didn't monitor their credit opened new credit card accounts. The study actually found that the credit scores were slightly lower for those monitoring their report than those who didn't monitor their credit report, but that makes sense.

"The difference in score distribution tends to support the theory that many self-monitoring consumers are doing so because they wish to improve their credit profiles," said Becker.

Anyone can monitor their credit reports by applying for a free credit report from any of the big three credit reporting agencies — Equifax, Experian and TransUnion — through AnnualCreditReport.com, the only federally approved service for free credit reports.

Consumers are allotted one free credit report each year from each of the three different agencies. That means you actually get three free credit reports each year.

Stagger access to each credit report over a year so that you receive one every four months and you'll keep tabs on what's happening to your report.

For example:

• In April, obtain the Equifax report.

• In August, obtain the Experian report.

• In December, obtain the TransUnion report.

If you've never had a look at your credit report, get all three now and pace your access next year.

Go over your report with a fine tooth comb looking for errors you can correct and to dispute items you deem problematic — say black marks still on your report after seven or 10 years.

You'll have to pay for your credit score but the nominal cost of $15 or less is worth the price of admission.

"This finding was a key insight, as consumers who monitor their credit appear to be more receptive to new credit offers and are actively looking to open new accounts at far greater rates than non-monitoring consumers," said Becker.

Click the infographic below to expand and obtain more information.

Other related articles:

Understanding Credit Cards: Who Uses Credit Scores?

Understanding Credit Cards: Top 5 Credit Score Myths

Understanding Credit Cards: Building Credit for Newbies

Understanding Credit Cards: The 5 Components of a Credit Score

The Paradox of Credit: The Secrets of Good Credit that Defy Logic

Understanding Credit Cards: Checking Your Credit

Understanding Credit Cards: What is Credit?

Understanding Mortgages: What is a Credit Score?

Cashing in on your credit score

Fully free credit scores long overdue

Site to See: Federal Reserve's 'Credit Reports and Credit Scores'

Fannie Mae & Jumbo Mortgage Rates

Just One Click! = Current Rate Chart

Start by selecting your state

Broderick Perkins

Home equity line of credit vs. home equity loan

Realty agents offer buyers pre-purchase credit, mortgage tips

Continued partisan attempts to undermine the CFPB victimize mortgage

Larger down payment crucial in today's low-inventory, multiple-offer housing market

Site to See: Freddie Mac's CreditSmart

Online mortgage videos a good mortgage news

Consumer Financial Protection Bureau may not be enough to clean up mortgage

How much home will the median price buy?

High-cost areas benefitting from jumbo loan boom

Mortgage credit slowly loosening, but many restraints still in place

Mortgage co-signing not what it used to be

Inside the lessons of homeownership counseling

What's to learn from homeownership counseling?

What can you do about higher FHA loan costs? Not a lot

Fundamentals apply when applying for a mortgage

Larger down payment prompts lender, seller largess

Erate Update: Which Way Mortgage Rates?

Mortgage banker vs. mortgage broker

The true cost of homeownership

No-marriage mortgages between couples are red flag parades

How much house will a conforming loan buy?

Real estate agents' role in the mortgage application process

Home Equity Line - Documentation

Home Equity Line vs Second Mortgage

Which Secondary Financing is best for me?

Home Equity Loans: Paychecks from your Home

Home Equity Loan Shopping: Tips and Types

Home Equity Line New Appraisal

Home Equity No Income Qualifier

Home Equity Typical Loan Terms

Home Equity Loan vs Refinance First Mtg

Second Mortgage, HELOC for Invest Prop

Use Your Home to Get Away: Home Equity Loans with Frequent Flyer Programs

Lower your monthly payments Debt Consolidation Calculator