Weekly Economic Summary

Monday, September 12th

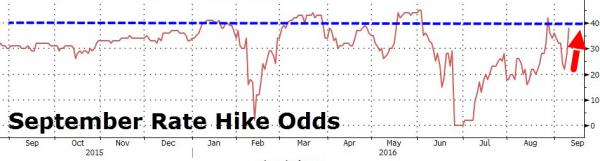

What Happened? Last weeks' U.S. Non-Farm Payroll Report came in below expectations at 150k jobs created. The immediate reaction of observers in the Bond Market was positive to bid up the price of bonds sending 10 Year U.S. Treasuries yields down toward 1.50%. The odds of a September or December interest rate hike started to go down. All good!

But then a series of Fed officials came out with comments which seemed to indicate that September was still "in play" for an interest rate rise...

On Tuesday and Wednesday, the Bond markets shrugged this off and continued to rally on poor economic "macro data" about the economy.

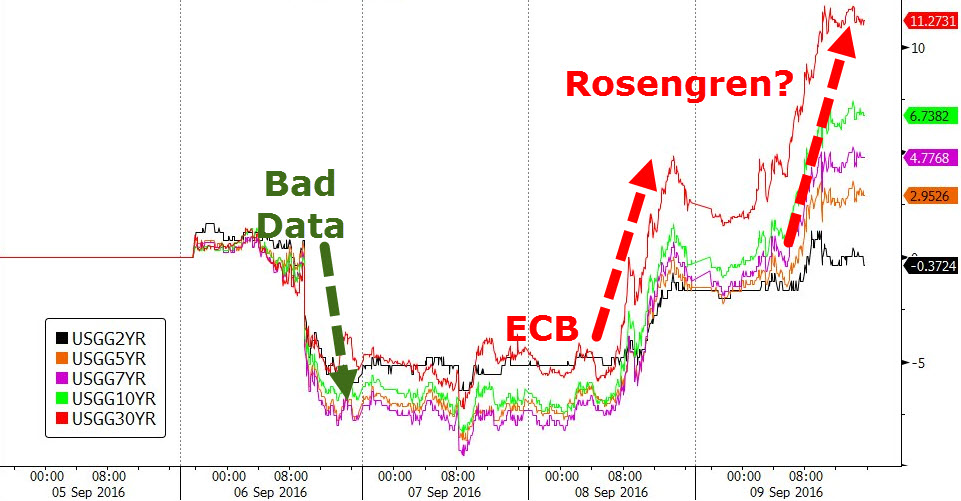

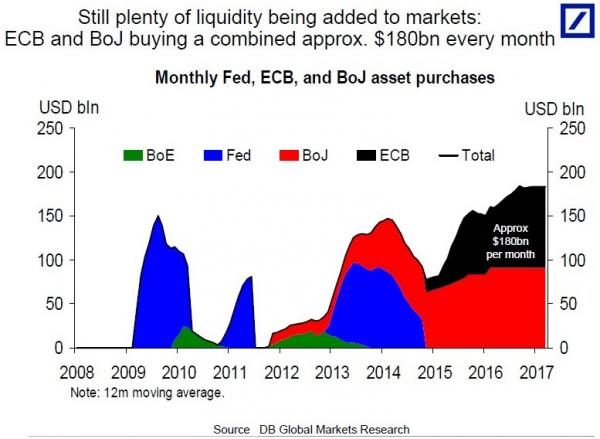

However, as it turned out the bond market was really focused on EC's statements from Mario Draghi and the outlook for continued bond buying in Europe. The ECB and BoJ were already in the midst of a program of Quantitative Easing (QE) that was buying some $180 billion of all sorts of Sovereign and Corporate debt that was scheduled to stretch out until March of 2017 and ultimately purchase some $1.2 Trillion in debt within the scope of its mandate.

However, strict guidelines were operating against ceilings which as it turned out were being run up against, quickly. As a technical matter, these rules were fast becoming an impediment to further European Central Bank bond buying and overall QE expansion and Mario Draghi's comments were seen as crucial to continuation of this monetary regime. Well he punted. He did not say the crucial words, "we'll do anything it takes" this time and bond holders who were front-running CB future purchases of bonds panicked en masse and started selling.

As a result, the yields in Sovereign and Corporate debt around the world began to rise pricing in no further increase in QE and a possible Federal Reserve rate hike in either September or December.

Japanese Gov't bond yields rose.

German Gov't bund yields increased from below zero interest rates to near zero yields once again.

Anticipating that stable Macro data increases the odds of a Fed Rate hike is on the table at the September 21st meeting.

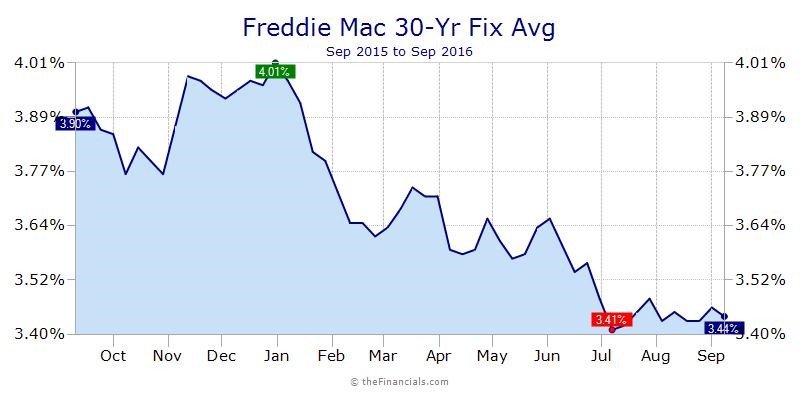

As a consequence, the U.S. 10 Yr. Bond yield also rose to as high as 1.67% which put increasing pressure on Mortgage rates which have jumped significantly in the last few days and may be heading over 3.50%.

Weekly Mortgage Rates Analysis

We do not know the future, but this period of super-low interest rates and unprecedented monetary policy moves may be coming to an end and "normalization" of the yield curve may be at hand. This would be a good time to lock in your Rates!!!

This weeks' key Economic releases, courtesy of www.zerohedge.com:

And the full US weekly event breakdown courtesy of Goldman:

Monday, September 12

- 08:05 AM Atlanta Fed President Lockhart (FOMC non-voter) speaks: Federal Reserve Bank of Atlanta President Dennis Lockhart will speak about monetary policy and the economic outlook at the National Association for Business Economics' national meeting in Atlanta, Georgia.

- 01:00 PM Minneapolis Fed President Kashkari (FOMC non-voter) speaks: Federal Reserve Bank of Minneapolis President Neel Kashkari will participate in a discussion about the U.S. economy and too-big-to-fail at the St. Paul Building Owners and Managers Association's Thought Leader Seminar and the St. Paul Port Authority's Expert Forum in St. Paul, Minnesota. Audience Q&A is expected.

- 01:15PM Governor Brainard (FOMC voter) speaks: Federal Reserve Board Governor Lael Brainard will discuss the economic outlook and monetary policy at an event titled, "Beyond Interest: The Economic Outlook and Monetary Policy" at the Chicago Council on Global Affairs in Chicago, Illinois. Audience and media Q&A is expected. Governor Brainard wrote down a one-hike baseline for 2016 in June.

Tuesday, September 13:

- 06:00 AM NFIB small business optimism index, August (consensus 94.8, last 94.6)

- 02:00 PM Monthly budget statement, August (consensus -$105.5bn, last -$112.8bn): Consensus expects the federal budget deficit declined to -$105.5bn in August.

Wednesday, September 14

- 08:30 AM Import price index, August (consensus -0.1%, last +0.1%): Consensus expects the import price index to decline by 0.1% in August. Last month, the headline index advanced for the fifth straight month despite a softening in imported fuel prices.

Thursday, September 15

- 8:30 AM Retail sales, August (GS -0.2%, consensus -0.1%, last flat); Retail sales ex-auto, August (GS +0.2%, consensus +0.2%, last -0.3%); Retail sales ex-auto & gas, August (GS +0.3%, consensus +0.3%, last -0.1%); Core retail sales, August (GS +0.2%, consensus +0.4%, last flat): We expect headline retail sales to soften by 0.2%, reflecting lower gasoline prices and soft auto sales figures in August. Core retail sales are likely to increase by 0.2% after a flat July print.

- 08:30 AM PPI final demand, August (GS +0.1%, consensus +0.1%, last -0.4%); PPI ex-food and energy, August (GS flat, consensus +0.1%, last -0.3%); PPI ex-food, energy, and trade, August (GS flat, consensus +0.1%, last flat); We expect PPI ex-food, energy, and trade to remain flat, and for headline PPI to increase by 0.1%. Last month, PPI was much softer than anticipated, with the headline index falling by 0.4% while prices ex-food and energy fell by 0.3%.

- 08:30 AM Initial jobless claims, week ended September 3 (GS 265k, consensus 265k, last 259k); Continuing jobless claims, week ended August 27 (consensus 2,150, last 2,144k): We expect initial jobless claims to edge up to 265k after moving down to 259k last week. The largest decline in claims was in Louisiana after two weeks of elevated claims following the recent flooding along the Gulf Coast. California and Illinois reported the largest increases in claims.

- 08:30 AM Philadelphia Fed manufacturing index, September (GS 0, consensus 1.0, last 2.0): We expect the Philadelphia Fed manufacturing survey to remain at 0 in September. Last month, the Philly Fed index signaled a modest expansion in manufacturing activity, although the majority of the report's underlying components softened.

- 08:30 AM Empire manufacturing survey, September (consensus -1.0, last -4.2): Consensus expects a modest pickup in the Empire manufacturing survey, after a slight miss in the August report.

- 08:30 AM Current account balance, Q2 (consensus -$120.8bn, last -$124.7 bn)

- 09:15 AM Industrial production, August (GS -0.2%, consensus -0.2%, last +0.7%); Manufacturing production, August (GS -0.3%, consensus -0.3%, last +0.5%); Capacity utilization, August (GS 75.7%, consensus 75.7%, last 75.9%): We expect that industrial production declined by 0.2% (mom) in August after a 0.7% gain in July, due to softer utilities output and lower motor vehicle manufacturing.

- 10:00 AM Business inventories, July (consensus +0.1%, last +0.2%): Consensus expects a 0.1% rise in inventory levels in July, following a 0.2% gain in June.

Friday, September 16

- 08:30 AM CPI (mom), August (GS +0.12%, consensus +0.1%, last +0.22%); Core CPI (mom), August (GS +0.17%, consensus +0.2%, last +0.09%); CPI (yoy), August (GS +1.0%, consensus +1.0%, last +0.8%); Core CPI (yoy), August (GS +2.2%, consensus +2.2%, last +2.2%): We expect that core CPI rose by 0.17% in August, following a soft 0.09% increase in July. On a year-on-year basis, core CPI likely rose by 2.2%, in line with last month. We estimate headline consumer prices increased by 0.12% last month, at a slower pace than July due to softer food and energy prices. On a year-on-year basis, the headline index likely increased by 1.0%.

- 10:00 AM University of Michigan consumer sentiment, September preliminary (GS 91.5, consensus 90.6, last 89.8): We expect the University of Michigan consumer sentiment index to improve in the September preliminary estimate, following last month's slight decline.

Source: Deutsche, BofA, Goldman

Get the Updated and Improved Mortgage Rates App from ERATE.com

- Why housing consumers say you need a real estate agent

- Lenders Double Down on Car-Title Loans Attempting to Stay Ahead of Regulators

- Need Cash Fast? Beware of Greedy Lenders Waiting to Exploit You

- Mortgage Rates and the Stock Market: Understanding the Relationship

- The ERATE® Resource Guide to No-Closing-Cost Refinancing

- You and Your Credit; Make it a Happy Ongoing Relationship

- Principal Reduction: New Programs, More Controversy

- Understanding Mortgages: Mortgage Paperwork

- What is Mortgage Interest?

- Mortgage Terms & Definitions

- Understanding Mortgages: Types of Mortgages

- Understanding Mortgages: How to Get a Mortgage

- What is a Short Sale?

- Understanding Mortgages: Buy or Rent?

- Understanding Mortgages: Working with a Real Estate Agent

- Understanding Mortgages: Working with a Real Estate Agent

- Understanding Credit Cards: Top Mistakes

FREE Mortgage Rate Widgets

Your State's Rates or National Rates Get this Widget for any State you want