Daily Rate Summary

Monday, July 17th, 2017

Mortgage Rates and Treasury Yields Fall Modestly.

On Friday, Treasury bond yields and Mortgage interest rates fell modestly as credit markets digested Fed Chairman, Janet Yellen's remarks at her semi-annual testimony to Congress last week. The consensus is now a little muddled as to whether September or December will be the final rate hike in this tightening cycle. Should Janet Yellen be considered a ‘short-timer' in her position as the Fed Chairmen as her term is up in January 2018? Has she decided to sail off into the sunset without having to make the tough decision to significantly tighten Monetary conditions & take the punchbowl away just when the party was getting started.

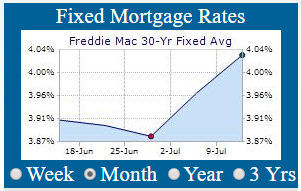

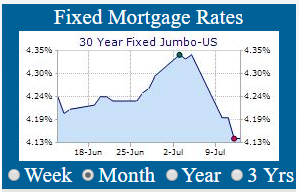

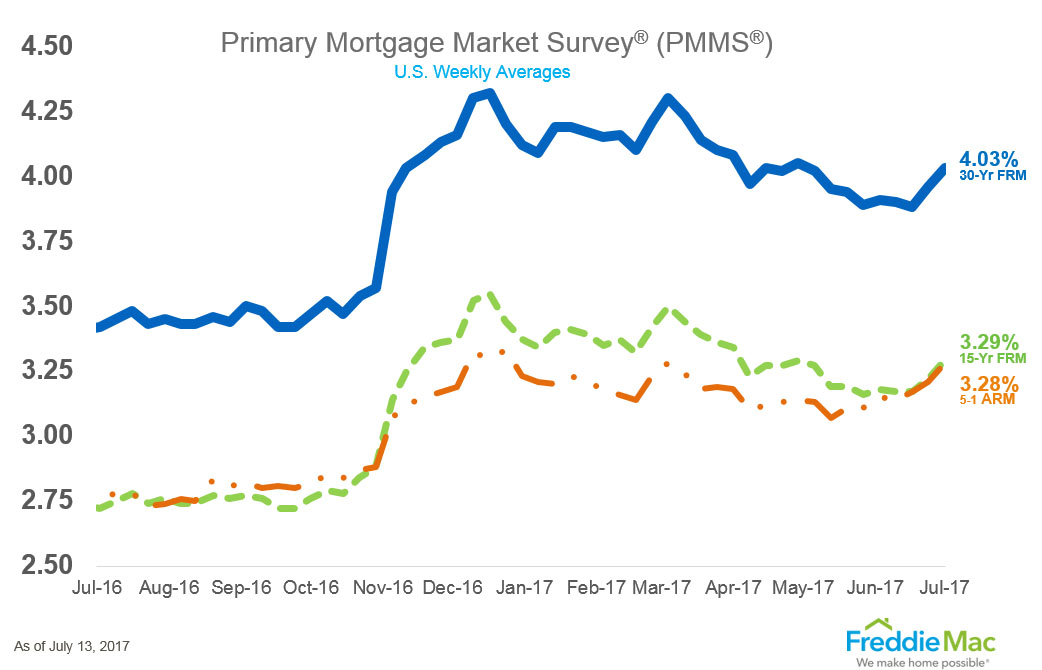

The September 10 Yr. U.S. Treasury Note stood at a yield of 2.3319% and the 30 Yr. U.S. Treasury Bond is yielding 2.9195%. 30 Year Mortgages according to Freddie Mac were around 4.03% for conforming and 4.14% for Jumbo products.

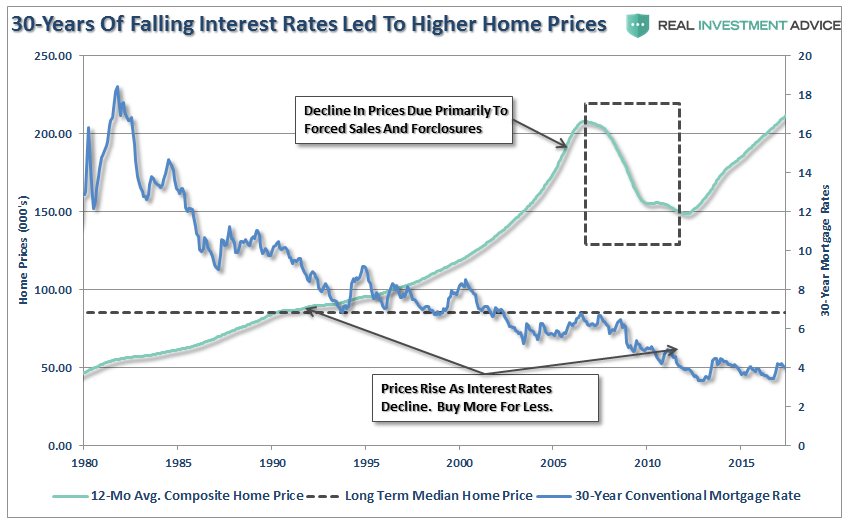

The multi-decade secular trend lower in Mortgage Rates has allowed U.S. Housing Prices to gently rise then accelerate via inflation from under $50k in 1980 to over $210k in 2017 (see chart below).

30-Year Mortgage Rates Vs. Home Prices (000s) (Real Investment Advice).

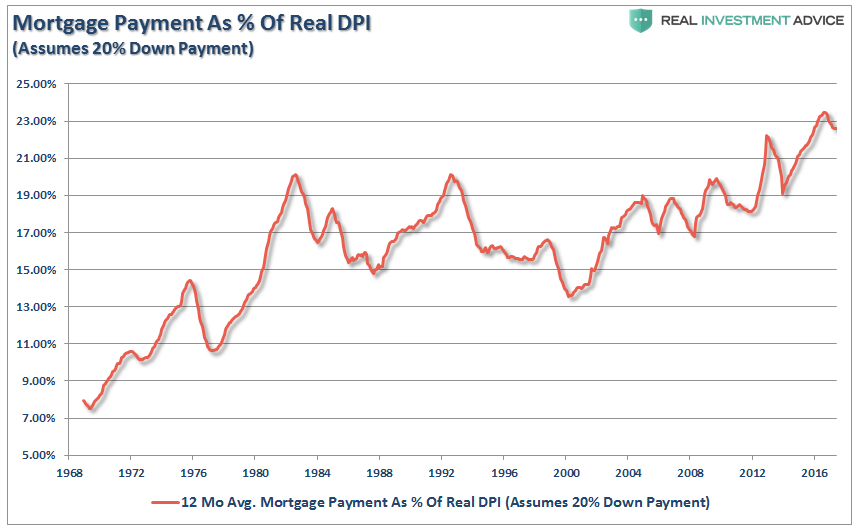

Because home borrowers for the most part buy a monthly mortgage payment and not a home price or interest rate, per se; widespread problems with housing un-affordability have been masked by a number of factors including: additional working spouse, greater levels of educational attainment, and general inflation in corporate SG&A (see chart below).

Mortgage Payment As % of Real Disposable Personal Income (DPI)

(Chart courtesy of Real Investment Advice).

The Mortgage Payment as a percentage of Real Disposable Personal Income (DPI) has been in a stable range of 15% to 20% for decades. The addition of a working spouse helped us jump from the 7% to 15% of DPI levels in the 1970's. General inflation, Advance degrees and specialized training & skills (when in the past Businesses and Corporations were inclined to pay additional compensation for more highly skilled professional workforce) moved us along the path into the 2000's.

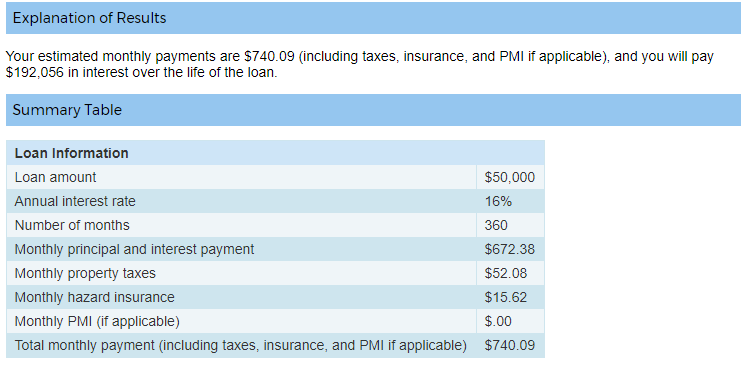

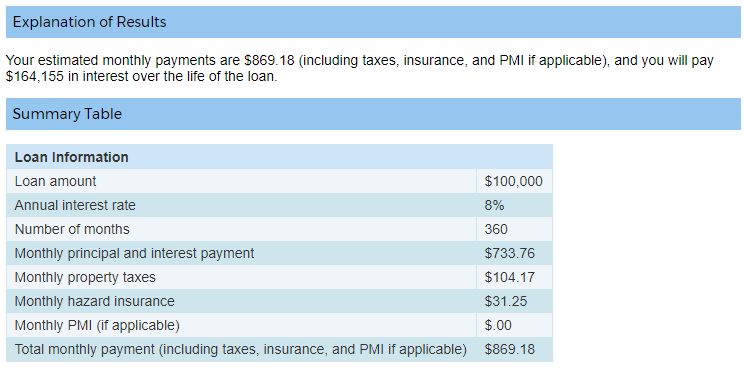

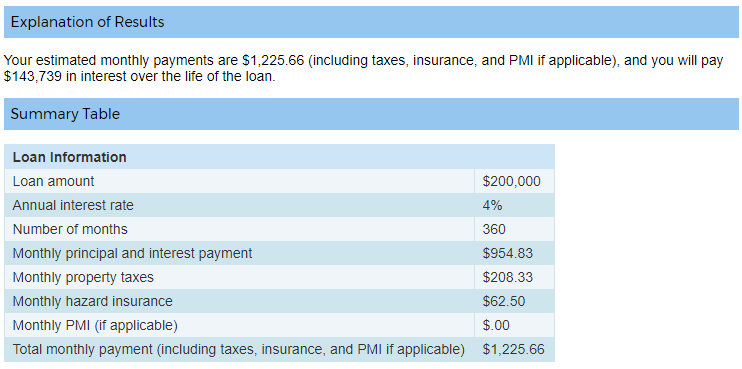

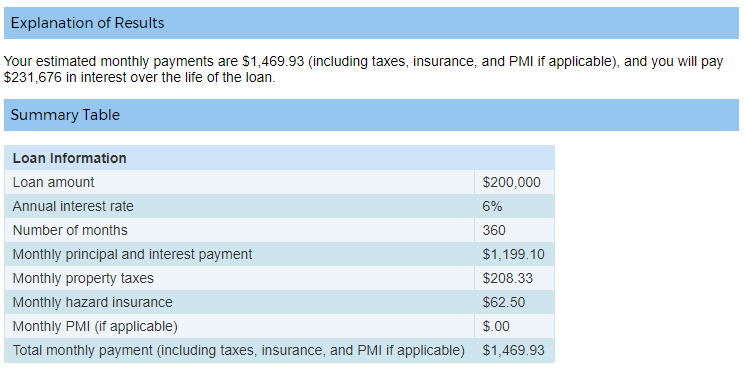

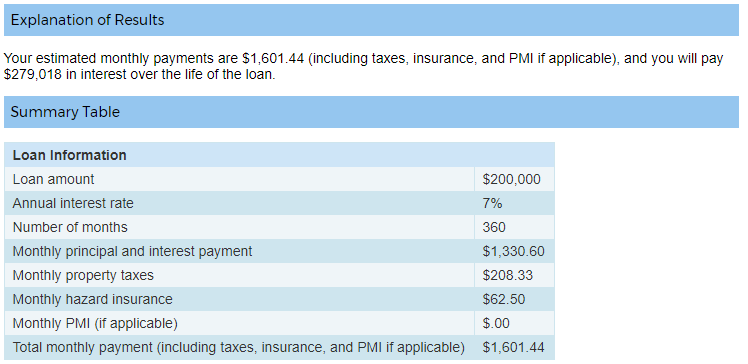

So, if I borrowed $50k at 16% in 1980, $100k at 8% 1995, and $200k at 4% in 2017 to buy a hypothetical home the amount of initial 1st year annual interest payments on those mortgages would be nearly equal at $8,000/year in the first crucial year of home ownership. The initial monthly payments during the amortization schedules are $673, $734, and $955/month. A stable though clearly inflationary financial dynamic is thus maintained; all due to the secular trend in Mortgage Interest rates (see Mortgage Calculator Results below).

Mortgage Calculator Results for Each Scenario (Courtesy of Erate.com).

The Mortgage Calculator results show that as the hypothetical Home appreciates fourfold in price between 1980 and 2017; the Secular trend lower in mortgage interest rates over that interval masks most of the erosion in home affordability (higher capital cost) and the mortgage payment only has risen from $672/month to $955/month in principal and interest (remember 1st year interest is still the exact same at $8,000).

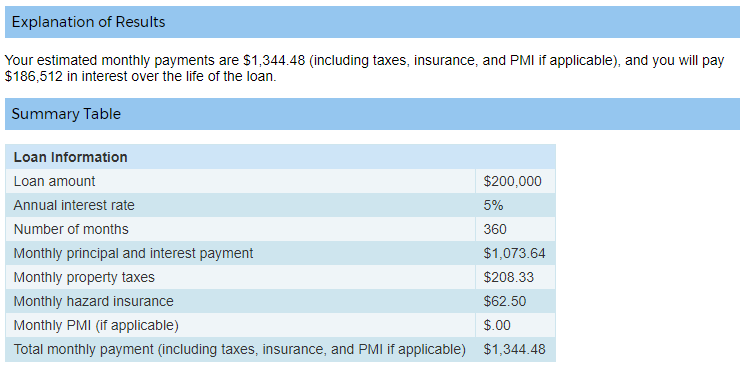

However, if instead mortgage rates now begin a secular increase from 4.00% in 2017 to 5% 2020, and then 6% in 2023 the math becomes very different and the stable dynamic disappears (unless businesses step up and increase Wages & Salaries consistently every year going forward).

As total interest & property taxes paid over the holding period balloons. The property tax problem is most acute because when you buy determines your fully capitalized cost of local government that your cohort is locked into paying (plus 2% per year increase see Prop. 13) and the inflation in the cost of local government has been and will continue to escalate at a rate far greater than inflation because politicians refuse to or can't deliver cost-improvements for the services rendered like private businesses and simply escalate their cost structures to infinity.

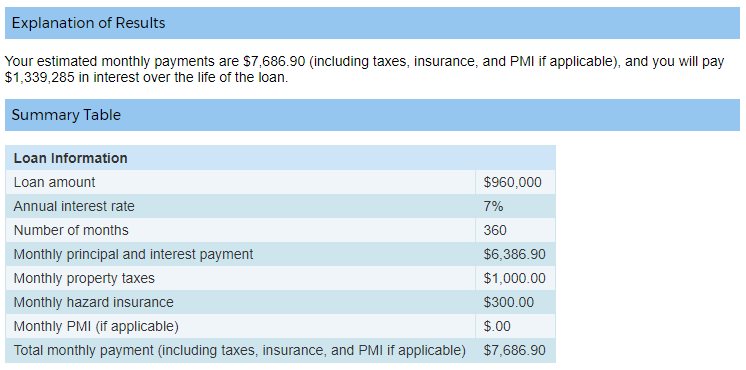

The scheme becomes untenable the higher property prices go so that you get a situation where a long-time owner who pays $2,000 a year in property taxes is sitting next to a recent owner who pays $12,000 a year in property taxes (Santa Clara County, CA) for neighbors with the exact same home.

The newer owner while nominally being able to afford the monthly mortgage payment is going to pay $300k in greater property taxes and $1.147m in greater mortgage interest than earlier owner over their lifetime of ownership and will receive the same level of local gov't services. This is Ponzi finance at its best.

There is a clear limit to how far this dynamic can be pushed and still find people who are willing to sacrifice home economics for ownership rights. In the Silicon Valley, the $200k home is now $1,200,000 and property taxes are $1,000/month. Would you sign on for this…

Unless you are a public-sector worker who just gamed the 80% of final year compensation formula give away with accrued vacation & overtime pay (sorry private sector employees); no one is going to be able to afford paying for these embedded cost structures and save for their own retirement & medical costs at these levels when mortgage interest rates normalize. Goodbye housing…

Weekly Mortgage Rates Analysis

As can be seen from Freddie Mac's Mortgage Market Survey, last week, 30 Yr. Fixed Mortgage rates for conforming loans hit 4.03% rising another 0.07% basis points from the previous week.

Treasury Prices Rise and Yields Fall for U.S. 10 Yr. and 30 Yr. Treasuries.

At the Chicago Board of Trade (CBOT): the US 10 Year Treasury Note futures Contract for September settlement closed at a price of 125'21.5 / 32nds; the 10 Year Note was up 8.5 basis points (bps) on the day, yielding 2.3319%. The US 30 Year Treasury Bond futures Contract for Sept. settlement closed at a price of 152'20 / 32nds; the 30 Year Bond was up 14 basis points (bps) on the day, yielding 2.9195%. Mortgage Rates have come off their 2017 lows and are up 0.07% bps from the previous Freddie Mac Survey last week.

Thanks to Real Investment Advice, ZeroHedge.com and FreddieMac.com for Charts and Graphics.

Disclaimer: The Information & content in this message is solely the opinion of the author and believed to be from reliable sources. Charts and tables contained herein were taken from other sources and a best effort was attempted by the author to give attribution where possible. None of this material should be construed as fact, and is not intended for use by reader as investment advice or relied upon for making financial decisions.

Get the Updated and Improved Mortgage Rates App from ERATE.com

- Why housing consumers say you need a real estate agent

- Lenders Double Down on Car-Title Loans Attempting to Stay Ahead of Regulators

- Need Cash Fast? Beware of Greedy Lenders Waiting to Exploit You

- Mortgage Rates and the Stock Market: Understanding the Relationship

- The ERATE® Resource Guide to No-Closing-Cost Refinancing

- You and Your Credit; Make it a Happy Ongoing Relationship

- Principal Reduction: New Programs, More Controversy

- Understanding Mortgages: Mortgage Paperwork

- What is Mortgage Interest?

- Mortgage Terms & Definitions

- Understanding Mortgages: Types of Mortgages

- Understanding Mortgages: How to Get a Mortgage

- What is a Short Sale?

- Understanding Mortgages: Buy or Rent?

- Understanding Mortgages: Working with a Real Estate Agent

- Understanding Mortgages: Working with a Real Estate Agent

- Understanding Credit Cards: Top Mistakes

FREE Mortgage Rate Widgets

Your State's Rates or National Rates Get this Widget for any State you want