Daily Rate Summary

Friday, January 12th, 2018

Mortgage Rates and Treasury Yields Fall.

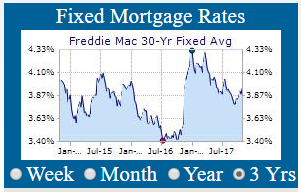

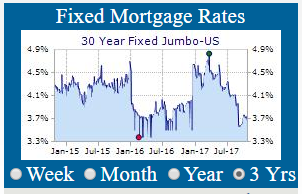

On Thursday, Treasury bond yields and Mortgage interest rates fell slightly as Bond investors are fleeing curve flattening trades that they put on earlier in the year. Stocks are still hot! and making a run to all-time highs on the averages. The allure of fast gains on a frothy stock market outshines boring bonds. Nervous investors mull economic signals and the impact of the Tax cut on economic growth potential. Bond investors are looking at the possibility of lower-for-longer policy as an incentive to buy bonds. 10 Yr. Treasury Note stood at a yield of 2.5367% and the 30 Yr. U.S. Treasury Bond is yielding 2.8673%. 30 Year Mortgages according to Freddie Mac were around 3.99% for conforming and 4.12% for Jumbo products.

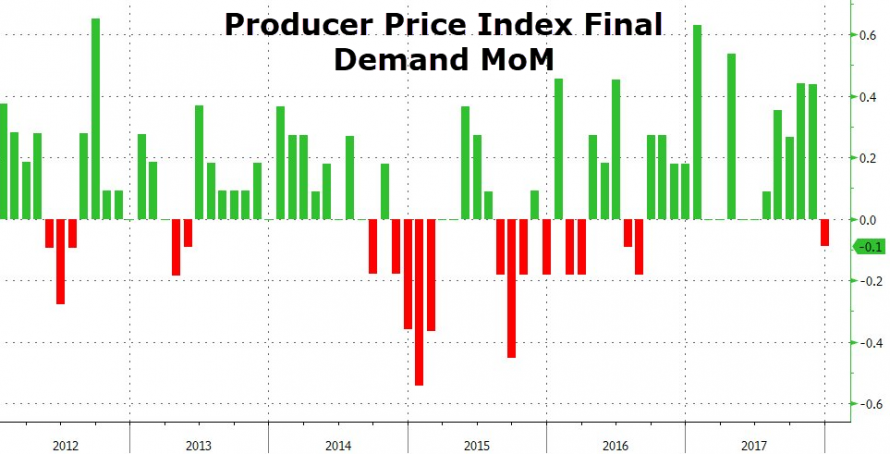

According to Zerohedge.com, “Following the deflationary core import price index print, producer prices dropped 0.1% in December, missing expectations dramatically and 'deflating' the most since Aug 2016.”

The synopsis as reported by the BLS report: Final demand ex food, energy fell 0.1% m/m vs est. up 0.2%. Final demand rose 2.6% y/y vs est. up 3%. Final demand ex food, energy rose 2.3% y/y vs est. up 2.5%. Final demand ex food, energy and trade services rose 0.1% m/m. Final demand personal consumption fell 0.2% m/m. Final demand personal consumption rose 2.6% y/y.

Producer Price Index (PPI) Falls -0.10% in December.

(Chart courtesy of Zerohedge.com).

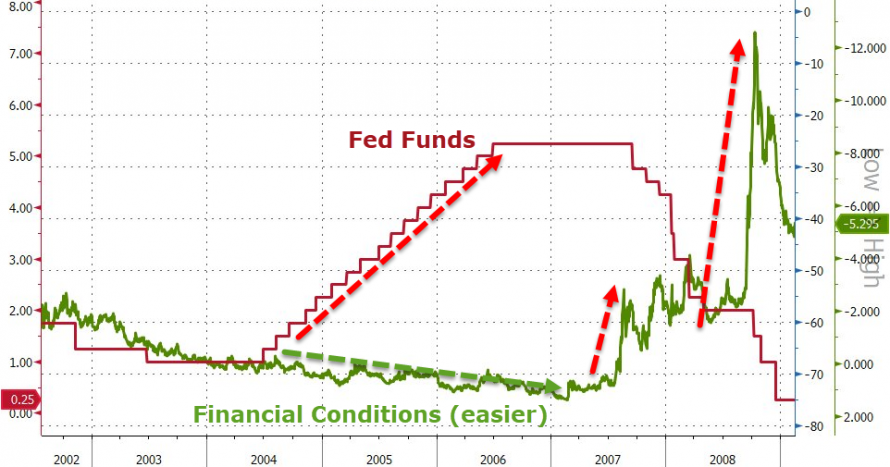

“In today's most anticipated Fed speech, outgoing NY Fed president Bill Dudley delivered keynote remarks at a SIFMA event in New York, titled "The Outlook for the US Economy in 2018 and Beyond", in which he warned bluntly that the prospect of U.S. economic overheating "is a real risk over the next few years" and cautioned that one area he is "slightly worried about is financial market asset valuations, which I would characterize as elevated."

He then reverted back to rates, saying that "I will continue to advocate for gradually removing monetary policy accommodation. As I see it, the case for doing so remains strong."

The reason for that is the same one Bank of America highlighted earlier: namely that "financial conditions today are easier than when we started to remove monetary policy accommodation." Which is precisely what Goldman warned nearly a year ago, when it said that it appeared that Yellen had lost control of the market.

As BofA recently noted, "the current backdrop feels very reminiscent of the Greenspan era of 2004-2006. Back then US interest rates rose 17 times. Yet, financial conditions remained loose and interest rate volatility fell to very low levels precisely because Fed monetary tightening was so predictable and patient: rates generally rose by 25bp at each meeting."

Sure enough, to Dudley, "this suggests that the Federal Reserve may have to press harder on the brakes at some point over the next few years. If that happens, the risk of a hard landing will increase."

To sum up Dudley's statement:

“I am optimistic about the near-term economic outlook and the likelihood that the FOMC will be able to make progress this year in pushing inflation up toward its 2 percent objective. The economy has considerable forward momentum, monetary policy is still accommodative, financial conditions are easy, and fiscal policy is set to provide a boost. But, there are some significant storm clouds over the longer term. If the labor market tightens much further, it will be harder to slow the economy to a sustainable pace, avoiding overheating and an eventual economic downturn. Another important issue is the need to get the country’s fiscal house in order for the long run. The longer that task is deferred, the greater the risk for financial markets and the economy, and the harder it will be for the Federal Reserve to keep the economy on an even keel.”

“US Treasury yields are breaking out higher today with 10Y Yields solidly above the 2.50% 'Maginot Line' for the first time since March 2017. The long-end is leading the way higher in yields and steeper in the curve in 2018. The selling pressure is notable, especially considering just how net short Treasuries everyone already is...”

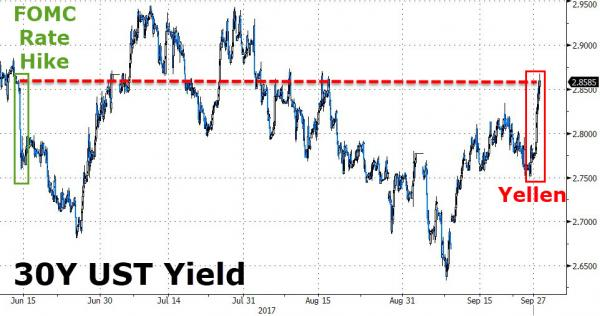

5 Yr. and 10 Yr. U.S. Treasury Note Yield Longer-term View back around 2.50% again.

(Chart courtesy of Zerohedge.com).

The charts display historic downtrend lines dating back nearly 30 years, that may be violated to the upside in the coming weeks.

“While the net speculative position is not as large as in the previous episodes of curve steepening, give it time…this is the moment of truth again for the long end of the bond market, yields are rising for the foreseeable future,” said one notable trader on the CFTC aggregate Net speculative position.

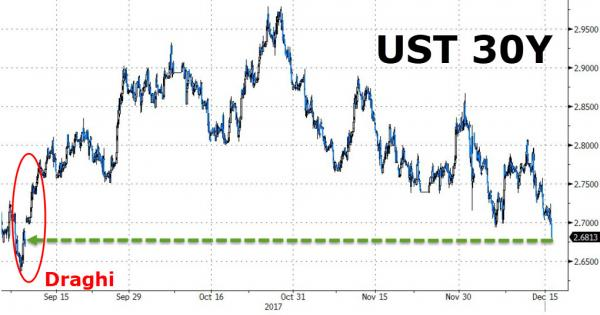

30 Year U.S. Treasury Bond Yield Testing range back above 2.85%.

(Chart courtesy of Zerohedge.com).

The 30 Year U.S. Treasury Bond has now tested the lows and returned to 2.80% and back again to the starting point since the market moving comments from ECB President, Mario Draghi regarding the tapering of bond purchases in late-2018.

10 Yr. U.S. Treasury Note Yield Short-term View back around 2.5367% again.

(Chart courtesy of Zerohedge.com).

The 10 Year U.S. Treasury Note has tested the lows and is moving back to the upper trading range in bond yields. We await whether that gap at 2.05% will get filled in coming months. If so, we will get another run at historically low rates before the final blow-off in Credit Markets sends Mortgage Interest rates up for good.

The above Chart does suggest that a constructive set-up is forming in the 10 Year Treasury Note with the potential to push the yield to around 2.00% over the next month. It is crucial that Mortgage Rates stay at or below 4.00% or demand for mortgage loans will dry up. The window of opportunity for borrowers seeking mortgage refinancing & home purchases is still open for now.

March Fed Funds Futures Rate Hike Odds Rise above 72%.

(Chart courtesy of Zerohedge.com).

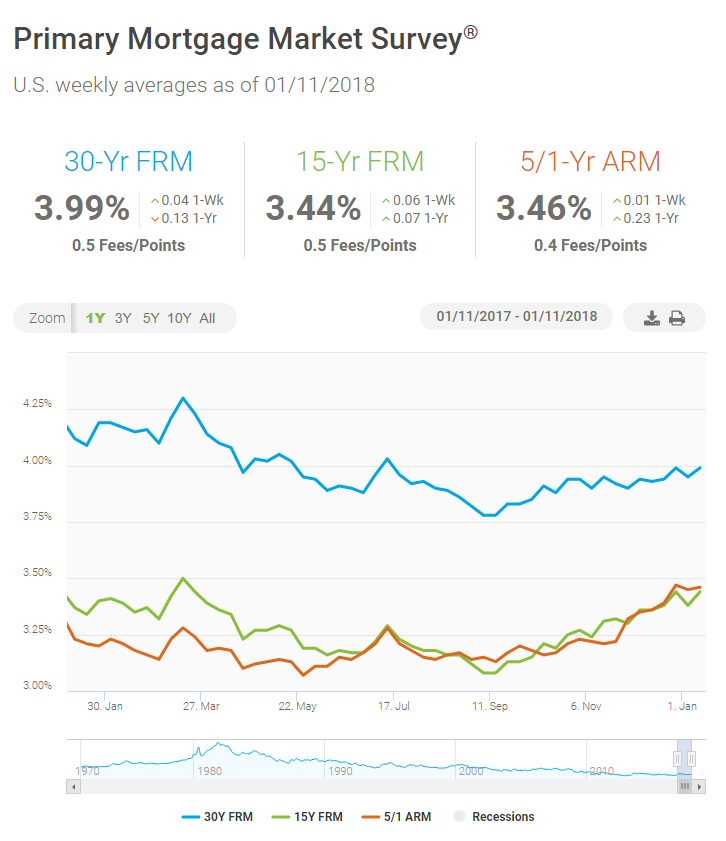

As can be seen from Freddie Mac’s Mortgage Market Survey, last week, 30 Yr. Fixed Mortgage rates for conforming loans hit 3.99% higher by 4 basis points (bps) from the previous week.

Treasury Prices Rise and Yields Fall for U.S. 10 Yr. and 30 Yr. Treasuries.

At the Chicago Board of Trade (CBOT): the US 10 Year Treasury Note futures Contract for March settlement closed at a price of 123’04 / 32nds; the 10 Year Note was up 4 basis points (bps) on the day, yielding 2.5367%. The US 30 Year Treasury Bond futures Contract for March settlement closed at a price of 150’14 / 32nds; the 30 Year Bond was up 12 basis points (bps) on the day, yielding 2.8673%. Mortgage Rates are off their 2017 lows and are higher by 4 basis points (bps) from the previous Freddie Mac Survey last week.

Thanks to ZeroHedge.com, Bureau of Labor Statistics (BLS), B of A Merrill Lynch Global Research, Goldman Sachs, Bloomberg, and FreddieMac.com for Charts and Graphics.

Disclaimer: The Information & content in this message is solely the opinion of the author and believed to be from reliable sources. Charts and tables contained herein were taken from other sources and a best effort was attempted by the author to give attribution where possible. None of this material should be construed as fact, and is not intended for use by reader as investment advice or relied upon for making financial decisions.

Get the Updated and Improved Mortgage Rates App from ERATE.com

- Why housing consumers say you need a real estate agent

- Lenders Double Down on Car-Title Loans Attempting to Stay Ahead of Regulators

- Need Cash Fast? Beware of Greedy Lenders Waiting to Exploit You

- Mortgage Rates and the Stock Market: Understanding the Relationship

- The ERATE® Resource Guide to No-Closing-Cost Refinancing

- You and Your Credit; Make it a Happy Ongoing Relationship

- Principal Reduction: New Programs, More Controversy

- Understanding Mortgages: Mortgage Paperwork

- What is Mortgage Interest?

- Mortgage Terms & Definitions

- Understanding Mortgages: Types of Mortgages

- Understanding Mortgages: How to Get a Mortgage

- What is a Short Sale?

- Understanding Mortgages: Buy or Rent?

- Understanding Mortgages: Working with a Real Estate Agent

- Understanding Mortgages: Working with a Real Estate Agent

- Understanding Credit Cards: Top Mistakes

FREE Mortgage Rate Widgets

Your State's Rates or National Rates Get this Widget for any State you want