Mortgage News

CFPB: Consumers complain about mortgages more than any other financial service tracked

by Broderick Perkins

(8/9/2012) - A year after the Consumer Financial Protection Bureau (CFPB) set up shop to lookout for financial consumers, consumers appear to be just getting started complaining about mortgages.

They complain when they can't make their mortgages and they complain when they can make their payments. They complain about loan modifications and refinancing and they complain about loan servicing, escrow accounts, mortgage originators and mortgage brokers.

It would be easier to discuss mortgage issues that don't lead them to complain, but complain they should.

A home loan is the largest financial stake many consumers have in their future and businesses that serve them ought to get it right - regulatory overhauls of the mortgage and other finance industries demand as much.

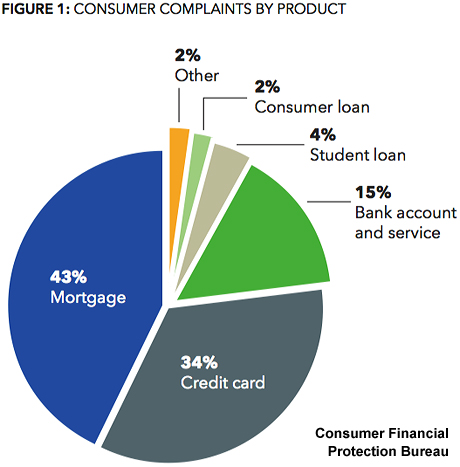

Mortgage complaints (43 percent) topped the list of 55,300 consumer complaints the Consumer Financial Protection Bureau (CFPB) collected over the past year, followed by complaints about credit cards (34 percent), bank accounts and related services (15 percent), student loans (4 percent) and consumer loans (2 percent). Two percent of the complaints came from "other" financial services, according to the "Second Semi-Annual Report of the Consumer Financial Protection Bureau."

Mortgage muddle

Empowered by the Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank Act) and officially opened a year ago, CFPB collected the tens of thousands of complaints between July 21, 2011 and June 30, 2012, as part of it's ongoing challenge to rein in abusive practices in the consumer finance industry.

The report says complaints indicates problems most often arise when consumers are unable to make a payment and seek loan modifications or face foreclosure.

"The complaints indicate that consumer confusion persists around the process and requirements for obtaining loan modifications and refinancing, especially regarding document submission timeframes, payment trial periods, allocation of payments, treatment of income in eligibility calculations, and credit bureau reporting during the evaluation period," the report says.

Consumers are particularly befuddled by the request to quickly submit a ream of loan modification documents that remain valid for a short period of time, only to be asked to submit the documents again - sometimes more than once - after the servicer or lender drops the ball and loses documents or drags out the process and then asks the borrower for another round of documents.

"This seems to contribute to consumer fatigue and frustration with these processes. Other common types of mortgage complaints address issues related to making payments, such as issues related to loan servicing, payments, or escrow accounts," the report says.

For example, consumers wonder if making timely trial modification payments will guarantee them and permanent modification. They also struggle when applying for a loan and dealing with the originator or the mortgage broker, among the most common complaints.

Mortgage consumers who share stories with the CFPB expressed additional challenges and concerns related to obtaining mortgages, including:

Mortgage horror stories

• Inability to qualify for a mortgage loan modification, or if they qualify they are unable to obtain a viable modification that sufficiently lowers their payments.

• Inability to refinance their loans even though they report having high credit scores.

• Lack of clarity about credit scoring and the scores that creditors use versus the scores consumers are given by credit bureaus, making it difficult for consumers to understand this key measure of their creditworthiness.

And that's just from mortgage consumers who complain.

Consumer complaints are part of the direct public feedback approach CFPB takes to understand challenges consumers face and to address those challenges in the form of new regulations, enforcement efforts and programs that improve the consumer experience.

Refinance at Today's Low Rates!

Follow the link to continue reading the related articles:

Impending federal rules prompt mortgage servicers to clean up their act

Wells Fargo settles on $175 million in discrimination restitutions, exists wholesale affiliations

Federal regulators order mortgage servicers not to violate military servicemembers' homeowner rights

Risk adverse lenders give new meaning to 'jumping through hoops'

CFPB mortgage servicing rules expand mortgage industry's regulatory overhaul

Fannie Mae & Jumbo Mortgage Rates

Just One Click! = Current Rate Chart

Start by selecting your state

Real Estate Market News

- New consumer finance bureau opens to criticism

- Watchdog SAFE Act curbing toxic mortgages

- Many consumers chronically mystified by mortgage maze

- Why housing consumers say you need a real estate agent

- States offer incentives for green improvements

- More borrowers reach for ARMs

- California issues consumer alerts for mortgage fraud

- Why vacant homes are a tough sell

- Could you qualify for a 'Qualified Residential Mortgage?'

- Government failed housing, but continues heavy housing subsidies

- Disconnect between what buyers, sellers want

- Is your real estate agent packing the latest technology?

- Mortgage maze still leaves home buyers in a haze

- Jobs-housing connection a key indicator to watch

- Investors move to the head of the home-buying class

- Foreign buyers cashing in on U.S. housing closeout sale

- S&P/Case-Shiller index confirms 'double-dip,' home buying opportunities

- Half of consumers can't come up with down payment

- Erate's 'Dirty Half Dozen Digital Ways to Buy or Sell in Today's Housing Market'

- Married couples ready to take the plunge

- Utah BBB issues EZ Loan Protection alert

- Housing to take center stage in 2012 election

- Don't over look credit union mortgages

- Renting gets tricky

- Voters united over homeownership

- Big break for California short sellers

- New survey ferrets out top markets for SFH rental property investments

- Consumer watchdog opens amid efforts to defang the new agency

- Housing counseling generates optimism during tough times

- Feds target deceptive mortgage advertising years after ads contributed to crash

- Mortgage rates eye of Wall Street storm after S&P downgrade

- Feds pondering how to unload government-owned distressed properties

- Best Back-to-School Real Estate Investment Cities

- Investors better than banks, Feds at shrinking distressed inventory

- Gauge your housing market's recovery and cash in

- Home ownership beats renting, if you can get a loan

- It's housing, stupid

- Mortgage morass gets murkier

Refinancing: Selecting a Loan

- Mortgage Program Options

- Interest Only Mortgage

- 100% Mortgage Financing - No Down Payment

- Mortgage Rates Comparison

- Mortgage Rates Tracker

- Search for Mortgage Rates

- No Costs Mortgage Refinancing

- 2% Rule - Refinancing Mortgage

- Yield Spread Premium

- Zero Costs Mortgage Refinancing

- Prepayment Penalty - Mortgage Refinancing

- What is APR and how is it calculated?

- Private Mortgage Insurance - Refinancing

Moving Ahead With Your Refinance

- Apply for a Mortgage

- Is it best to pay points up front to reduce the interest rate?

- Rate Lock info - Refinancing Mortgage

- Refinancing Mortgage Tax Information

- Should you pre-pay your mortgage?

- Title Insurance for Mortgage Refinancing

- Homeowner's Insurance

- Earthquake Insurance - Refinancing Mortgage